calculate the dividend/cash flow each year using thr growth rate.

determine where the growth if the company becomes constant (this is the key constant growth rate model), this is called the terminal or horizon value. this will gice you a value.

place each of these cash flows into the calculator or excel using the interest rate given and calculate NPV,which is now called the intrinsic value.

show all work

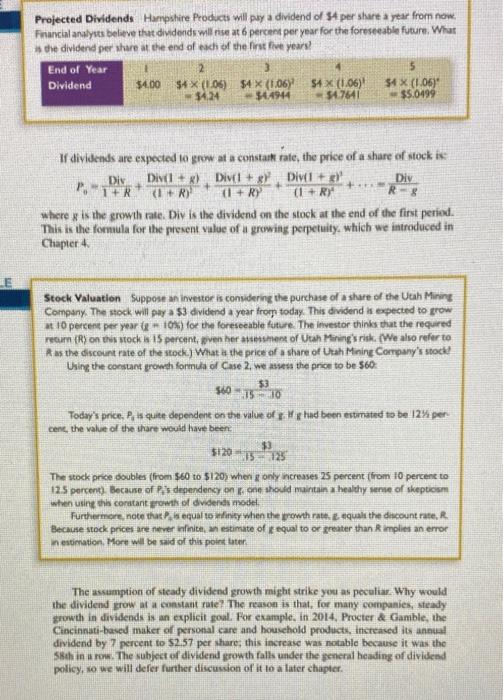

Projected Dividends Hampshire Products will pay a dividend of 34 per share a year from now. Financial analysts believe the dividends will rise at 6 percent per year for the foreseeable future, What e dividend per shure at the end of each of the first five years End of Year 2 5 Dividend $4.00 $4X (105) $4x (1.06) S4 x (1.06) $4X (1.06) 34.24 5.4944 54.7641 $5.0499 If dividends are expected to grow at a constark rate, the price of a share of stock is DiN Dive+ Div(tte Diyet Div ( IR) (1 + R) (1+RY R8 Where x is the growth rate. Div is the dividend on the stock at the end of the first period. This is the formula for the present value of a growing perpetuity, which we introduced in Chapter 4 +R E Stock Valuation Support an investor is considering the purchase of a share of the Utah Mining Company. The stock will pay a $3 dividend a year from today. This dividend is expected to grow 10 percent per year 10%) for the foreseeable future. The investor thinks that the required recum (R) on this stock 15 percent ven her assesment of Utah Mining's risk. (We also refer to A as the discount rate of the stock.) What as the price of a share of Utah Mining Company's stocked Using the constant growth forms of Case 2, we assess the prior to be 560 53 5601510 Today's price. Po as quite dependent on the value of n. Wy had been estimated to be 12% per cent, the value of the share would have been $3 5:20. B The stock pride doubles (from $60 to $120, when only increases 25 percent (from 10 percent to 12.5 percent). Because of Ps dependency on one should maintain a healthy sense of skepticism when using this constant growth of dividends model Furthermore, note that is equal to finity when the growth rate. Etqualithe discount rate, Because stock prices are never Infinite, mestimate of equal to or greater than implies an error estimation More will be said of this point later The assumption of steady dividend growth might strike you as peculiar. Why would the dividend grow at a constant rate? The reason is that, for many companies, steady growth in dividends is an explicit goul. For example, in 2014, Procter & Gamble, the Cincinnati-based maker of personal care and household products, increased its annual dividend by 7 percent to $2.57 per share, this increase was notable because it was 5th in a row. The subject of dividend growth falls under the general heading of dividend policy, so we will defer further discussion of it to a later chapter. You might wonder what would happen with the dividend growth model if the growth rate, 8. were greater than the discount rate, R. It looks like we would get a negative stock price because R - g would be less than zero. This is not what would happen. Instead, if the constant growth rate exceeds the discount rate, then the stock price is infinitely large. Why? If the growth rate is bigger than the discount rate, the present value of the dividends keeps getting bigger. Essentially the same is true if the growth rate and the discount rate are equal. In both cases, the simplification that allows us to replace the infinite stream of dividends with the dividend growth model is illegal." so the answers we get from the dividend growth model are nonsense unless the growth rate is less than the discount rate Case 3 (Differential Growth) In this case, an algebraic formula would be too unwieldy. Instead, we present examples. Differential Growth Comider Elbdir Drug Company, which is expected to enjoy rapid growth from the introduction of its new back ryb ointment. The dividend for a share of Elodir's stock a year from today is expected to be 51.15. During the next four years, the dividend is expected to grow 15 percent per year (-15%). After that, growth () will be equal to 10 percent per year. Calculate the present value of a share of stock if the required return (R) s 15 percent. Figure 9.2 Growth in Dividends for Ear Drug Company 10% growth rate Dividends 1 $2.9449 15% growth rate 52.6772 $2.2008 20114 $2.2125 $1.450 $1.5209 $11225 $1.15 N End of year Pure 9.2 display the growth in Boris dividends. We need to apply a two-step process to discount these dividende We first calculate the present value of the dividends growing at 15 percent per annum. That we first calculate the present out of the dividends at the end of each of the fire five years. Second, we calculate the prevent value of the vidende beginning the end of Year LO der Course Hero chegg.com/reader/9781259295881/314/ Credit Card, Mortga.. M Gmail Home | St. Joseph's... Paused Course Hero Other bookmarks Readil The "Idea" with the free cash flow q... a Qa . 278 WATU WC Present of Fine Dividende the Future Erd 1 15 The Thew Presente de Dindd DOO - The - 9.2 Estimates of Parameters in the Dividend Discount Model nem 10 Type here to search o Projected Dividends Hampshire Products will pay a dividend of 34 per share a year from now. Financial analysts believe the dividends will rise at 6 percent per year for the foreseeable future, What e dividend per shure at the end of each of the first five years End of Year 2 5 Dividend $4.00 $4X (105) $4x (1.06) S4 x (1.06) $4X (1.06) 34.24 5.4944 54.7641 $5.0499 If dividends are expected to grow at a constark rate, the price of a share of stock is DiN Dive+ Div(tte Diyet Div ( IR) (1 + R) (1+RY R8 Where x is the growth rate. Div is the dividend on the stock at the end of the first period. This is the formula for the present value of a growing perpetuity, which we introduced in Chapter 4 +R E Stock Valuation Support an investor is considering the purchase of a share of the Utah Mining Company. The stock will pay a $3 dividend a year from today. This dividend is expected to grow 10 percent per year 10%) for the foreseeable future. The investor thinks that the required recum (R) on this stock 15 percent ven her assesment of Utah Mining's risk. (We also refer to A as the discount rate of the stock.) What as the price of a share of Utah Mining Company's stocked Using the constant growth forms of Case 2, we assess the prior to be 560 53 5601510 Today's price. Po as quite dependent on the value of n. Wy had been estimated to be 12% per cent, the value of the share would have been $3 5:20. B The stock pride doubles (from $60 to $120, when only increases 25 percent (from 10 percent to 12.5 percent). Because of Ps dependency on one should maintain a healthy sense of skepticism when using this constant growth of dividends model Furthermore, note that is equal to finity when the growth rate. Etqualithe discount rate, Because stock prices are never Infinite, mestimate of equal to or greater than implies an error estimation More will be said of this point later The assumption of steady dividend growth might strike you as peculiar. Why would the dividend grow at a constant rate? The reason is that, for many companies, steady growth in dividends is an explicit goul. For example, in 2014, Procter & Gamble, the Cincinnati-based maker of personal care and household products, increased its annual dividend by 7 percent to $2.57 per share, this increase was notable because it was 5th in a row. The subject of dividend growth falls under the general heading of dividend policy, so we will defer further discussion of it to a later chapter. You might wonder what would happen with the dividend growth model if the growth rate, 8. were greater than the discount rate, R. It looks like we would get a negative stock price because R - g would be less than zero. This is not what would happen. Instead, if the constant growth rate exceeds the discount rate, then the stock price is infinitely large. Why? If the growth rate is bigger than the discount rate, the present value of the dividends keeps getting bigger. Essentially the same is true if the growth rate and the discount rate are equal. In both cases, the simplification that allows us to replace the infinite stream of dividends with the dividend growth model is illegal." so the answers we get from the dividend growth model are nonsense unless the growth rate is less than the discount rate Case 3 (Differential Growth) In this case, an algebraic formula would be too unwieldy. Instead, we present examples. Differential Growth Comider Elbdir Drug Company, which is expected to enjoy rapid growth from the introduction of its new back ryb ointment. The dividend for a share of Elodir's stock a year from today is expected to be 51.15. During the next four years, the dividend is expected to grow 15 percent per year (-15%). After that, growth () will be equal to 10 percent per year. Calculate the present value of a share of stock if the required return (R) s 15 percent. Figure 9.2 Growth in Dividends for Ear Drug Company 10% growth rate Dividends 1 $2.9449 15% growth rate 52.6772 $2.2008 20114 $2.2125 $1.450 $1.5209 $11225 $1.15 N End of year Pure 9.2 display the growth in Boris dividends. We need to apply a two-step process to discount these dividende We first calculate the present value of the dividends growing at 15 percent per annum. That we first calculate the present out of the dividends at the end of each of the fire five years. Second, we calculate the prevent value of the vidende beginning the end of Year LO der Course Hero chegg.com/reader/9781259295881/314/ Credit Card, Mortga.. M Gmail Home | St. Joseph's... Paused Course Hero Other bookmarks Readil The "Idea" with the free cash flow q... a Qa . 278 WATU WC Present of Fine Dividende the Future Erd 1 15 The Thew Presente de Dindd DOO - The - 9.2 Estimates of Parameters in the Dividend Discount Model nem 10 Type here to search o