can someone please help answer these questions A,B,C,D,E,F,G,H or at least a few of these questions. thankyou.

i have uploaded tax tables (UK) and other images to help. if i need to upload anything else to support please tell me in the comments.

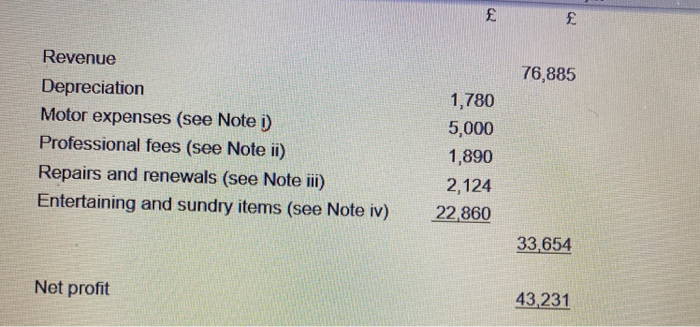

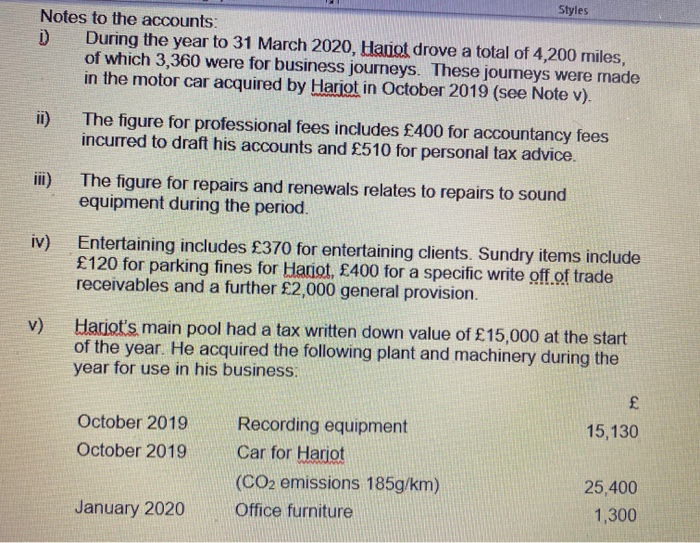

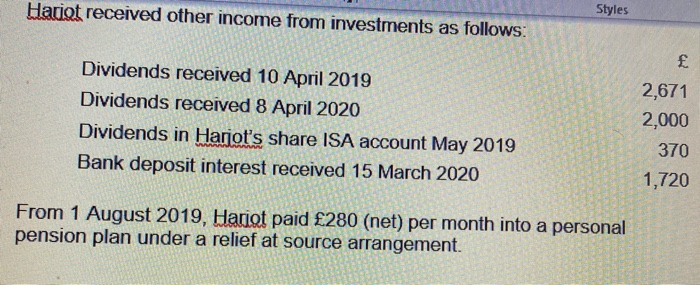

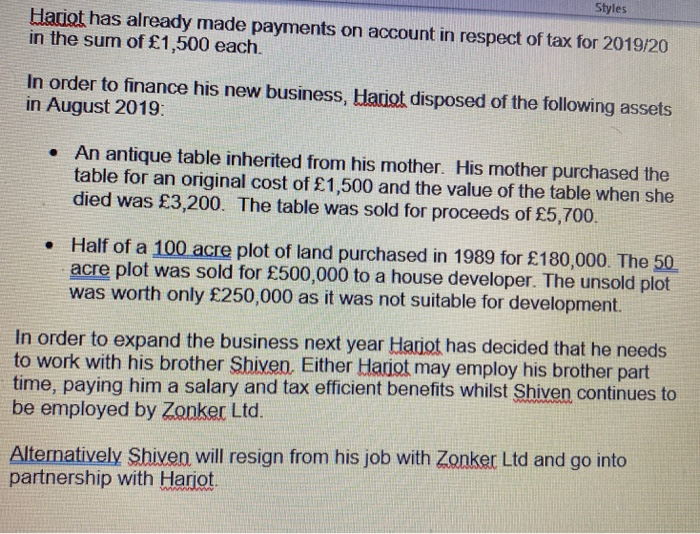

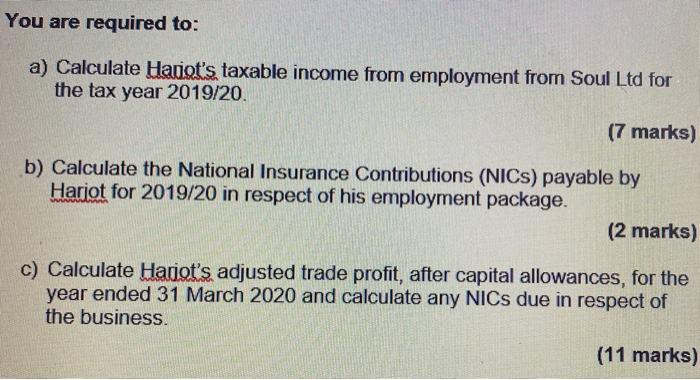

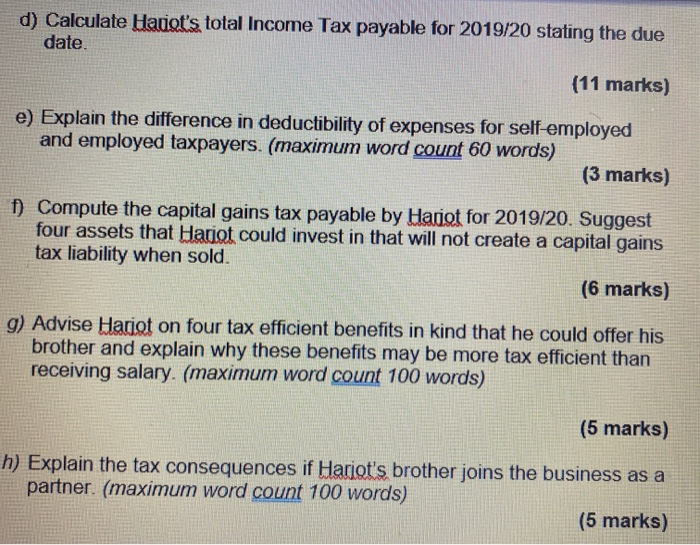

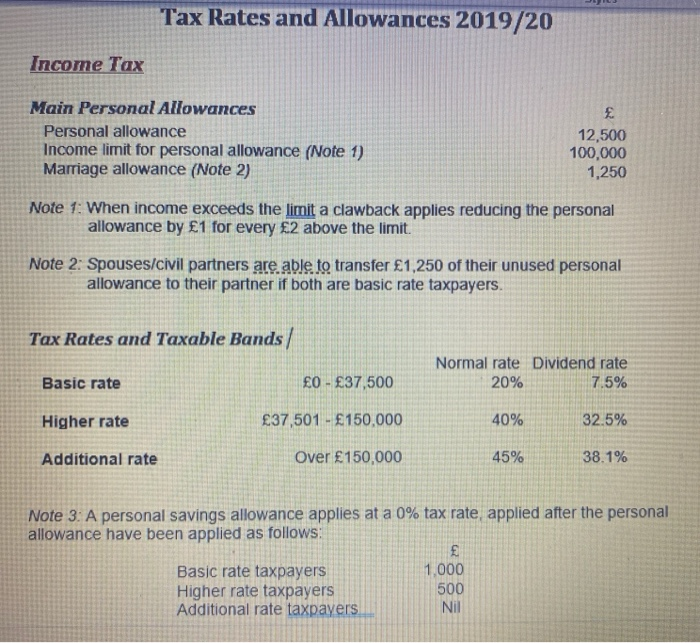

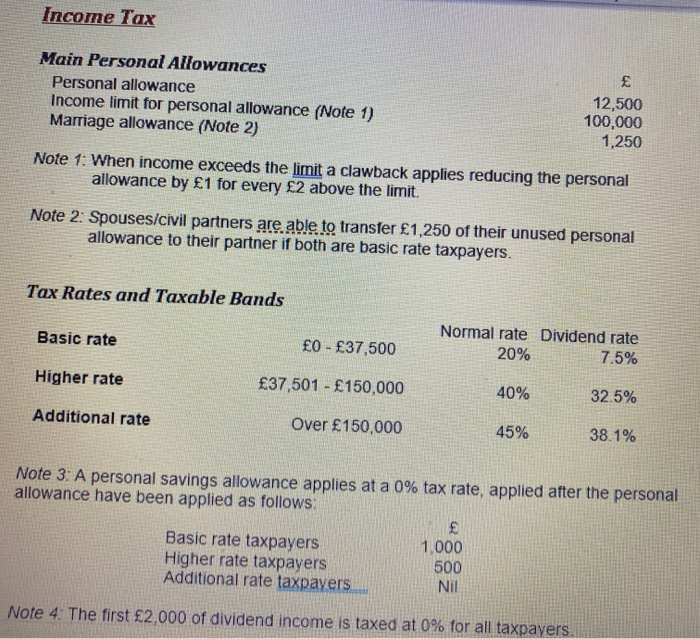

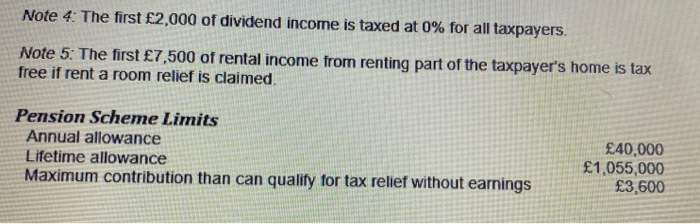

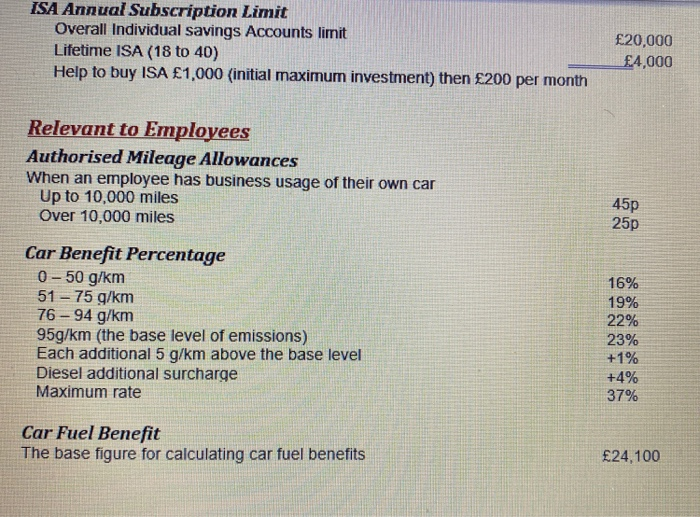

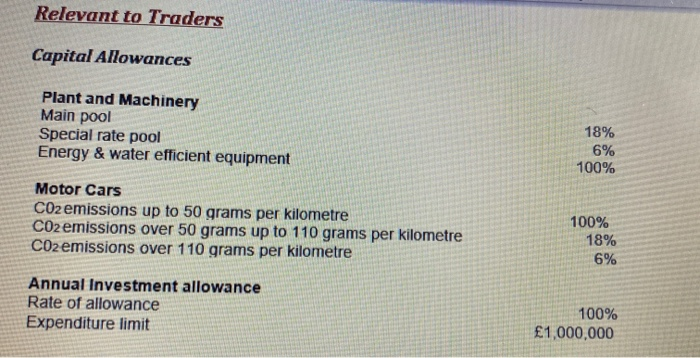

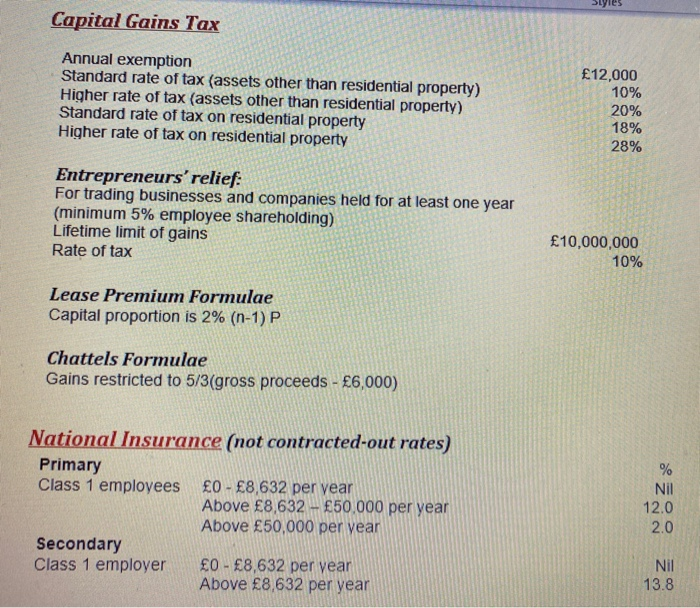

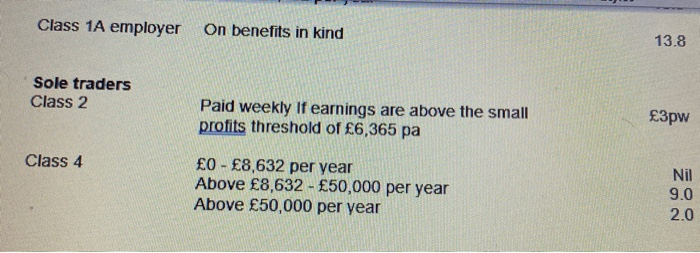

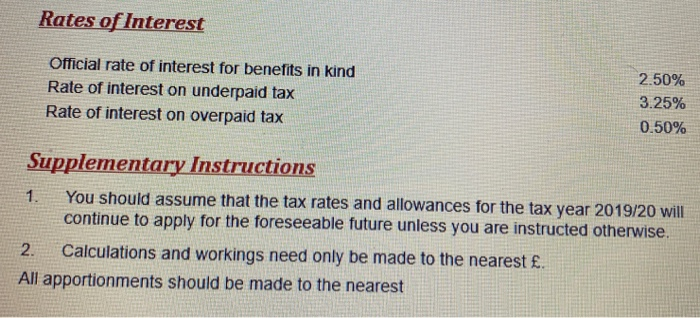

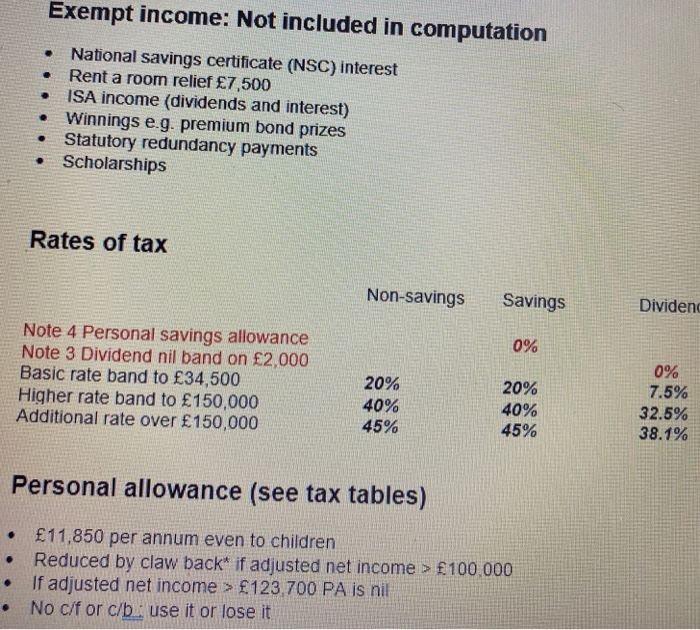

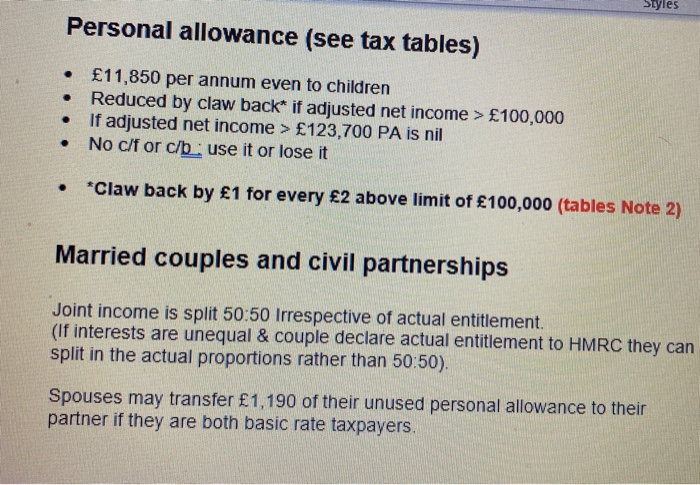

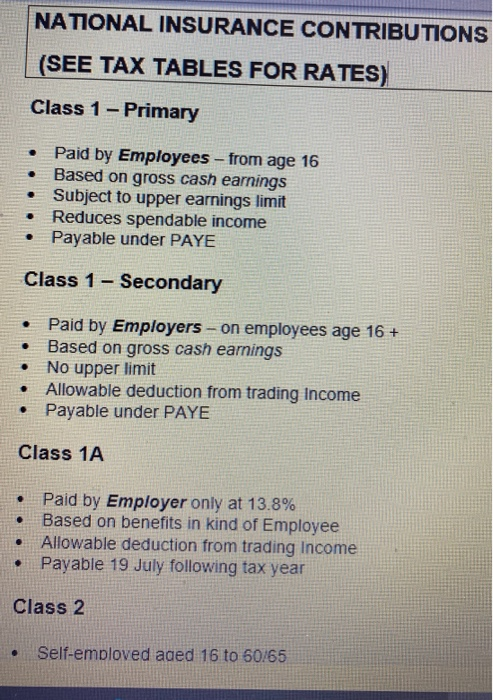

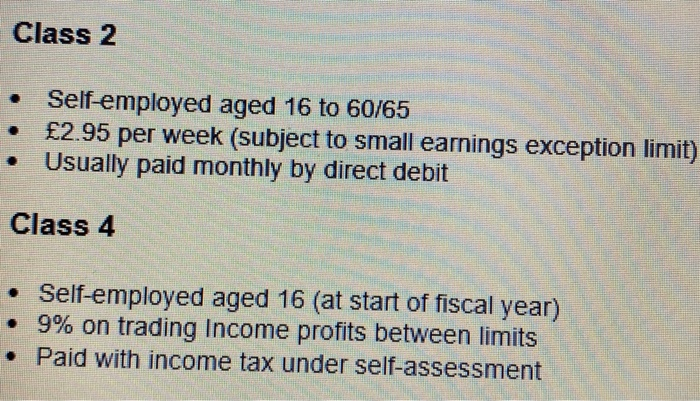

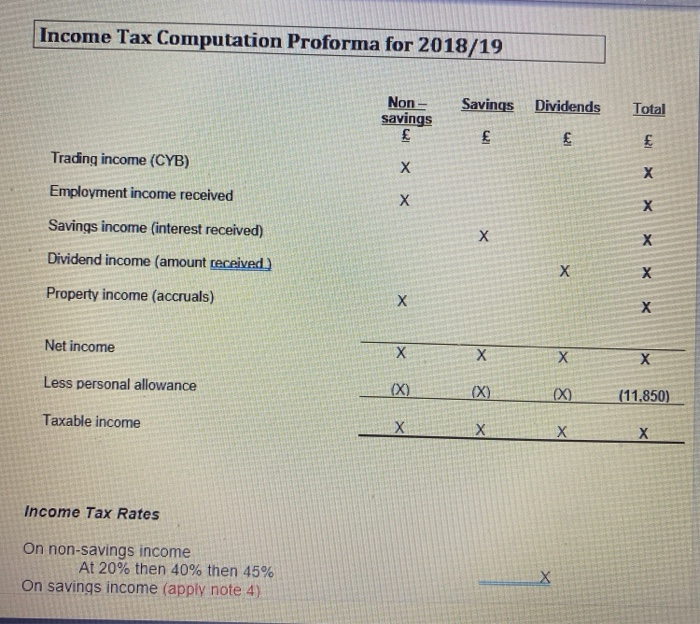

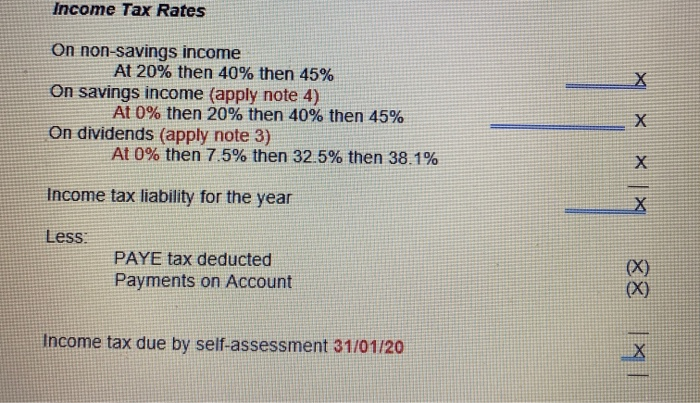

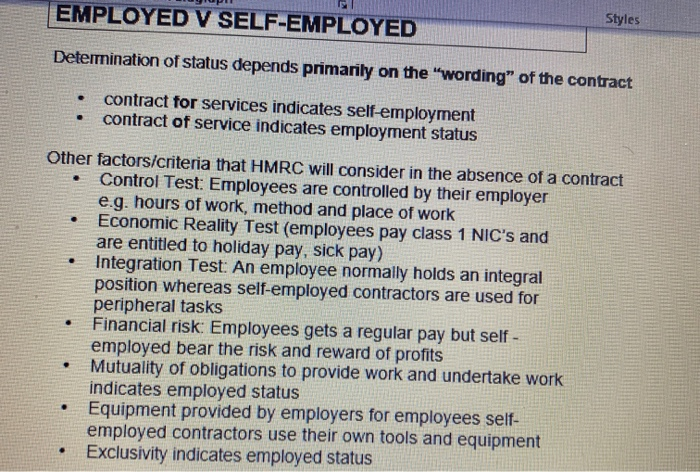

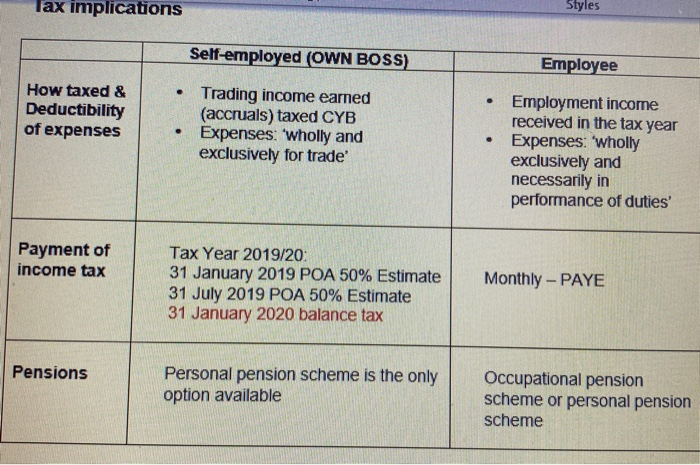

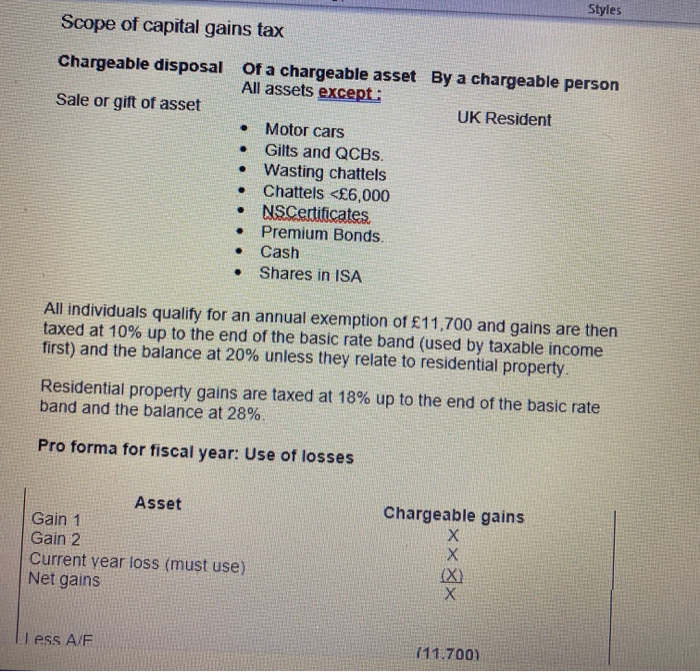

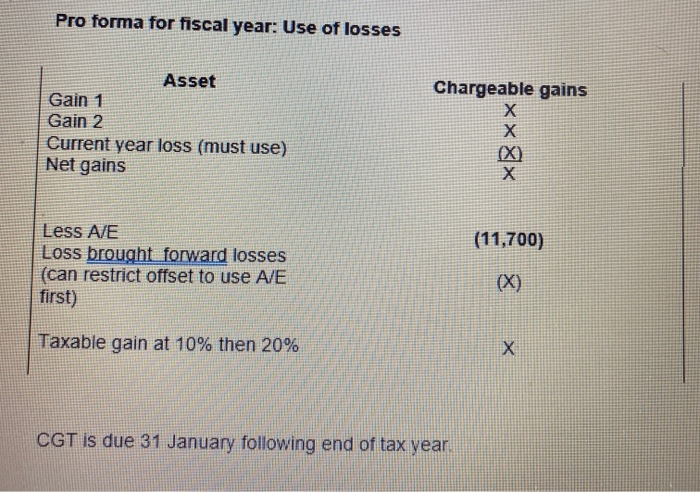

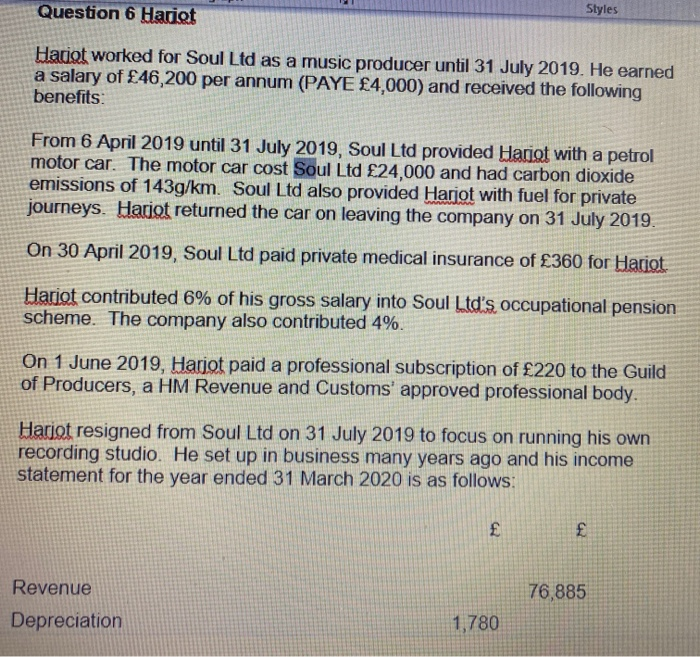

Question 6 Harigt Styles Hariat worked for Soul Ltd as a music producer until 31 July 2019. He earned a salary of 46,200 per annum (PAYE 4,000) and received the following benefits From 6 April 2019 until 31 July 2019, Soul Ltd provided Hariot with a petrol motor car. The motor car cost Soul Ltd 24,000 and had carbon dioxide emissions of 143g/km. Soul Ltd also provided Harjot with fuel for private journeys. Hariot returned the car on leaving the company on 31 July 2019. On 30 April 2019, Soul Ltd paid private medical insurance of 360 for Hariot Hariot contributed 6% of his gross salary into Soul Ltd's occupational pension scheme. The company also contributed 4%. On 1 June 2019, Harjot paid a professional subscription of 220 to the Guild of Producers, a HM Revenue and Customs' approved professional body. Hariat resigned from Soul Ltd on 31 July 2019 to focus on running his own recording studio. He set up in business many years ago and his income statement for the year ended 31 March 2020 is as follows: 76,885 Revenue Depreciation 1,780 76,885 Revenue Depreciation Motor expenses (see Note 1) Professional fees (see Note ii) Repairs and renewals (see Note iii) Entertaining and sundry items (see Note iv) 1,780 5,000 1,890 2,124 22.860 33,654 Net profit 43,231 Styles Notes to the accounts: D During the year to 31 March 2020, Haciat drove a total of 4,200 miles, of which 3,360 were for business journeys. These joumeys were made in the motor car acquired by Harjot in October 2019 (see Note v). ii) The figure for professional fees includes 400 for accountancy fees incurred to draft his accounts and 510 for personal tax advice. iii) The figure for repairs and renewals relates to repairs to sound equipment during the period. iv) Entertaining includes 370 for entertaining clients. Sundry items include 120 for parking fines for Hariot, 400 for a specific write off of trade receivables and a further 2,000 general provision. v) Hariot's main pool had a tax written down value of 15,000 at the start of the year. He acquired the following plant and machinery during the year for use in his business. October 2019 Recording equipment 15,130 October 2019 Car for Harjot (CO2 emissions 185g/km) 25,400 January 2020 Office furniture 1,300 Hariot received other income from investments as follows: Styles Dividends received 10 April 2019 Dividends received 8 April 2020 Dividends in Harjot's share ISA account May 2019 Bank deposit interest received 15 March 2020 2,671 2,000 370 1,720 From 1 August 2019, Hariot paid 280 (net) per month into a personal pension plan under a relief at source arrangement. Styles Haciat has already made payments on account in respect of tax for 2019/20 in the sum of 1,500 each. In order to finance his new business, Harigt disposed of the following assets in August 2019 An antique table inherited from his mother. His mother purchased the table for an original cost of 1,500 and the value of the table when she died was 3,200. The table was sold for proceeds of 5,700. Half of a 100 acre plot of land purchased in 1989 for 180,000. The 50 acre plot was sold for 500,000 to a house developer. The unsold plot was worth only 250,000 as it was not suitable for development. In order to expand the business next year Harjot has decided that he needs to work with his brother Shiven. Either Hariot may employ his brother part time, paying him a salary and tax efficient benefits whilst Shiven continues to be employed by Zonker Ltd. Alternatively Shiven will resign from his job with Zonker Ltd and go into partnership with Harjot. You are required to: a) Calculate Hariot's taxable income from employment from Soul Ltd for the tax year 2019/20 (7 marks) b) Calculate the National Insurance Contributions (NICs) payable by Harjot for 2019/20 in respect of his employment package. (2 marks) c) Calculate Hariot's adjusted trade profit, after capital allowances, for the year ended 31 March 2020 and calculate any NICs due in respect of the business. (11 marks) d) Calculate Hariot's total Income Tax payable for 2019/20 stating the due date. (11 marks) e) Explain the difference in deductibility of expenses for self-employed and employed taxpayers. (maximum word count 60 words) (3 marks) f) Compute the capital gains tax payable by Hariot for 2019/20. Suggest four assets that Hariot could invest in that will not create a capital gains tax liability when sold. (6 marks) g) Advise Hariot on four tax efficient benefits in kind that he could offer his brother and explain why these benefits may be more tax efficient than receiving salary. (maximum word count 100 words) (5 marks) h) Explain the tax consequences if Hariot's brother joins the business as a partner. (maximum word count 100 words) (5 marks) Tax Rates and Allowances 2019/20 Income Tax Main Personal Allowances Personal allowance Income limit for personal allowance (Note 1) Marriage allowance (Note 2) 12,500 100,000 1,250 Note 1: When income exceeds the limit a clawback applies reducing the personal allowance by 1 for every 2 above the limit. Note 2: Spouses/civil partners are able to transfer 1,250 of their unused personal allowance to their partner if both are basic rate taxpayers. Tax Rates and Taxable Bands / Normal rate Dividend rate 20% 7.5% Basic rate O - 37,500 Higher rate 37,501 - 150,000 40% 32.5% Additional rate Over 150,000 45% 38.1% Note 3. A personal savings allowance applies at a 0% tax rate applied after the personal allowance have been applied as follows: f Basic rate taxpayers 1,000 Higher rate taxpayers 500 Additional rate taxpayers Nil Income Tax Main Personal Allowances Personal allowance Income limit for personal allowance (Note 1) Marriage allowance (Note 2) 12,500 100,000 1,250 Note 1: When income exceeds the limit a clawback applies reducing the personal allowance by 1 for every 2 above the limit. Note 2: Spouses/civil partners are able to transfer 1,250 of their unused personal allowance to their partner if both are basic rate taxpayers. Tax Rates and Taxable Bands Basic rate 0 - 37,500 Normal rate Dividend rate 20% 7.5% Higher rate 37,501 - 150,000 40% 32.5% Additional rate Over 150,000 45% 38.1% Note 3: A personal savings allowance applies at a 0% tax rate, applied after the personal allowance have been applied as follows: $ Basic rate taxpayers 1,000 Higher rate taxpayers 500 Additional rate taxpayers Nil Note 4. The first 2,000 of dividend income is taxed at 0% for all taxpayers. Note 4: The first 2,000 of dividend income is taxed at 0% for all taxpayers. Note 5: The first 7,500 of rental income from renting part of the taxpayer's home is tax free if rent a room relief is claimed Pension Scheme Limits Annual allowance Lifetime allowance Maximum contribution than can qualify for tax relief without earnings 40,000 1,055,000 3,600 ISA Annual Subscription Limit Overall Individual savings Accounts limit Lifetime ISA (18 to 40) Help to buy ISA 1,000 (initial maximum investment) then 200 per month 20,000 4,000 Relevant to Employees Authorised Mileage Allowances When an employee has business usage of their own car Up to 10,000 miles Over 10,000 miles 45p 25p Car Benefit Percentage 0-50 g/km 51 - 75 g/km 76 - 94 g/km 95g/km (the base level of emissions) Each additional 5 g/km above the base level Diesel additional surcharge Maximum rate 16% 19% 22% 23% +1% +4% 37% Car Fuel Benefit The base figure for calculating car fuel benefits 24,100 Relevant to Traders Capital Allowances Plant and Machinery Main pool Special rate pool Energy & water efficient equipment 18% 6% 100% Motor Cars CO2 emissions up to 50 grams per kilometre CO2 emissions over 50 grams up to 110 grams per kilometre CO2 emissions over 110 grams per kilometre 100% 18% 6% Annual Investment allowance Rate of allowance Expenditure limit 100% 1,000,000 Capital Gains Tax Annual exemption Standard rate of tax (assets other than residential property) Higher rate of tax (assets other than residential property) Standard rate of tax on residential property Higher rate of tax on residential property 12,000 10% 20% 18% 28% Entrepreneurs' relief: For trading businesses and companies held for at least one year (minimum 5% employee shareholding) Lifetime limit of gains Rate of tax 10,000,000 10% Lease Premium Formulae Capital proportion is 2% (n-1) P Chattels Formulae Gains restricted to 5/3(gross proceeds - 6,000) National Insurance (not contracted-out rates) Primary Class 1 employees 0 - 8,632 per year Above 8,632 - 50,000 per year Above 50,000 per year Secondary Class 1 employer 0 - 8,632 per year Above 8,632 per year % Nil 12.0 2.0 Nil 13.8 Class 1A employer On benefits in kind 13.8 Sole traders Class 2 Paid weekly If earnings are above the small profits threshold of 6,365 pa 3pw Class 4 0 - 8,632 per year Above 8,632 - 50,000 per year Above 50,000 per year Nil 9.0 2.0 Rates of Interest Official rate of interest for benefits in kind Rate of interest on underpaid tax Rate of interest on overpaid tax 2.50% 3.25% 0.50% Supplementary Instructions 1. You should assume that the tax rates and allowances for the tax year 2019/20 will continue to apply for the foreseeable future unless you are instructed otherwise, 2. Calculations and workings need only be made to the nearest . All apportionments should be made to the nearest Exempt income: Not included in computation . National savings certificate (NSC) interest Rent a room relief 7,500 ISA income (dividends and interest) Winnings e.g. premium bond prizes Statutory redundancy payments Scholarships . Rates of tax Non-savings Savings Dividend 0% Note 4 Personal savings allowance Note 3 Dividend nil band on 2,000 Basic rate band to 34,500 Higher rate band to 150,000 Additional rate over 150,000 20% 40% 45% 20% 40% 45% 0% 7.5% 32.5% 38.1% Personal allowance (see tax tables) . 11,850 per annum even to children Reduced by claw back* if adjusted net income > 100.000 If adjusted net income > 123,700 PA is nil No c/f or c/ buse it or lose it Styles Personal allowance (see tax tables) . 11,850 per annum even to children Reduced by claw back* if adjusted net income > 100,000 If adjusted net income > 123,700 PA is nil No c/f or c/ buse it or lose it . * Claw back by 1 for every 2 above limit of 100,000 (tables Note 2) Married couples and civil partnerships Joint income is split 50:50 Irrespective of actual entitlement. (If interests are unequal & couple declare actual entitlement to HMRC they can split in the actual proportions rather than 50:50). Spouses may transfer 1,190 of their unused personal allowance to their partner if they are both basic rate taxpayers. NATIONAL INSURANCE CONTRIBUTIONS (SEE TAX TABLES FOR RATES) Class 1 - Primary Paid by Employees - from age 16 Based on gross cash earnings Subject to upper earnings limit Reduces spendable income Payable under PAYE Class 1 - Secondary Paid by Employers - on employees age 16+ Based on gross cash earnings No upper limit Allowable deduction from trading Income Payable under PAYE . . Class 1A Paid by Employer only at 13.8% Based on benefits in kind of Employee Allowable deduction from trading Income Payable 19 July following tax year . Class 2 Self-emploved aged 16 to 50/65 Class 2 Self-employed aged 16 to 60/65 2.95 per week (subject to small earnings exception limit) Usually paid monthly by direct debit Class 4 Self-employed aged 16 (at start of fiscal year) 9% on trading Income profits between limits Paid with income tax under self-assessment Income Tax Computation Proforma for 2018/19 Savings Dividends Total Non- savings Trading income (CYB) X Employment income received X X Savings income interest received) X Dividend income (amount received X X Property income (accruals) X X Net income X X X Less personal allowance (X) (X) (11.850) Taxable income X Income Tax Rates On non-savings income At 20% then 40% then 45% On savings income (apply note 4) Income Tax Rates On non-savings income At 20% then 40% then 45% On savings income (apply note 4) At 0% then 20% then 40% then 45% On dividends (apply note 3) At 0% then 7.5% then 32.5% then 38.1% X Income tax liability for the year X Less PAYE tax deducted Payments on Account (X) (X) Income tax due by self-assessment 31/01/20 X EMPLOYED V SELF-EMPLOYED Styles Determination of status depends primarily on the "wording" of the contract contract for services indicates self-employment contract of service indicates employment status Other factors/criteria that HMRC will consider in the absence of a contract Control Test: Employees are controlled by their employer e.g. hours of work, method and place of work Economic Reality Test (employees pay class 1 NIC's and are entitled to holiday pay, sick pay) Integration Test: An employee normally holds an integral position whereas self-employed contractors are used for peripheral tasks Financial risk: Employees gets a regular pay but self- employed bear the risk and reward of profits Mutuality of obligations to provide work and undertake work indicates employed status Equipment provided by employers for employees self- employed contractors use their own tools and equipment Exclusivity indicates employed status . . Tax implications Styles Self-employed (OWN BOSS) Employee . How taxed & Deductibility of expenses Trading income earned (accruals) taxed CYB Expenses: 'wholly and exclusively for trade . . Employment income received in the tax year Expenses: 'wholly exclusively and necessarily in performance of duties' Payment of income tax Tax Year 2019/20 31 January 2019 POA 50% Estimate 31 July 2019 POA 50% Estimate 31 January 2020 balance tax Monthly - PAYE Pensions Personal pension scheme is the only option available Occupational pension scheme or personal pension scheme Styles Scope of capital gains tax . Chargeable disposal of a chargeable asset By a chargeable person All assets except: Sale or gift of asset UK Resident Motor cars Gilts and QCBs. Wasting chattels Chattels 100.000 If adjusted net income > 123,700 PA is nil No c/f or c/ buse it or lose it Styles Personal allowance (see tax tables) . 11,850 per annum even to children Reduced by claw back* if adjusted net income > 100,000 If adjusted net income > 123,700 PA is nil No c/f or c/ buse it or lose it . * Claw back by 1 for every 2 above limit of 100,000 (tables Note 2) Married couples and civil partnerships Joint income is split 50:50 Irrespective of actual entitlement. (If interests are unequal & couple declare actual entitlement to HMRC they can split in the actual proportions rather than 50:50). Spouses may transfer 1,190 of their unused personal allowance to their partner if they are both basic rate taxpayers. NATIONAL INSURANCE CONTRIBUTIONS (SEE TAX TABLES FOR RATES) Class 1 - Primary Paid by Employees - from age 16 Based on gross cash earnings Subject to upper earnings limit Reduces spendable income Payable under PAYE Class 1 - Secondary Paid by Employers - on employees age 16+ Based on gross cash earnings No upper limit Allowable deduction from trading Income Payable under PAYE . . Class 1A Paid by Employer only at 13.8% Based on benefits in kind of Employee Allowable deduction from trading Income Payable 19 July following tax year . Class 2 Self-emploved aged 16 to 50/65 Class 2 Self-employed aged 16 to 60/65 2.95 per week (subject to small earnings exception limit) Usually paid monthly by direct debit Class 4 Self-employed aged 16 (at start of fiscal year) 9% on trading Income profits between limits Paid with income tax under self-assessment Income Tax Computation Proforma for 2018/19 Savings Dividends Total Non- savings Trading income (CYB) X Employment income received X X Savings income interest received) X Dividend income (amount received X X Property income (accruals) X X Net income X X X Less personal allowance (X) (X) (11.850) Taxable income X Income Tax Rates On non-savings income At 20% then 40% then 45% On savings income (apply note 4) Income Tax Rates On non-savings income At 20% then 40% then 45% On savings income (apply note 4) At 0% then 20% then 40% then 45% On dividends (apply note 3) At 0% then 7.5% then 32.5% then 38.1% X Income tax liability for the year X Less PAYE tax deducted Payments on Account (X) (X) Income tax due by self-assessment 31/01/20 X EMPLOYED V SELF-EMPLOYED Styles Determination of status depends primarily on the "wording" of the contract contract for services indicates self-employment contract of service indicates employment status Other factors/criteria that HMRC will consider in the absence of a contract Control Test: Employees are controlled by their employer e.g. hours of work, method and place of work Economic Reality Test (employees pay class 1 NIC's and are entitled to holiday pay, sick pay) Integration Test: An employee normally holds an integral position whereas self-employed contractors are used for peripheral tasks Financial risk: Employees gets a regular pay but self- employed bear the risk and reward of profits Mutuality of obligations to provide work and undertake work indicates employed status Equipment provided by employers for employees self- employed contractors use their own tools and equipment Exclusivity indicates employed status . . Tax implications Styles Self-employed (OWN BOSS) Employee . How taxed & Deductibility of expenses Trading income earned (accruals) taxed CYB Expenses: 'wholly and exclusively for trade . . Employment income received in the tax year Expenses: 'wholly exclusively and necessarily in performance of duties' Payment of income tax Tax Year 2019/20 31 January 2019 POA 50% Estimate 31 July 2019 POA 50% Estimate 31 January 2020 balance tax Monthly - PAYE Pensions Personal pension scheme is the only option available Occupational pension scheme or personal pension scheme Styles Scope of capital gains tax . Chargeable disposal of a chargeable asset By a chargeable person All assets except: Sale or gift of asset UK Resident Motor cars Gilts and QCBs. Wasting chattels Chattels