Answered step by step

Verified Expert Solution

Question

1 Approved Answer

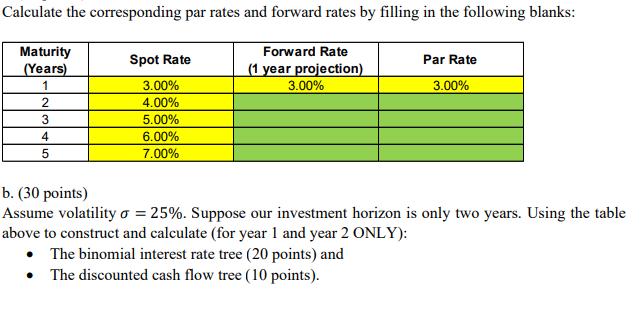

Calculate the corresponding par rates and forward rates by filling in the following blanks: Forward Rate (1 year projection) 3.00% Maturity (Years) 1 2

Calculate the corresponding par rates and forward rates by filling in the following blanks: Forward Rate (1 year projection) 3.00% Maturity (Years) 1 2 3 4 5 Spot Rate 3.00% 4.00% 5.00% 6.00% 7.00% Par Rate 3.00% b. (30 points) Assume volatility o = 25%. Suppose our investment horizon is only two years. Using the table above to construct and calculate (for year 1 and year 2 ONLY): The binomial interest rate tree (20 points) and The discounted cash flow tree (10 points).

Step by Step Solution

★★★★★

3.44 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

To construct the binomial interest rate tree we can use a twostep binomial model based on the given ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics For Business Decision Making And Analysis

Authors: Robert Stine, Dean Foster

2nd Edition

978-0321836519, 321836510, 978-0321890269