can someone please help out

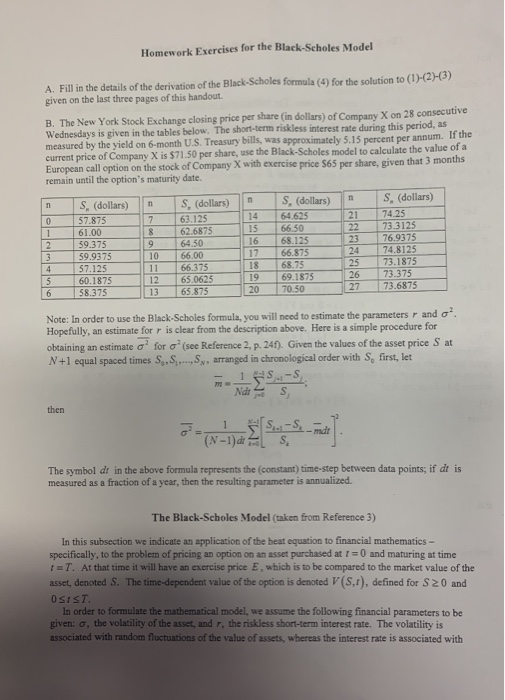

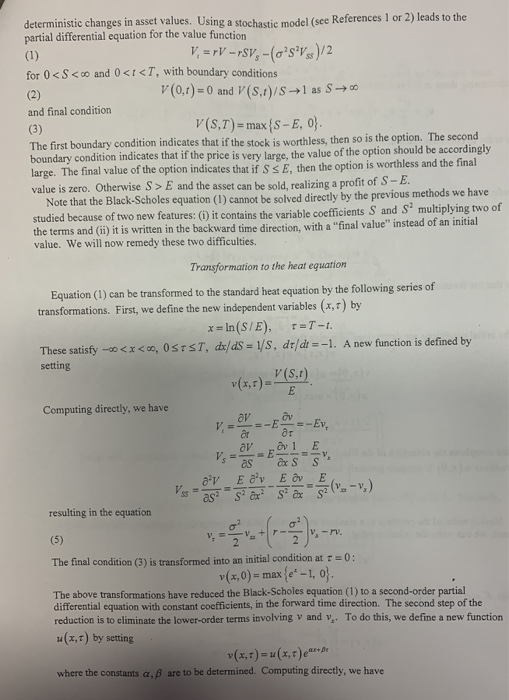

The Black-Scholes Model for Valuation of Stock Options References: 1. Fischer Black and Myron Scholes, "The pricing of options and corporate liabilities". Journal of Political Economy, 81 (1973). 637-654. 2. P. Wilmott, S. Howison, and J. Dewynne, The Mathematics of Financial Derivatives. Cambridge University Press, New York, 1995. 3. M. Pinsky, Partial Differential Equations and Boundary Value Problems with Applications, McGraw-Hill Company, New York, 1984 Definition: A European call option is a security giving the holder the right, but not the obligation, to buy a single share of a specific stock at a specified price E on a specified future date T. E is called the exercise (or strike) price and T is called the maturity (or expiration) date of the option Let V=V(S.1) denote the value of the (European call option at time I (0,7) if the current market value of the stock is S dollars per share. If r denotes the constant) short-term riskless interest rate and o denotes the "volatility parameter of the stock's price per share, then Black and Scholes showed that V satisfies the partial differential equation V = -V - SV -('s Vs)/2 for 0

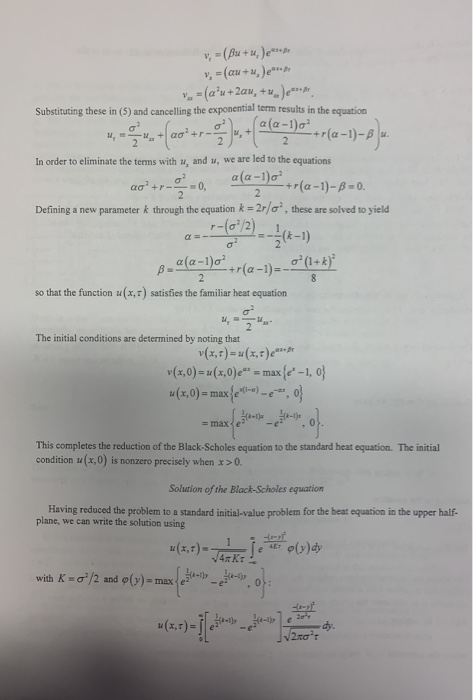

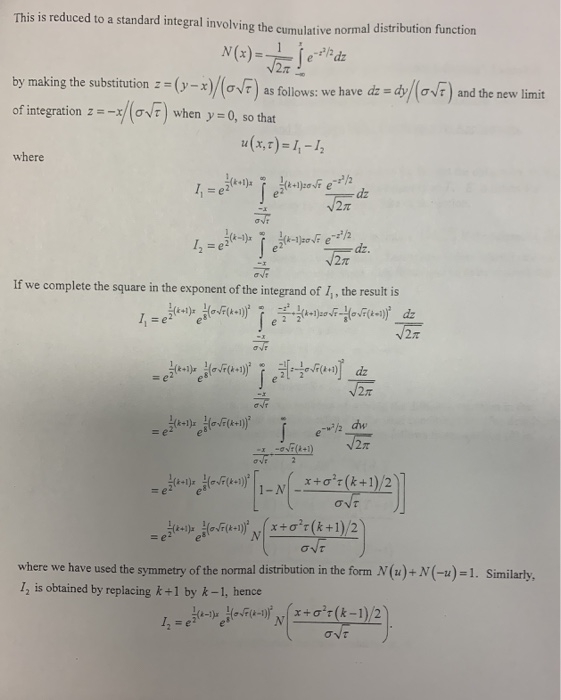

E and the asset can be sold, realizing a profit of S-E. Note that the Black-Scholes equation (1) cannot be solved directly by the previous methods we have studied because of two new features: (i) it contains the variable coefficients S and S multiplying two of the terms and (ii) it is written in the backward time direction with a "final value" instead of an initial value. We will now remedy these two difficulties. Transformation to the heat equation Equation (1) can be transformed to the standard heat equation by the following series of transformations. First, we define the new independent variables (x,T) by x = ln(S/E), r=1-1. These satisfy - 0 0. Solution of the Black-Scholes equation Having reduced the problem to a standard initial-value problem for the heat equation in the upper half- plane, we can write the solution using (3,7)- with K = 0/2 and (y) max je oly)dy This is reduced to a standard integral involving the cumulative normal distribution function N(x) = bajerledz by making the substitution ==(y=x)/(OVF) as follows: we have dz = dy/(OVT) and the new limit of integration z = -x/(OVT) when y = 0, so that u(x, 7) = 1, - 1 I, ezkut) e-l)zovi e 2/2 -dz where on 27 1, 3-1 3-1: Vi e--1/2 If we complete the square in the exponent of the integrand of I, the result is 1. = e(+1) Hot(2-1) -1):37-HOW(2-1)dz 27 ezte) Hova(+1) dz 2. HotFile-1) I 2 - to, jump --- - **0*74+1)/2) e) HOW(+1)*(x+or(k+1)/2 or where we have used the symmetry of the normal distribution in the form N(u)+N(-u)=1. Similarly, 1, is obtained by replacing k +1 by k-1, hence 1, e34e-) Hof(2-1)(x+o+=(k-1)/2 OVE The Black-Scholes Model for Valuation of Stock Options References: 1. Fischer Black and Myron Scholes, "The pricing of options and corporate liabilities". Journal of Political Economy, 81 (1973). 637-654. 2. P. Wilmott, S. Howison, and J. Dewynne, The Mathematics of Financial Derivatives. Cambridge University Press, New York, 1995. 3. M. Pinsky, Partial Differential Equations and Boundary Value Problems with Applications, McGraw-Hill Company, New York, 1984 Definition: A European call option is a security giving the holder the right, but not the obligation, to buy a single share of a specific stock at a specified price E on a specified future date T. E is called the exercise (or strike) price and T is called the maturity (or expiration) date of the option Let V=V(S.1) denote the value of the (European call option at time I (0,7) if the current market value of the stock is S dollars per share. If r denotes the constant) short-term riskless interest rate and o denotes the "volatility parameter of the stock's price per share, then Black and Scholes showed that V satisfies the partial differential equation V = -V - SV -('s Vs)/2 for 0 E and the asset can be sold, realizing a profit of S-E. Note that the Black-Scholes equation (1) cannot be solved directly by the previous methods we have studied because of two new features: (i) it contains the variable coefficients S and S multiplying two of the terms and (ii) it is written in the backward time direction with a "final value" instead of an initial value. We will now remedy these two difficulties. Transformation to the heat equation Equation (1) can be transformed to the standard heat equation by the following series of transformations. First, we define the new independent variables (x,T) by x = ln(S/E), r=1-1. These satisfy - 0 0. Solution of the Black-Scholes equation Having reduced the problem to a standard initial-value problem for the heat equation in the upper half- plane, we can write the solution using (3,7)- with K = 0/2 and (y) max je oly)dy This is reduced to a standard integral involving the cumulative normal distribution function N(x) = bajerledz by making the substitution ==(y=x)/(OVF) as follows: we have dz = dy/(OVT) and the new limit of integration z = -x/(OVT) when y = 0, so that u(x, 7) = 1, - 1 I, ezkut) e-l)zovi e 2/2 -dz where on 27 1, 3-1 3-1: Vi e--1/2 If we complete the square in the exponent of the integrand of I, the result is 1. = e(+1) Hot(2-1) -1):37-HOW(2-1)dz 27 ezte) Hova(+1) dz 2. HotFile-1) I 2 - to, jump --- - **0*74+1)/2) e) HOW(+1)*(x+or(k+1)/2 or where we have used the symmetry of the normal distribution in the form N(u)+N(-u)=1. Similarly, 1, is obtained by replacing k +1 by k-1, hence 1, e34e-) Hof(2-1)(x+o+=(k-1)/2 OVE