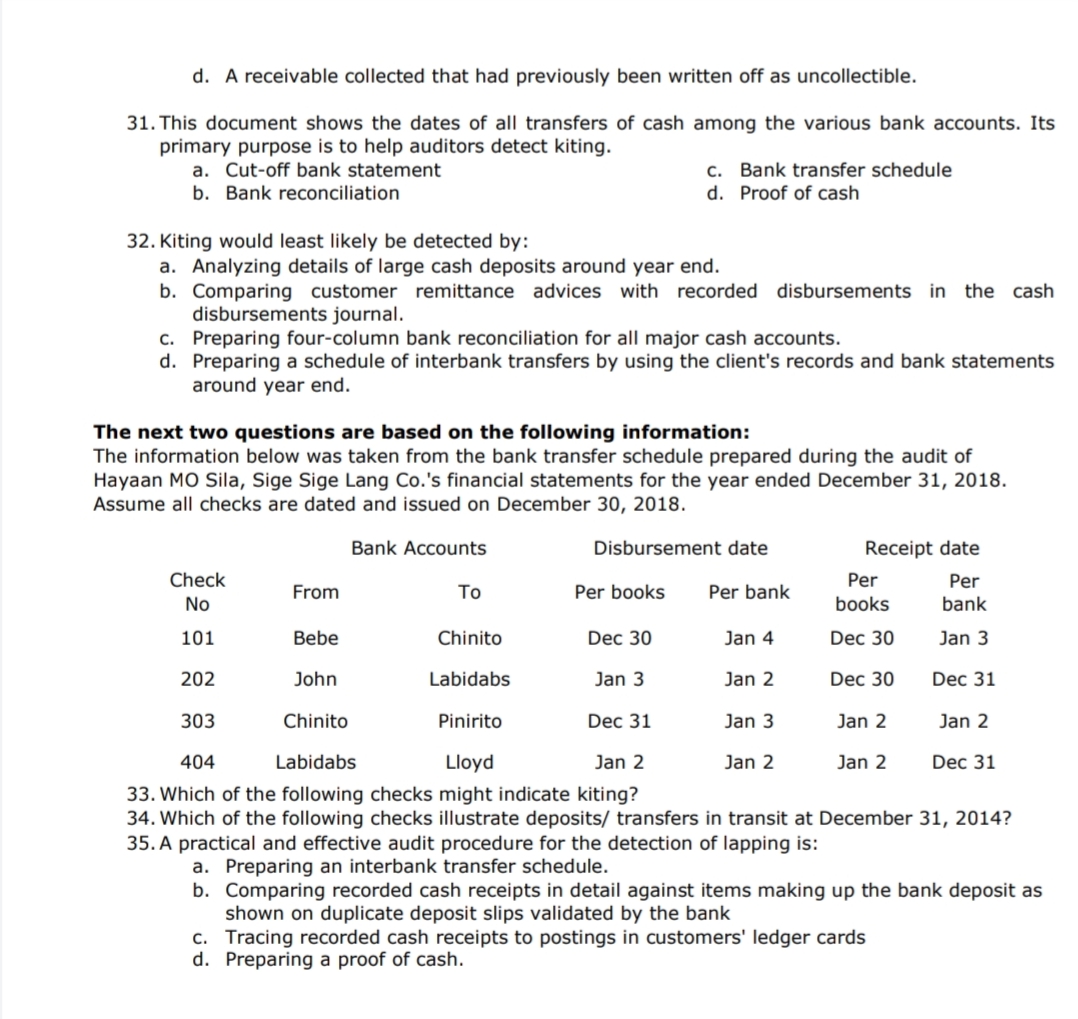

Can someone help me (with solutions in the problem)

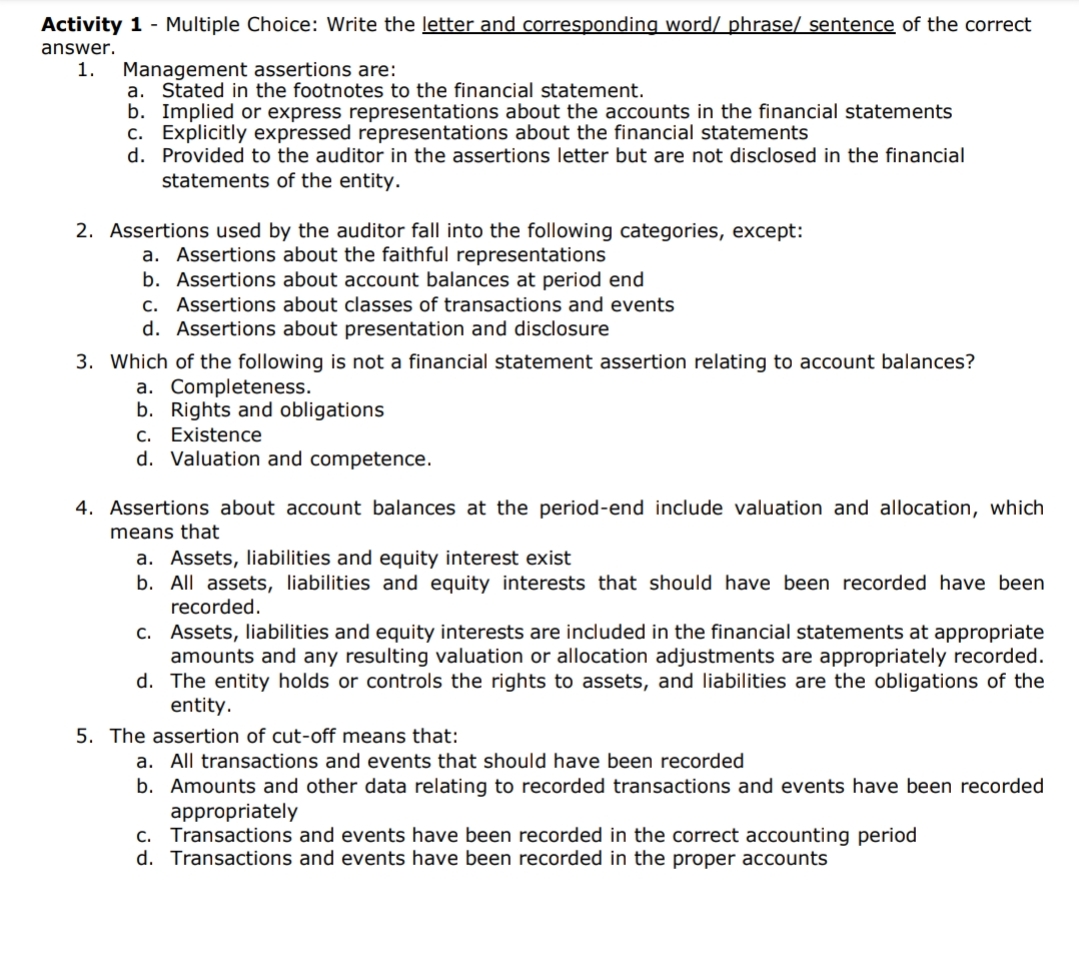

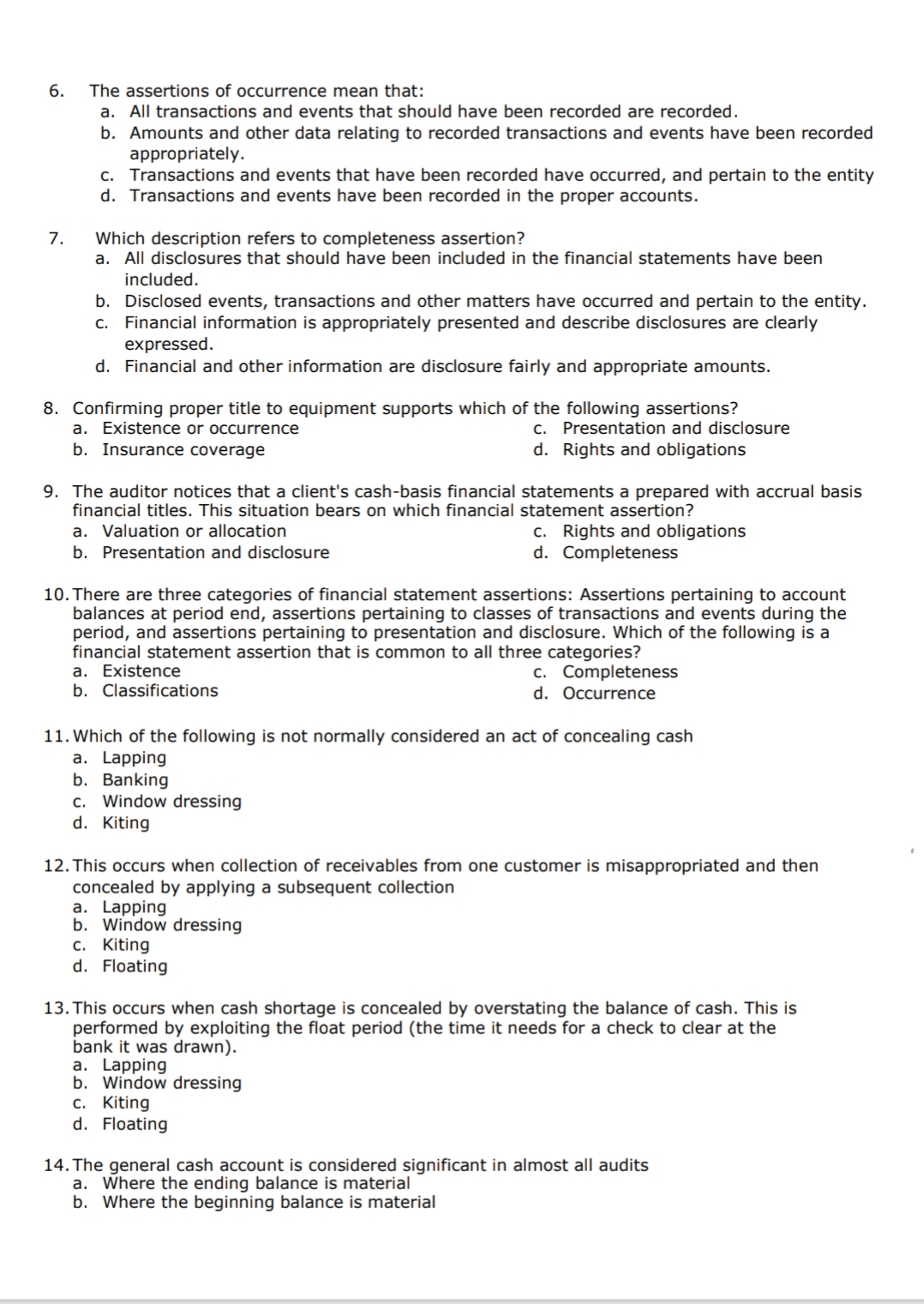

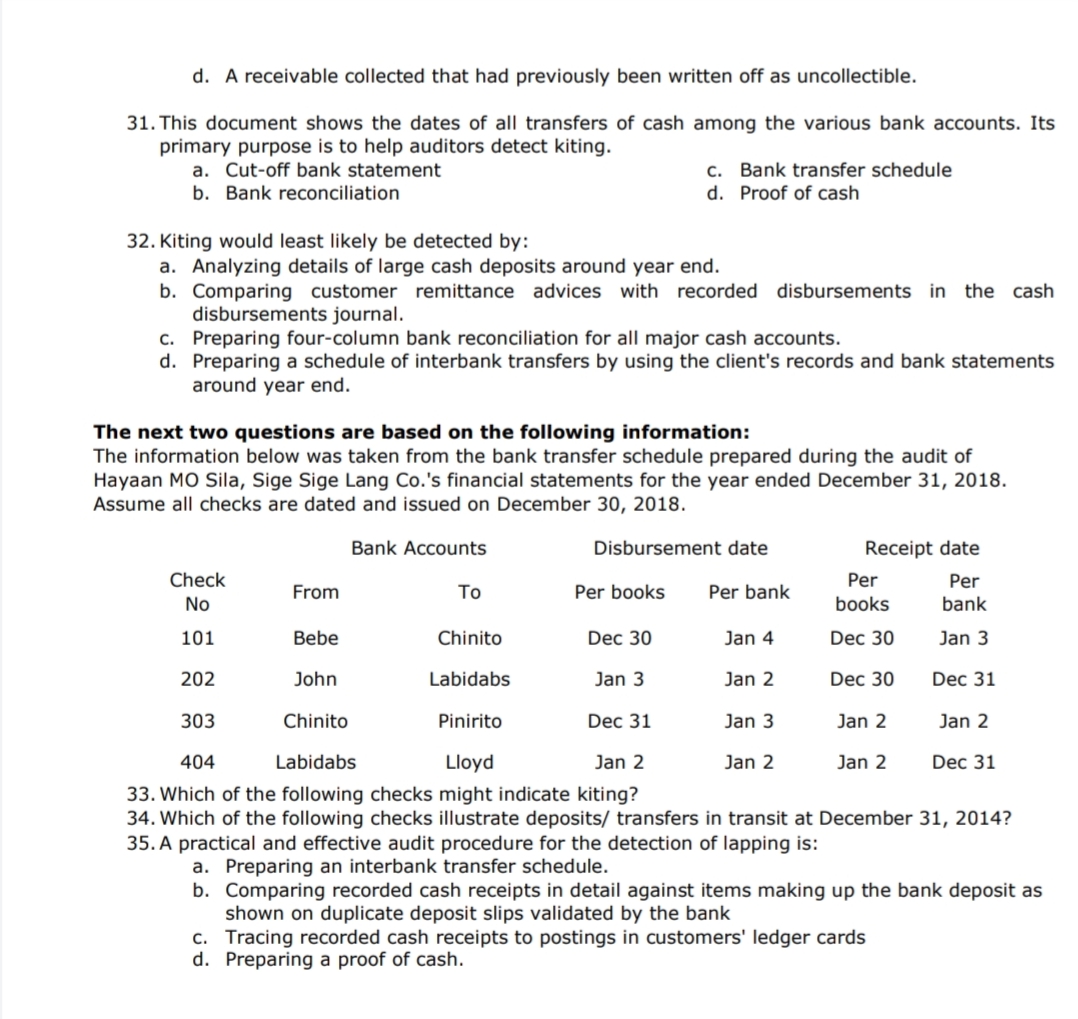

Activity 1 - Multiple Choice: Write the letter and corresponding word/ phrase/ sentence of the correct answer. 1. Management assertions are: a. Stated in the footnotes to the financial statement. b. Implied or express representations about the accounts in the financial statements . Explicitly expressed representations about the financial statements d. Provided to the auditor in the assertions letter but are not disclosed in the financial statements of the entity. 2. Assertions used by the auditor fall into the following categories, except: a. Assertions about the faithful representations b. Assertions about account balances at period end c. Assertions about classes of transactions and events d. Assertions about presentation and disclosure 3. Which of the following is not a financial statement assertion relating to account balances? a. Completeness b. Rights and obligations C. Existence d. Valuation and competence. 4. Assertions about account balances at the period-end include valuation and allocation, which means that a. Assets, liabilities and equity interest exist b. All assets, liabilities and equity interests that should have been recorded have been recorded. C. Assets, liabilities and equity interests are included in the financial statements at appropriate amounts and any resulting valuation or allocation adjustments are appropriately recorded. d. The entity holds or controls the rights to assets, and liabilities are the obligations of the entity. 5. The assertion of cut-off means that: a. All transactions and events that should have been recorded b. Amounts and other data relating to recorded transactions and events have been recorded appropriately C. Transactions and events have been recorded in the correct accounting period d. Transactions and events have been recorded in the proper accounts6. The assertions of occurrence mean that: a. All transactions and events that should have been recorded are recorded. b. Amounts and other data relating to recorded transactions and events have hem recorded appropriately. c. Transactions and events that have been recorded have occurred, and pertain to the entity d. Transactions and events have been recorded in the proper accounts. 7. Which description refers to completeness assertion? a. All disclosures that should have been included in the nancial statements have been included. b. Disclosed events, transactions and other matters have occun'ed and pertain to the entity. c. Financial information is appropriately presented and describe disclosures are clearly expressed. d. Financial and other information are disdosure fairly and appropriate amounts. 8. Conrming proper title to equipment supports which of the following assertions? a. Existence or occurrence c. Presentation and disclosure b. Insurance coverage d. Rights and obligations 9. The auditor notices that a client's cashbasis nancial statements a prepared with accrual basis nancial titles. This situation bears on which nancial statement assertion? a. Valuation or allocation c. Rights and obligations b. Presentation and disclosure d. Completeness 10.There are three categories of nancial statement assertions: Assertions pertaining to account balances at period end, assertions pertaining to classes of transactions and events during the period, and assertions pertaining to presentation and disclosure. Which of the following is a financial statement assertion that is common to all three categories? a. Existence c. Completeness b. Classications d. Occurrence 11. Which of the following is not normally considered an act of concealing cash a. Lapping b. Banking c. Window dressing d. Kiting 12.This occurs when collection of receivables from one customer is misappropriated and then concealed by applying a subsequent collection a. Lapping b. Window dressing c. Kiting d. Floating 13.This occurs when cash shortage is concealed by overstating the balance of cash. This is performed by exploiting the float period (the time it needs for a check to clear at the bank it was drawn). a. Lapping b. Window dressing c. Kiting d. Floating 14.The general cash account is considered signicant in almost all audits a. Where the ending balance is material b. Where the beginning balance is material Even when the ending balance is immaterial d. Except those for non-profit organizations 15. When conducting surprise cash count, the auditor should simultaneously count all cash funds, marketable securities and other negotiable assets to prevent a. Time-out b. Defalcation Substitution d. Misappropriation 16. A cash shortage may be concealed by transporting funds from one location to another or by converting negotiable assets to cash. Because of this, which of the following is vital? a. b. Simultaneous confirmations. d. Simultaneous verification. Simultaneous bank reconciliations. Simultaneous surprise cash count. 17. The primary purpose of sending a standard bank confirmation request to financial institutions with which the client has done business during the year is to: a. Request information concerning contingent liabilities & collateral b. Detect kiting activities that may otherwise not be discovered C. Provide the data needed to prepare the bank section of a four-column proof of cash. d. Corroborate/verify information regarding cash & loan balances. 18. As one of the year-end audit procedures, the auditor instructed the client's personnel to prepare a standard bank confirmation request for a bank account that had been closed during the year. After the client's treasurer had signed the request, it was mailed by the assistant treasurer. What is the major flaw in this audit procedure? a. The confirmation request was signed by the treasurer. b. Sending the request was meaningless because the account was closed before the year-end. c. The request was mailed by the assistant treasurer. d. The CPA did not sign the confirmation request before it was mailed. 19. In October, three months before year-end, the bookkeeper erroneously recorded the receipt of a one year bank loan with a debit to cash and a credit to miscellaneous revenue. Select the most effective method for detecting this type of error. a. Foot the cash receipts journal for October. b. Send a bank confirmation as of year-end. C. Prepare bank reconciliation as of year-end. d. Prepare a bank transfer schedule as of year-end. 20. Which of the following is not confirmed on the standard form used for cash balances at financial institutions? a. Cash checking account balances. Cash savings account balances. c. Loans payable. d. Securities held for the client by the financial institution. 21. The primary assertion being addressed by sending bank confirmation is a. Existence b. Completeness c. Rights and obligation d. Classification 22. Which of the following assertions is least likely to be addressed by sending bank confirmation? a. Existence b. Completeness c. Rights and obligation d. Classification 23. This document is a bank statement prepared a few days after month end Its purpose is to help auditors verify reconciling items on the year-end bank reconciliation.a. Cut-off bank statement c. Bank transfer schedule b. Bank reconciliation d. Proof of cash 24.An auditor who is engaged to examine the nancial statements of a business enterprise will request a cutoff bank statement primarily in order to a. Verify the cash balance reported on the bank conrmation inquiry form. b. Verify reconciling items on the client's bank reconciliation. c. Detect lapping. d. Detect kiting. 25.The auditors use a bank cutoff statement to compare: a. Deposits in transit on the year-end cash general ledger account to deposits in the cash receipts journal. b. Checks dated prior to year-end to the outstanding ched