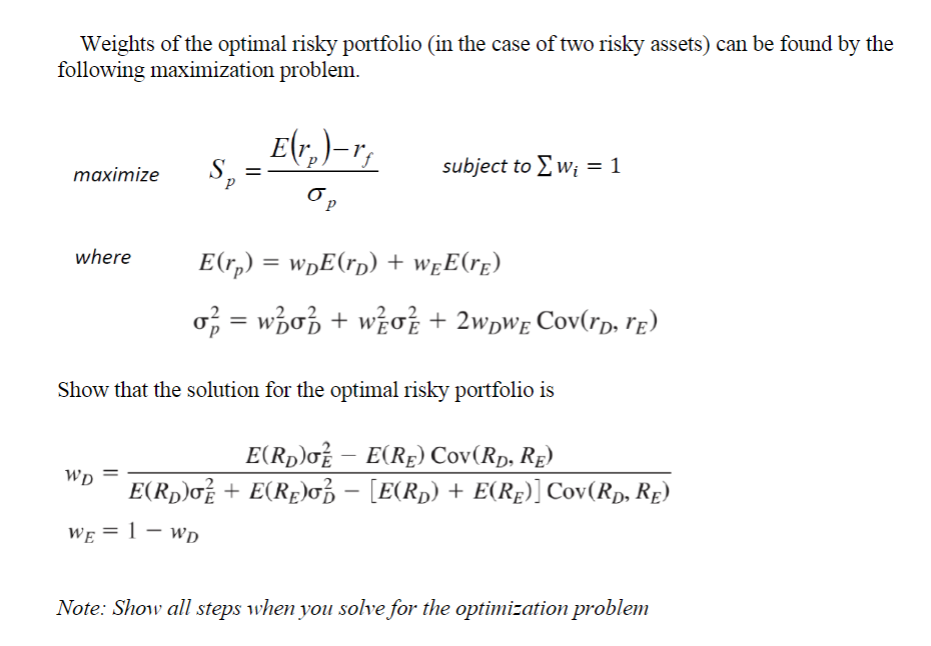

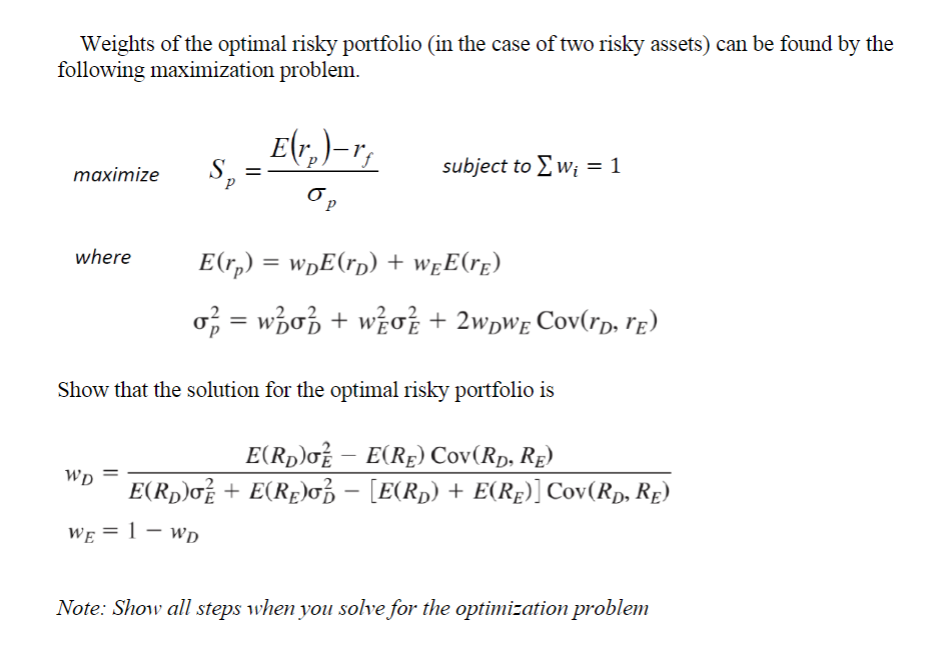

Question

Can someone help with this optimization problem (need to show all steps)? first you have the maximization formula and that's where you start, you use

Can someone help with this optimization problem (need to show all steps)? first you have the maximization formula and that's where you start, you use the other two subject to formulas in the steps to get to the final answer which is the last two formulas (Wd and We). You need to show that you can maximize the Sp formula and get to Wd and We formulas as the final answer.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Multinational Finance

Authors: Michael H. Moffett, Arthur I. Stonehill, David K. Eiteman

5th edition

205989756, 978-0205989751