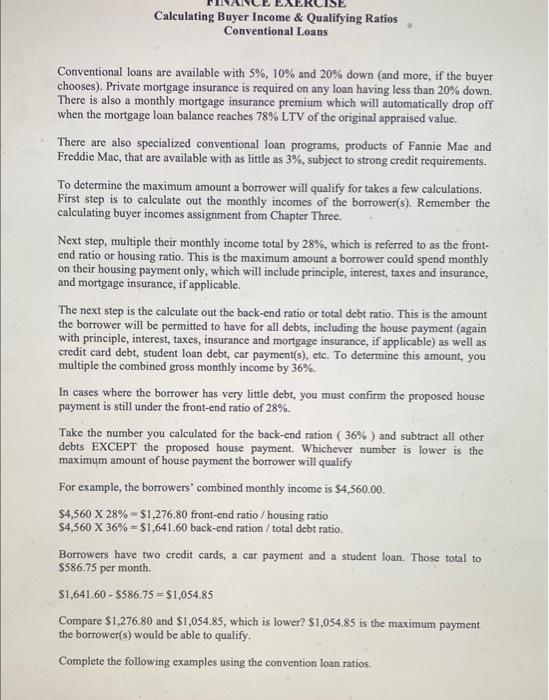

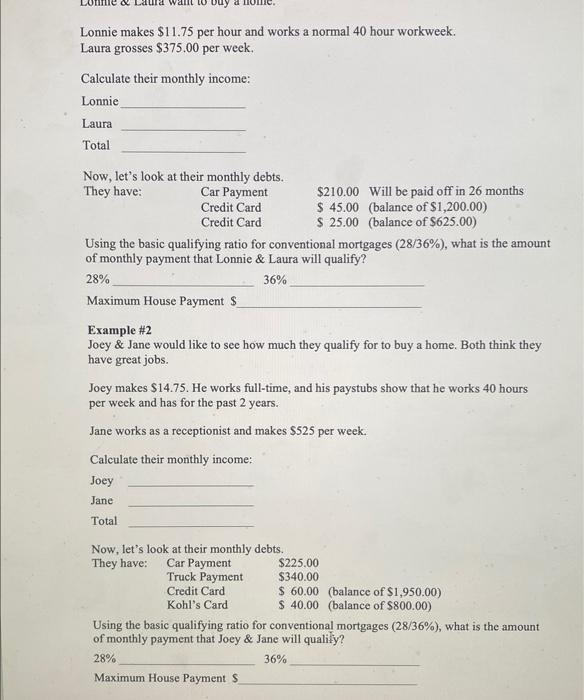

Calculating Buyer Income \& Qualifying Ratios Conventional Loans Conventional loans are available with 5%,10% and 20% down (and more, if the buyer chooses). Private mortgage insurance is required on any loan having less than 20% down. There is also a monthly mortgage insurance premium which will automatically drop off when the mortgage loan balance reaches 78% LTV of the original appraised value. There are also specialized conventional loan programs, products of Fannie Mae and Freddie Mac, that are available with as little as 3%, subject to strong credit requirements. To determine the maximum amount a borrower will qualify for takes a few calculations. First step is to calculate out the monthly incomes of the borrower(s). Remember the calculating buyer incomes assignment from Chapter Three. Next step, multiple their monthly income total by 28%, which is referred to as the frontend ratio or housing ratio. This is the maximum amount a borrower could spend monthly on their housing payment only, which will include principle, interest, taxes and insurance, and mortgage insurance, if applicable. The next step is the calculate out the back-end ratio or total debt ratio. This is the amount the borrower will be permitted to have for all debts, including the house payment (again with principle, interest, taxes, insurance and mortgage insurance, if applicable) as well as credit card debt, student loan debt, car payment(5), etc. To determine this amount, you multiple the combined gross monthly income by 36%. In cases where the borrower has very little debt, you must confirm the proposed house payment is still under the front-end ratio of 28%. Take the number you calculated for the back-end ration ( 36%) and subtract all other debts EXCEPT the proposed house payment. Whichever number is lower is the maximum amount of house payment the borrower will qualify For example, the borrowers' combined monthly income is $4,560.00. $4,56028%=$1,276.80 front-end ratio / housing ratio $4,56036%=$1,641,60 back-end ration / total debt ratio. Borrowers have two credit cards, a car payment and a student loan. Those total to $586.75 per month. $1,641.60$586.75=$1,054.85 Compare $1,276.80 and $1,054.85, which is lower? $1,054.85 is the maximum payment the borrower(s) would be able to qualify. Complete the following examples using the convention loan ratios. Lonnie makes $11.75 per hour and works a normal 40 hour workweek. Laura grosses $375.00 per week. Calculate their monthly income: Lonnie Laura Total Now, let's look at their monthly debts. They have: CarPaymentCreditCardCreditCard$210.00Willbepaidoffin26months$45.00(balanceof$1,200.00)$25.00(balanceof$625.00) Using the basic qualifying ratio for conventional mortgages ( 28/36% ), what is the amount of monthly payment that Lonnie \& Laura will qualify? 28% Maximum House Payment $ Example \#2 Joey \& Jane would like to see how much they qualify for to buy a home. Both think they have great jobs. Joey makes $14.75. He works full-time, and his paystubs show that he works 40 hours per week and has for the past 2 years. Jane works as a receptionist and makes $525 per week. Calculate their monthly income: Joey Jane Total Now, let's look at their monthly debts. Theyhave:KohlsCardCarPaymentTruckPaymentCreditCard$40.00(balanceof$800.00)$225.00$340.00$60.00(balanceof$1,950.00) Using the basic qualifying ratio for conventional mortgages ( 28/36%), what is the amount of monthly payment that Joey \& Jane will qualify? 28% Maximum House Payment $