Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Calculate the standard deviation of the portfolio Consider the data provided in the table below for a portfolio of assets A and B. The portfolio

Calculate the standard deviation of the portfolio

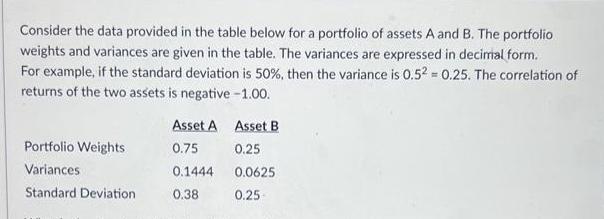

Consider the data provided in the table below for a portfolio of assets A and B. The portfolio weights and variances are given in the table. The variances are expressed in decimal form. For example, if the standard deviation is 50%, then the variance is 0.52 = 0.25. The correlation of returns of the two assets is negative -1.00. Portfolio Weights Variances Standard Deviation Asset A Asset B 0.75 0.25 0.1444 0.0625 0.38 0.25

Step by Step Solution

★★★★★

3.46 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the standard deviation of a portfolio consisting of two assets A and B you need to know ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction to Corporate Finance What Companies Do

Authors: John Graham, Scott Smart

3rd edition

9781111532611, 1111222282, 1111532613, 978-1111222284