Answered step by step

Verified Expert Solution

Question

1 Approved Answer

can the guy who solved my question answer the rest of these the exact same way (through excel) thanks Answer 9-14 through excel and show

can the guy who solved my question answer the rest of these the exact same way (through excel)

thanks

Answer 9-14 through excel and show work with formulas

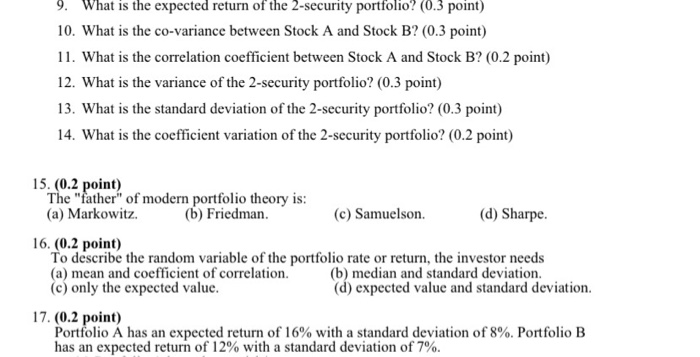

9. What is the expected return of the 2-security portfolio? (0.3 point) 10. What is the co-variance between Stock A and Stock B? (0.3 point) 11. What is the correlation coefficient between Stock A and Stock B? (0.2 point) 12. What is the variance of the 2-security portfolio? (0.3 point) 13. What is the standard deviation of the 2-security portfolio? (0.3 point) 14. What is the coefficient variation of the 2-security portfolio? (0.2 point) 15. (0.2 point) The "father" of modern portfolio theory is: (a) Markowitz. (b) Friedman (c) Samuelson. (d) Sharpe. 16. (0.2 point) To describe the random variable of the portfolio rate or return, the investor needs (a) mean and coefficient of correlation. (b) median and standard deviation. (c) only the expected value. (d) expected value and standard deviation. 17. (0.2 point) Portfolio has an expected return of 16% with a standard deviation of 8%. Portfolio B has an expected return of 12% with a standard deviation of 7%. 11:10 LTE Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management For Nurse Managers Merging The Heart With The Dollar Merging The Heart With The Dollar

Authors: J. Michael Leger, Janne Dunham-Taylor

4th Edition

1284127257, 978-1284127256