Question

Calculation and working out. I have been working on this for last few hours, and the answer seems to be wrong.... I would like to

Calculation and working out. I have been working on this for last few hours, and the answer seems to be wrong.... I would like to compare my working outs with expert's

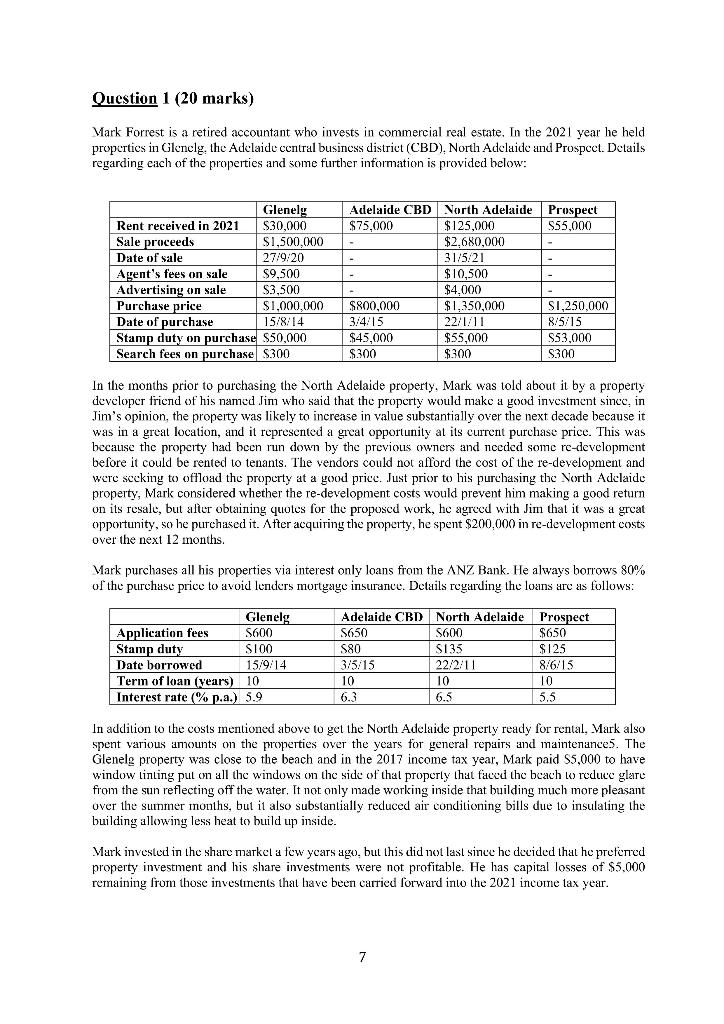

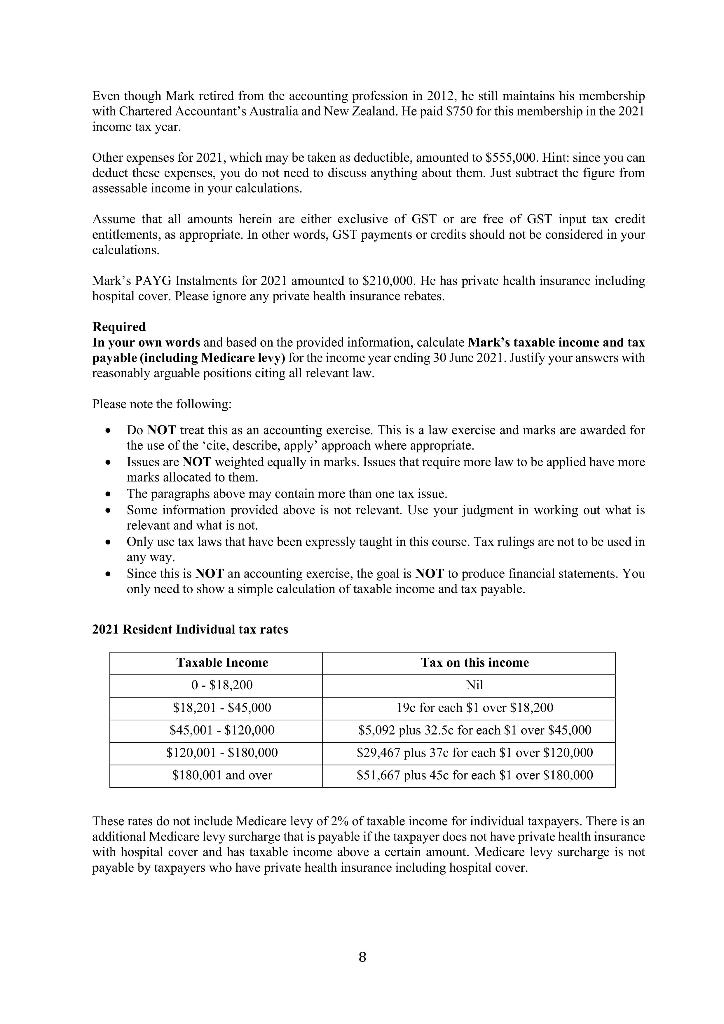

Question 1 (20 marks) Mark Forrest is a retired accountant who invests in commercial real estate. In the 2021 year he held properties in Glenelg, the Adelaide central business district (CBD). North Adelaide and Prospect. Details regarding cach of the properties and some further information is provided below: Adelaide CBD North Adelaide Prospect $75.000 $125,000 S55,000 $2,680,000 31/5/21 Glenely Rent received in 2021 $30.000 Sale proceeds $1,500,000 Date of sale 27/9:20 Agent's fees on sale Advertising on sale Purchase price $1,000,000 100 Date of purchase 15/8/14 Stamp duty on purchase $50,000 Search fees on purchase 300 $9,500 $3.500 $10,500 S1,250,000 $800,000 3:4:15 $45.000 $4.000 $1,350,000 22/1/11 $55,000 $300 8:5:15 S53.000 $300 $300 In the months prior to purchasing the North Adelaide property, Mark was told about it by a property developer friend of his named Jim who said that the property would make a good investment since in Jim's opinion, the property was likely to increase in value substantially over the next decade because it was in a great location, and it represented a great opportunity at its current purchase price. This was because the property had been run down by the previous owners and needed some re-development ore i to tenants. The vendors could afford the cost re-development were seeking to offload the property at a good price. Just prior to his purchasing the North Adelaide property, Mark considered whether the re-development costs would prevent him making a good return on its resalc, but alter obtaining quotes for the proposed work, he agreed with Jim that it was a great opportunity, so he purchased it. After acquiring the property, he spent $200,000 in re-development costs over the next 12 inonths. be Mark purchases all his properties via interest only loans from the ANZ Bank. He always borrows 80% of the purchase price to avoid lenders mortgage insurance. Details regarding the loans are as follows: Glenelg Application fees S600 Stamp duty S100 Date borrowed 15:9:14 Term of loan (years) 10 Interest rate (% p.a.) 5.9 Adelaide CBD S650 580 3:5:15 10 6.3 North Adelaide Prospect 5600 $650 S135 $125 22/2/11 8/6/15 10 10 6.5 5,5 In addition to the costs mentioned above to get the North Adelaide property ready for rental, Mark also spent various amounts on the properties over the years for general repairs and maintenance. The Glenelg property was close to the beach and in the 2017 income tax year, Mark paid $5,000 to have window linting put on all the windows on the side of thal properly that faced the beach to reduce glaru from the sun reflecting off the water. It not only made working inside that building much more pleasant over the sunmer months, but it also substantially reduced air conditioning bills due to insulating the building allowing less heat to build up inside. Mark invested in the share market a few years ago, but this did not last since he decided that he preferred property investment and his share investments were not profitable. He has capital losses of $5.000 remaining from those investments that have been carried forward into the 2021 income tax year. 7 Even though Mark retired from the accounting profession in 2012, he still maintains his membership with Chartered Accountant's Australia and New Zealand. He paid S750 for this membership in the 2021 income tax ycar. Other expenses for 2021, which may be taken as deductible, amounted to $555,000. Hint: since you can deduct these expenses, you do not need to discuss anything about them. Just subtract the figure from assessable income in your calculations. Assume that all amounts herein are either exclusive of GST or are free of GST input tax credit entitlements, as appropriate. In other words, GST payments or credits should not be considered in your calculations. Mark's PAYG Instalments for 2021 amounted to $210,000. He has privatchcalth insurance including hospital cover. Please ignore any private health insurance rebates. Required In your own words and based on the provided information, calculate Mark's taxable income and tax payable (including Medicare levy) for the income year ending 30 June 2021. Justify your answers with reasonably arguable positions citing all relevant law. Please note the following: . . Do NOT treat this as an accounting exercise. This is a law exercise and marks are awarded for the use of the 'cite, describe, apply' approach where appropriate. Issues are NOT weighted equally in marks. Issues that require more law to be applied have more marks allocated to them. The paragraphs above may contain more than one lax issue. Some information provided above is not relevant. Use your judgment in working out what is relevant and what is not. Only use tax laws that have been expressly taught in this course. Tax rulings are not to be used in any way Since this is NOT an accounting exercise, the goal is NOT to produce financial statements. You only need to show a simple calculation of taxable income and tax payable. . . 2021 Resident Individual tax rates Taxable income 0 - $18,200 $18,201 - $45,000 $45,001 - $120,000 $120,001 - S180,000 Tax on this income Nil 19c for each $1 over $18,200 $5,092 plus 32.5c for each $1 over $45,000 S29,467 plus 37c for each $1 over $120,000 $51.667 plus 45c for each $1 over $180.000 $180.001 and over These rates do not include Medicare levy of 2% of taxable income for individual taxpayers. There is an additional Medicare levy surcharge that is payable if the taxpayer does not have private health insurance with hospital cover and has taxable income above certain amount. Medicare levy surcharge is not payable by taxpayers who have private health insurance including hospital cover. 8 Question 1 (20 marks) Mark Forrest is a retired accountant who invests in commercial real estate. In the 2021 year he held properties in Glenelg, the Adelaide central business district (CBD). North Adelaide and Prospect. Details regarding cach of the properties and some further information is provided below: Adelaide CBD North Adelaide Prospect $75.000 $125,000 S55,000 $2,680,000 31/5/21 Glenely Rent received in 2021 $30.000 Sale proceeds $1,500,000 Date of sale 27/9:20 Agent's fees on sale Advertising on sale Purchase price $1,000,000 100 Date of purchase 15/8/14 Stamp duty on purchase $50,000 Search fees on purchase 300 $9,500 $3.500 $10,500 S1,250,000 $800,000 3:4:15 $45.000 $4.000 $1,350,000 22/1/11 $55,000 $300 8:5:15 S53.000 $300 $300 In the months prior to purchasing the North Adelaide property, Mark was told about it by a property developer friend of his named Jim who said that the property would make a good investment since in Jim's opinion, the property was likely to increase in value substantially over the next decade because it was in a great location, and it represented a great opportunity at its current purchase price. This was because the property had been run down by the previous owners and needed some re-development ore i to tenants. The vendors could afford the cost re-development were seeking to offload the property at a good price. Just prior to his purchasing the North Adelaide property, Mark considered whether the re-development costs would prevent him making a good return on its resalc, but alter obtaining quotes for the proposed work, he agreed with Jim that it was a great opportunity, so he purchased it. After acquiring the property, he spent $200,000 in re-development costs over the next 12 inonths. be Mark purchases all his properties via interest only loans from the ANZ Bank. He always borrows 80% of the purchase price to avoid lenders mortgage insurance. Details regarding the loans are as follows: Glenelg Application fees S600 Stamp duty S100 Date borrowed 15:9:14 Term of loan (years) 10 Interest rate (% p.a.) 5.9 Adelaide CBD S650 580 3:5:15 10 6.3 North Adelaide Prospect 5600 $650 S135 $125 22/2/11 8/6/15 10 10 6.5 5,5 In addition to the costs mentioned above to get the North Adelaide property ready for rental, Mark also spent various amounts on the properties over the years for general repairs and maintenance. The Glenelg property was close to the beach and in the 2017 income tax year, Mark paid $5,000 to have window linting put on all the windows on the side of thal properly that faced the beach to reduce glaru from the sun reflecting off the water. It not only made working inside that building much more pleasant over the sunmer months, but it also substantially reduced air conditioning bills due to insulating the building allowing less heat to build up inside. Mark invested in the share market a few years ago, but this did not last since he decided that he preferred property investment and his share investments were not profitable. He has capital losses of $5.000 remaining from those investments that have been carried forward into the 2021 income tax year. 7 Even though Mark retired from the accounting profession in 2012, he still maintains his membership with Chartered Accountant's Australia and New Zealand. He paid S750 for this membership in the 2021 income tax ycar. Other expenses for 2021, which may be taken as deductible, amounted to $555,000. Hint: since you can deduct these expenses, you do not need to discuss anything about them. Just subtract the figure from assessable income in your calculations. Assume that all amounts herein are either exclusive of GST or are free of GST input tax credit entitlements, as appropriate. In other words, GST payments or credits should not be considered in your calculations. Mark's PAYG Instalments for 2021 amounted to $210,000. He has privatchcalth insurance including hospital cover. Please ignore any private health insurance rebates. Required In your own words and based on the provided information, calculate Mark's taxable income and tax payable (including Medicare levy) for the income year ending 30 June 2021. Justify your answers with reasonably arguable positions citing all relevant law. Please note the following: . . Do NOT treat this as an accounting exercise. This is a law exercise and marks are awarded for the use of the 'cite, describe, apply' approach where appropriate. Issues are NOT weighted equally in marks. Issues that require more law to be applied have more marks allocated to them. The paragraphs above may contain more than one lax issue. Some information provided above is not relevant. Use your judgment in working out what is relevant and what is not. Only use tax laws that have been expressly taught in this course. Tax rulings are not to be used in any way Since this is NOT an accounting exercise, the goal is NOT to produce financial statements. You only need to show a simple calculation of taxable income and tax payable. . . 2021 Resident Individual tax rates Taxable income 0 - $18,200 $18,201 - $45,000 $45,001 - $120,000 $120,001 - S180,000 Tax on this income Nil 19c for each $1 over $18,200 $5,092 plus 32.5c for each $1 over $45,000 S29,467 plus 37c for each $1 over $120,000 $51.667 plus 45c for each $1 over $180.000 $180.001 and over These rates do not include Medicare levy of 2% of taxable income for individual taxpayers. There is an additional Medicare levy surcharge that is payable if the taxpayer does not have private health insurance with hospital cover and has taxable income above certain amount. Medicare levy surcharge is not payable by taxpayers who have private health insurance including hospital cover. 8Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Development Of Integrated Reporting In The SME SectorCase Studies From European Countries

Authors: Joanna Dyczkowska, Andrea Szirmai Madarasine, Adriana Tiron-Tudor

1st Edition

3030819027, 9783030819026