Can I get help with this?

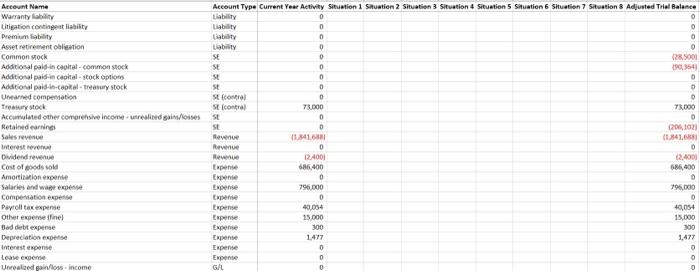

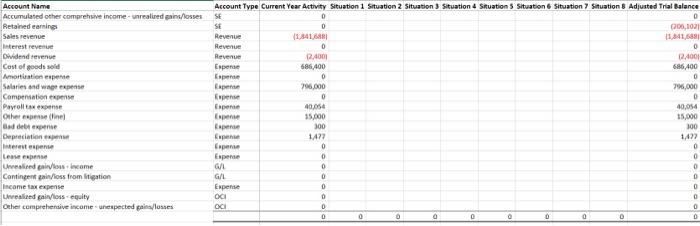

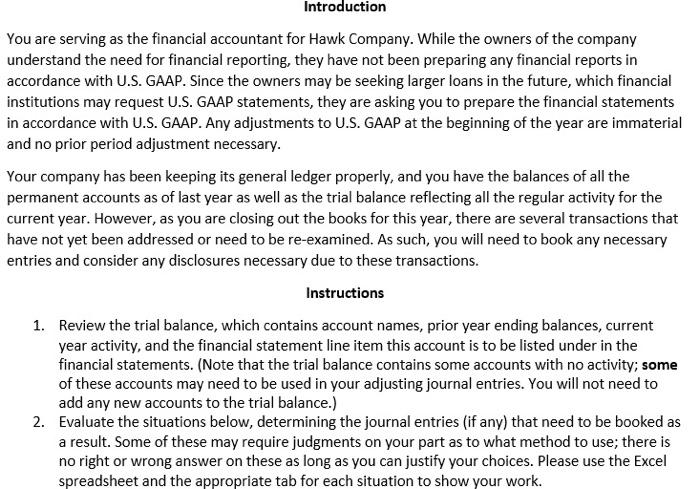

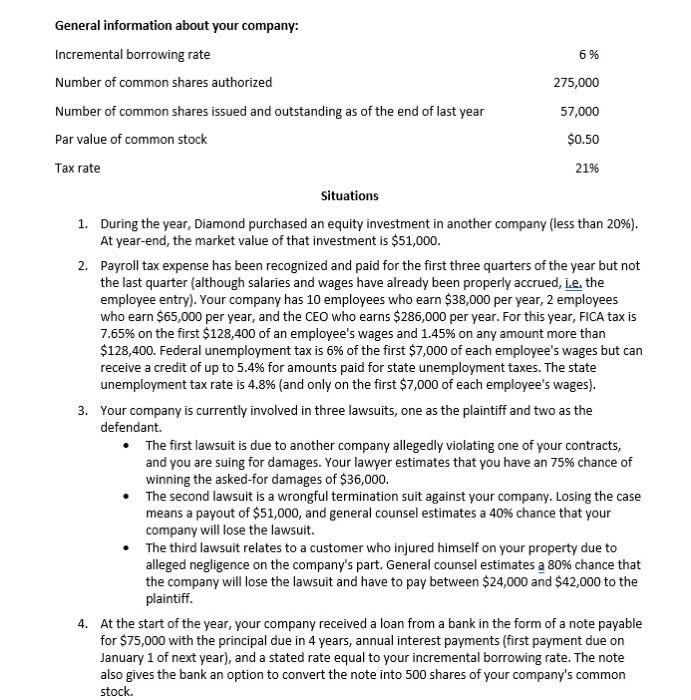

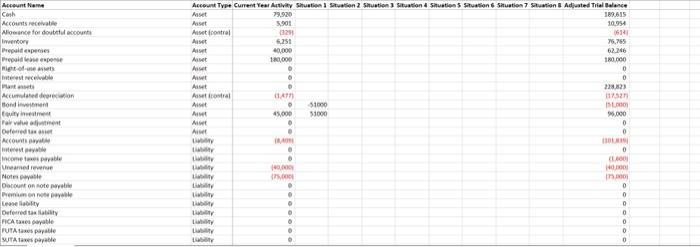

You are serving as the financial accountant for Hawk Company. While the owners of the company understand the need for financial reporting, they have not been preparing any financial reports in accordance with U.S. GAAP. Since the owners may be seeking larger loans in the future, which financial institutions may request U.S. GAAP statements, they are asking you to prepare the financial statements in accordance with U.S. GAAP. Any adjustments to U.S. GAAP at the beginning of the year are immaterial and no prior period adjustment necessary. Your company has been keeping its general ledger properly, and you have the balances of all the permanent accounts as of last year as well as the trial balance reflecting all the regular activity for the current year. However, as you are closing out the books for this year, there are several transactions that have not yet been addressed or need to be re-examined. As such, you will need to book any necessary entries and consider any disclosures necessary due to these transactions. Instructions 1. Review the trial balance, which contains account names, prior year ending balances, current year activity, and the financial statement line item this account is to be listed under in the financial statements. (Note that the trial balance contains some accounts with no activity; some of these accounts may need to be used in your adjusting journal entries. You will not need to add any new accounts to the trial balance.) 2. Evaluate the situations below, determining the journal entries (if any) that need to be booked as a result. Some of these may require judgments on your part as to what method to use; there is no right or wrong answer on these as long as you can justify your choices. Please use the Excel spreadsheet and the appropriate tab for each situation to show your work. 2. Payroll tax expense has been recognized and paid for the first three quarters of the year but not the last quarter (although salaries and wages have already been properly accrued, i.e, the employee entry). Your company has 10 employees who earn $38,000 per year, 2 employees who earn $65,000 per year, and the CEO who earns $286,000 per year. For this year, FICA tax is 7.65% on the first $128,400 of an employee's wages and 1.45% on any amount more than $128,400. Federal unemployment tax is 6% of the first $7,000 of each employee's wages but can receive a credit of up to 5.4% for amounts paid for state unemployment taxes. The state unemployment tax rate is 4.8% (and only on the first $7,000 of each employee's wages). 3. Your company is currently involved in three lawsuits, one as the plaintiff and two as the defendant. - The first lawsuit is due to another company allegedly violating one of your contracts, and you are suing for damages. Your lawyer estimates that you have an 75% chance of winning the asked-for damages of $36,000. - The second lawsuit is a wrongful termination suit against your company. Losing the case means a payout of $51,000, and general counsel estimates a 40% chance that your company will lose the lawsuit. - The third lawsuit relates to a customer who injured himself on your property due to alleged negligence on the company's part. General counsel estimates a 80% chance that the company will lose the lawsuit and have to pay between $24,000 and $42,000 to the plaintiff. 4. At the start of the year, your company received a loan from a bank in the form of a note payable for $75,000 with the principal due in 4 years, annual interest payments (first payment due on January 1 of next year), and a stated rate equal to your incremental borrowing rate. The note also gives the bank an option to convert the note into 500 shares of your company's common stock. You are serving as the financial accountant for Hawk Company. While the owners of the company understand the need for financial reporting, they have not been preparing any financial reports in accordance with U.S. GAAP. Since the owners may be seeking larger loans in the future, which financial institutions may request U.S. GAAP statements, they are asking you to prepare the financial statements in accordance with U.S. GAAP. Any adjustments to U.S. GAAP at the beginning of the year are immaterial and no prior period adjustment necessary. Your company has been keeping its general ledger properly, and you have the balances of all the permanent accounts as of last year as well as the trial balance reflecting all the regular activity for the current year. However, as you are closing out the books for this year, there are several transactions that have not yet been addressed or need to be re-examined. As such, you will need to book any necessary entries and consider any disclosures necessary due to these transactions. Instructions 1. Review the trial balance, which contains account names, prior year ending balances, current year activity, and the financial statement line item this account is to be listed under in the financial statements. (Note that the trial balance contains some accounts with no activity; some of these accounts may need to be used in your adjusting journal entries. You will not need to add any new accounts to the trial balance.) 2. Evaluate the situations below, determining the journal entries (if any) that need to be booked as a result. Some of these may require judgments on your part as to what method to use; there is no right or wrong answer on these as long as you can justify your choices. Please use the Excel spreadsheet and the appropriate tab for each situation to show your work. 2. Payroll tax expense has been recognized and paid for the first three quarters of the year but not the last quarter (although salaries and wages have already been properly accrued, i.e, the employee entry). Your company has 10 employees who earn $38,000 per year, 2 employees who earn $65,000 per year, and the CEO who earns $286,000 per year. For this year, FICA tax is 7.65% on the first $128,400 of an employee's wages and 1.45% on any amount more than $128,400. Federal unemployment tax is 6% of the first $7,000 of each employee's wages but can receive a credit of up to 5.4% for amounts paid for state unemployment taxes. The state unemployment tax rate is 4.8% (and only on the first $7,000 of each employee's wages). 3. Your company is currently involved in three lawsuits, one as the plaintiff and two as the defendant. - The first lawsuit is due to another company allegedly violating one of your contracts, and you are suing for damages. Your lawyer estimates that you have an 75% chance of winning the asked-for damages of $36,000. - The second lawsuit is a wrongful termination suit against your company. Losing the case means a payout of $51,000, and general counsel estimates a 40% chance that your company will lose the lawsuit. - The third lawsuit relates to a customer who injured himself on your property due to alleged negligence on the company's part. General counsel estimates a 80% chance that the company will lose the lawsuit and have to pay between $24,000 and $42,000 to the plaintiff. 4. At the start of the year, your company received a loan from a bank in the form of a note payable for $75,000 with the principal due in 4 years, annual interest payments (first payment due on January 1 of next year), and a stated rate equal to your incremental borrowing rate. The note also gives the bank an option to convert the note into 500 shares of your company's common stock