Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Calculate the expected utility for both investors if they invested solely in each industry. Which industry does each investor prefer? What are the reasons for

- Calculate the expected utility for both investors if they invested solely in each industry. Which industry does each investor prefer? What are the reasons for their preference?

- Consider the MATL and HC industries. What is the optimal portfolio for both Boris and Angela that contains these two industries? Discuss what happens to each investor's utility and portfolio risk for this portfolio compared to holding these two industries individually. Will you always reach this conclusion or is specific to these two portfolios?

- Calculate the optimal portfolio for both investors that consists of the following five industries: MATL, CONS, TELE, RE, and HC. How does this portfolio compare to the one industry and two industry portfolios in terms of diversification benefits to each investor?

- Calculate the optimal portfolio for both investors that consists of all eleven industries. Compare this to the other portfolios you have already estimated in terms of diversification benefits. What do you observe? Contrast the differences in what you observe between the two investors.

- Now consider the case where both Boris and Angela can invest in a risk-free asset. The risk-free rate is 0.5% per month. Estimate the optimal combined portfolio for each investor using the five industries in part 3 and then estimate the optimal combined portfolio for each investor using all eleven industries. How does the existence of the risk-free rate affect your conclusion regarding diversification benefits? Are diversification benefits increased or reduced if the investors can borrow or lend at a risk-free rate?

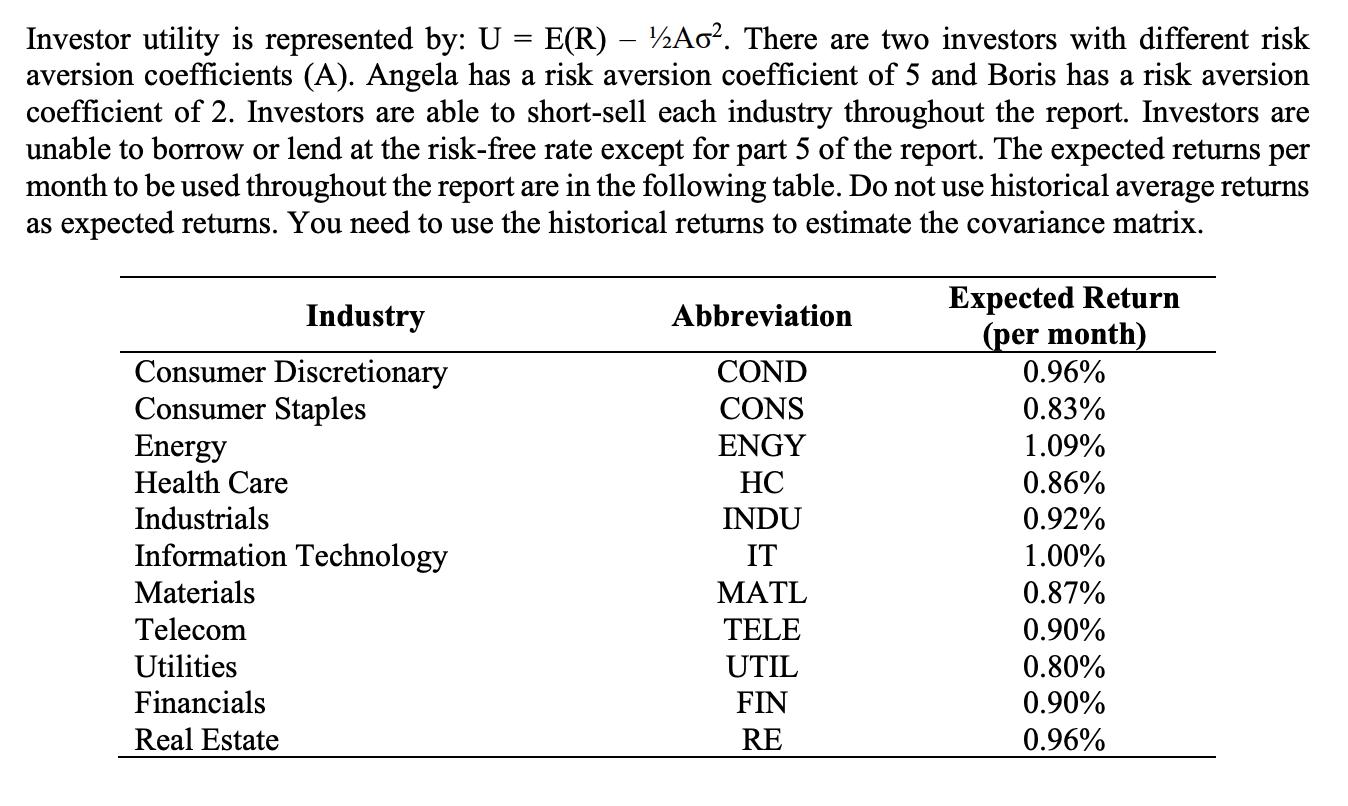

Investor utility is represented by: U = E(R) Ao. There are two investors with different risk aversion coefficients (A). Angela has a risk aversion coefficient of 5 and Boris has a risk aversion coefficient of 2. Investors are able to short-sell each industry throughout the report. Investors are unable to borrow or lend at the risk-free rate except for part 5 of the report. The expected returns per month to be used throughout the report are in the following table. Do not use historical average returns as expected returns. You need to use the historical returns to estimate the covariance matrix. Industry Consumer Discretionary Consumer Staples Energy Health Care Industrials Information Technology Materials Telecom Utilities Financials Real Estate Abbreviation COND CONS ENGY HC INDU IT MATL TELE UTIL FIN RE Expected Return (per month) 0.96% 0.83% 1.09% 0.86% 0.92% 1.00% 0.87% 0.90% 0.80% 0.90% 0.96%

Step by Step Solution

★★★★★

3.52 Rating (159 Votes )

There are 3 Steps involved in it

Step: 1

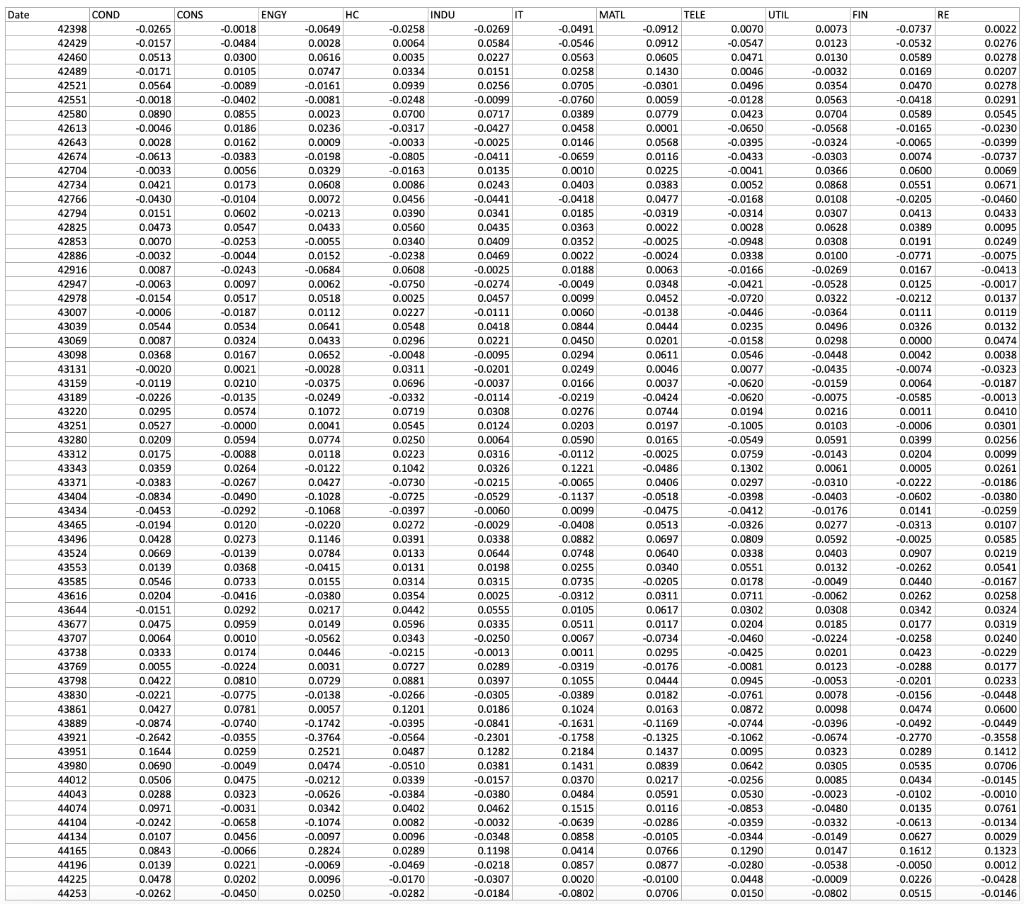

Question The expected utility of each industry COND CONS ENGY HC INDU IT The expected utility of Angela 022 045 064 036 035 023 The expected utility of Boris 066 068 040 066 069 051 MATL TELE UTIL FIN ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance Turning Money into Wealth

Authors: Arthur J. Keown

7th edition

978-0133856507, 013385650X, 133856437, 978-0133856439