Answered step by step

Verified Expert Solution

Question

1 Approved Answer

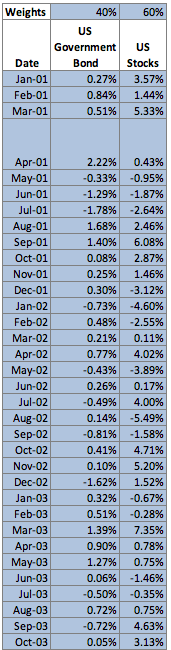

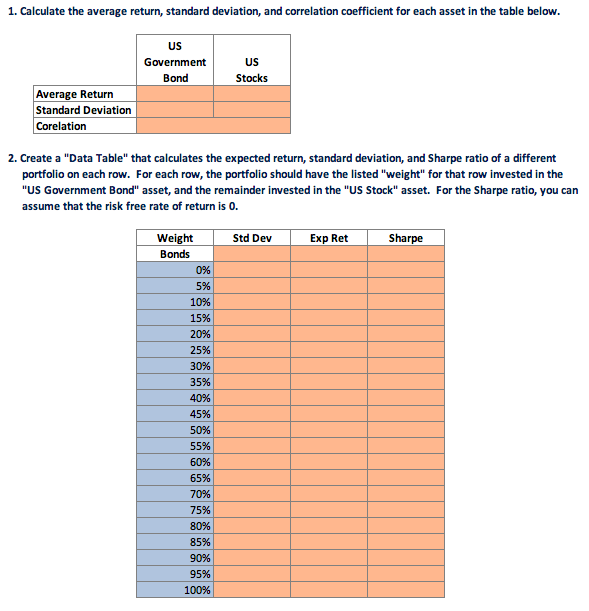

Can someone help me with the orange areas? Please show me the formulas/steps, I really appreciate it! 60% Weights 40% US Government Date Bond Jan-01

Can someone help me with the orange areas? Please show me the formulas/steps, I really appreciate it!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The House That Bogle Built How John Bogle And Vanguard Reinvented The Mutual Fund Industry

Authors: Lewis Braham

1st Edition

0071749063,0071751157