can someone please explain how to solve this problem of 5.6 but in simpler terms? im confused on how you know when to buy foreign currency and convert versus when you should buy US currency and convert.

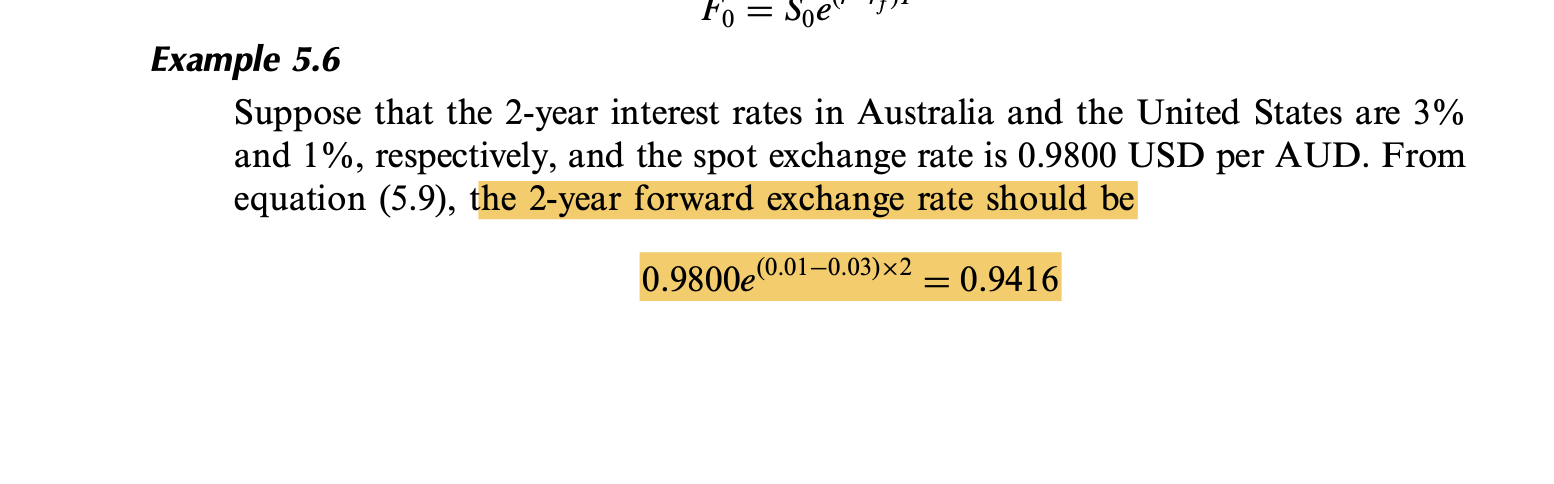

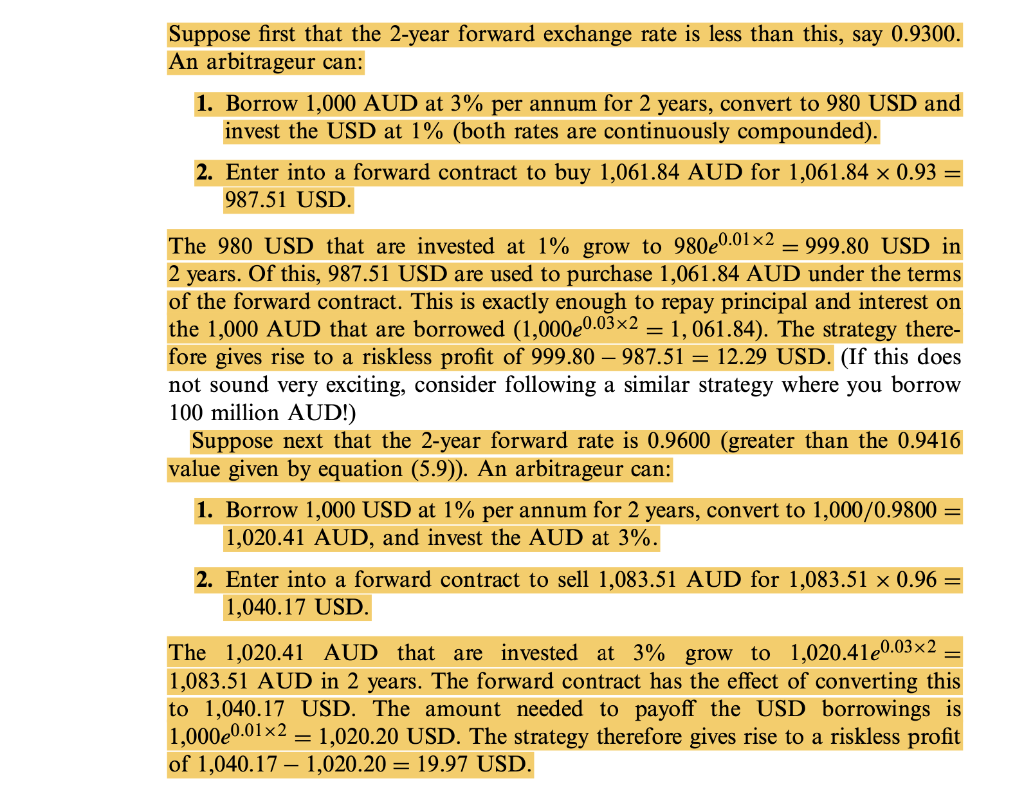

ample 5.6 Suppose that the 2-year interest rates in Australia and the United States are 3\% and 1%, respectively, and the spot exchange rate is 0.9800 USD per AUD. From equation (5.9), the 2-year forward exchange rate should be 0.9800e(0.010.03)2=0.9416 Suppose first that the 2-year forward exchange rate is less than this, say 0.9300. An arbitrageur can: 1. Borrow 1,000AUD at 3% per annum for 2 years, convert to 980USD and invest the USD at 1% (both rates are continuously compounded). 2. Enter into a forward contract to buy 1,061.84AUD for 1,061.840.93= 987.51 USD. The 980 USD that are invested at 1% grow to 980e0.012=999.80 USD in 2 years. Of this, 987.51USD are used to purchase 1,061.84 AUD under the terms of the forward contract. This is exactly enough to repay principal and interest on the 1,000AUD that are borrowed (1,000e0.032=1,061.84). The strategy therefore gives rise to a riskless profit of 999.80987.51=12.29USD. (If this does not sound very exciting, consider following a similar strategy where you borrow 100 million AUD!) Suppose next that the 2-year forward rate is 0.9600 (greater than the 0.9416 value given by equation (5.9)). An arbitrageur can: 1. Borrow 1,000 USD at 1% per annum for 2 years, convert to 1,000/0.9800= 1,020.41AUD, and invest the AUD at 3%. 2. Enter into a forward contract to sell 1,083.51 AUD for 1,083.510.96= 1,040.17 USD. The 1,020.41 AUD that are invested at 3% grow to 1,020.41e0.032= 1,083.51 AUD in 2 years. The forward contract has the effect of converting this to 1,040.17 USD. The amount needed to payoff the USD borrowings is 1,000e0.012=1,020.20 USD. The strategy therefore gives rise to a riskless profit of 1,040.171,020.20=19.97 USD. ample 5.6 Suppose that the 2-year interest rates in Australia and the United States are 3\% and 1%, respectively, and the spot exchange rate is 0.9800 USD per AUD. From equation (5.9), the 2-year forward exchange rate should be 0.9800e(0.010.03)2=0.9416 Suppose first that the 2-year forward exchange rate is less than this, say 0.9300. An arbitrageur can: 1. Borrow 1,000AUD at 3% per annum for 2 years, convert to 980USD and invest the USD at 1% (both rates are continuously compounded). 2. Enter into a forward contract to buy 1,061.84AUD for 1,061.840.93= 987.51 USD. The 980 USD that are invested at 1% grow to 980e0.012=999.80 USD in 2 years. Of this, 987.51USD are used to purchase 1,061.84 AUD under the terms of the forward contract. This is exactly enough to repay principal and interest on the 1,000AUD that are borrowed (1,000e0.032=1,061.84). The strategy therefore gives rise to a riskless profit of 999.80987.51=12.29USD. (If this does not sound very exciting, consider following a similar strategy where you borrow 100 million AUD!) Suppose next that the 2-year forward rate is 0.9600 (greater than the 0.9416 value given by equation (5.9)). An arbitrageur can: 1. Borrow 1,000 USD at 1% per annum for 2 years, convert to 1,000/0.9800= 1,020.41AUD, and invest the AUD at 3%. 2. Enter into a forward contract to sell 1,083.51 AUD for 1,083.510.96= 1,040.17 USD. The 1,020.41 AUD that are invested at 3% grow to 1,020.41e0.032= 1,083.51 AUD in 2 years. The forward contract has the effect of converting this to 1,040.17 USD. The amount needed to payoff the USD borrowings is 1,000e0.012=1,020.20 USD. The strategy therefore gives rise to a riskless profit of 1,040.171,020.20=19.97 USD