can you explain how to make the table its asking me to on C. its telling me to make it similar to ex. 9.16 from the textbook which i posted a picture of.

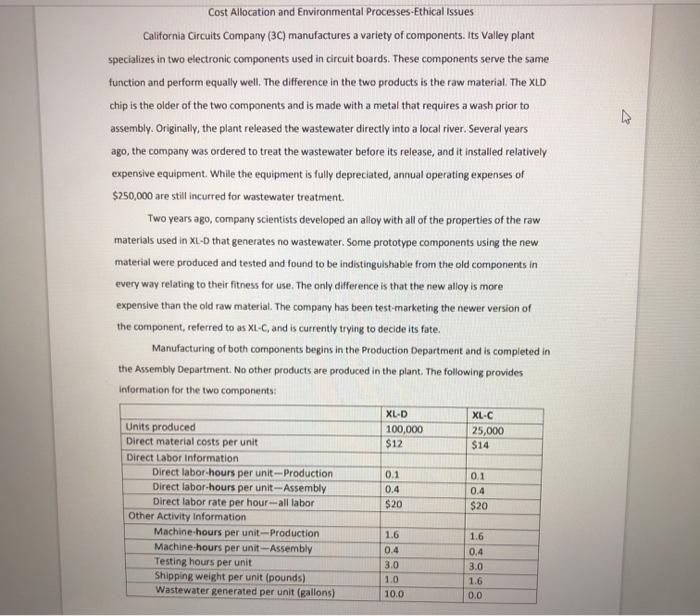

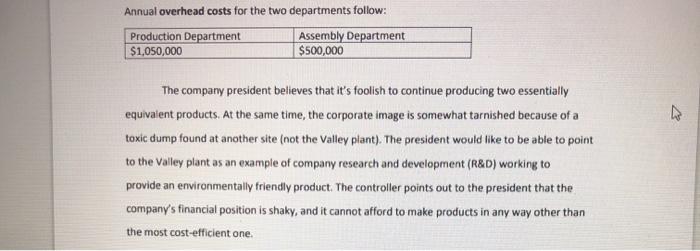

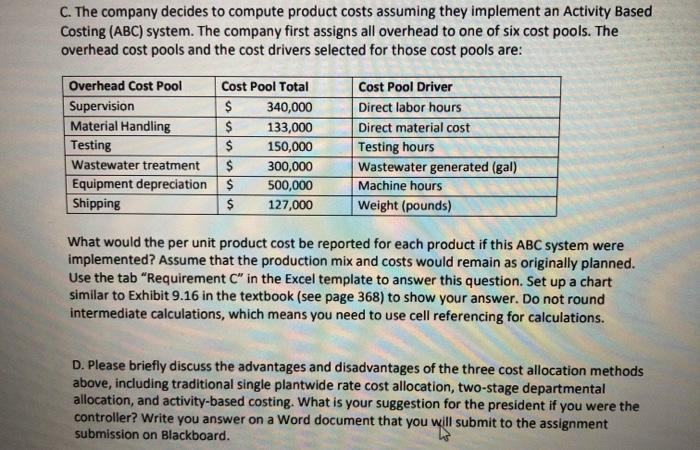

Cost Allocation and Environmental Processes-Ethical Issues California Circuits Company (3C) manufactures a variety of components. Its Valley plant specializes in two electronic components used in circuit boards. These components serve the same function and perform equally well. The difference in the two products is the raw material. The XLD chip is the older of the two components and is made with a metal that requires a wash prior to assembly. Originally, the plant released the wastewater directly into a local river. Several years ago, the company was ordered to treat the wastewater before its release, and it installed relatively expensive equipment. While the equipment is fully depreciated, annual operating expenses of $250,000 are still incurred for wastewater treatment Two years ago, company scientists developed an alloy with all of the properties of the raw materials used in XL-D that generates no wastewater. Some prototype components using the new material were produced and tested and found to be indistinguishable from the old components in every way relating to their fitness for use. The only difference is that the new alloy is more expensive than the old raw material. The company has been test marketing the newer version of the component, referred to as XL-C, and is currently trying to decide its fate. Manufacturing of both components begins in the Production Department and is completed in the Assembly Department. No other products are produced in the plant. The following provides Information for the two components: XL-D XL-C Units produced 100,000 25,000 Direct material costs per unit $12 $14 Direct Labor information Direct labor hours per unit-Production Direct labor-hours per unit--Assembly Direct labor rate per hour - all labor $20 Other Activity Information Machine hours per unit-Production Machine-hours per unit-Assembly Testing hours per unit Shipping weight per unit (pounds) Wastewater generated per unit (Ballons) 0.1 0.4 0.1 0.4 $20 1.6 1.6 0.4 3.0 1.0 10.0 0.4 3.0 1.6 0.0 Annual overhead costs for the two departments follow: Production Department Assembly Department $1,050,000 $500,000 The company president believes that it's foolish to continue producing two essentially equivalent products. At the same time, the corporate image is somewhat tarnished because of a toxic dump found at another site (not the Valley plant). The president would like to be able to point to the Valley plant as an example of company research and development (R&D) working to provide an environmentally friendly product. The controller points out to the president that the company's financial position is shaky, and it cannot afford to make products in any way other than the most cost-efficient one C. The company decides to compute product costs assuming they implement an Activity Based Costing (ABC) system. The company first assigns all overhead to one of six cost pools. The overhead cost pools and the cost drivers selected for those cost pools are: Overhead Cost Pool Cost Pool Total Supervision $ 340,000 Material Handling $ 133,000 Testing $ 150,000 Wastewater treatment $ 300,000 Equipment depreciation $ 500,000 Shipping $ 127,000 Cost Pool Driver Direct labor hours Direct material cost Testing hours Wastewater generated (gal) Machine hours Weight (pounds) What would the per unit product cost be reported for each product if this ABC system were implemented? Assume that the production mix and costs would remain as originally planned. Use the tab "Requirement C" in the Excel template to answer this question. Set up a chart similar to Exhibit 9.16 in the textbook (see page 368) to show your answer. Do not round intermediate calculations, which means you need to use cell referencing for calculations. D. Please briefly discuss the advantages and disadvantages of the three cost allocation methods above, including traditional single plantwide rate cost allocation, two-stage departmental allocation, and activity-based costing. What is your suggestion for the president if you were the controller? Write you answer on a Word document that you will submit to the assignment submission on Blackboard. Using the information in the cost flow diagram, Nancy assigns costs to the two products. The direct costs, material and labor, are, of course, the same as in the original system and the two-stage system described earlier in the chapter. There is a difference, however, in the assignment of overhead costs. No longer can Nancy multiply the number of units of the cost driver in a unit of product by the cost driver rate because not all cost drivers are identified at the unit level (i.e., they are not all volume related). In the production cost report that Nancy prepares ( Exhibit 9.16), she first calculates the total cost of production for each product and then divides the total cost by the number of units produced to arrive at the unit cost. She could also have calculated the cost driver rate per unit of product for each of the cost drivers and then calculated the unit cost of the product directly. Page 368 Exhibit 9.16 Third Quarter Unit Cost Report, Activity-Based Costing-CenterPoint Manufacturing Facility Exhibit 9.16 Third Quarter Unit Cost Report, Activity-Based Costing-CenterPoint Manufacturing Facility B A Sport Pro 1 2 S 1,500,000 $ 2,400,000 3. Direct material 4 Direct labor 5 Assembly $750,000 $ 600.000 6 Packaging 990,000 360,000 7 Total direct labor $ 1,740,000 $ 960,000 8 Direct costs $ 3.240,000 $ 3,360,000 9 Overhead 10 Assembly building 11 Assembling @ $ 30 per MH) $ 180,000 $ 900.000 12 Setting up machines (@ $ 900 per setup hour) 36,000 360,000 13 Handling material (@$ 3,000 per run) 24.000 120,000 14 Packaging building 15 Inspecting and packing (@ $5 per direct labor-hour) 300,000 114.000 16 Shipping (@$ 1.320 per shipment) 132.000 264.000 17 Total ABC overhead S672.000 $ 1.758,000 18 Total ABC cost $ 3,912.000 $ 5.118.000 19 Number of units 100,000 40.000 21 39.12 $ 127.95 20 Unit cost Cost Allocation and Environmental Processes-Ethical Issues California Circuits Company (3C) manufactures a variety of components. Its Valley plant specializes in two electronic components used in circuit boards. These components serve the same function and perform equally well. The difference in the two products is the raw material. The XLD chip is the older of the two components and is made with a metal that requires a wash prior to assembly. Originally, the plant released the wastewater directly into a local river. Several years ago, the company was ordered to treat the wastewater before its release, and it installed relatively expensive equipment. While the equipment is fully depreciated, annual operating expenses of $250,000 are still incurred for wastewater treatment Two years ago, company scientists developed an alloy with all of the properties of the raw materials used in XL-D that generates no wastewater. Some prototype components using the new material were produced and tested and found to be indistinguishable from the old components in every way relating to their fitness for use. The only difference is that the new alloy is more expensive than the old raw material. The company has been test marketing the newer version of the component, referred to as XL-C, and is currently trying to decide its fate. Manufacturing of both components begins in the Production Department and is completed in the Assembly Department. No other products are produced in the plant. The following provides Information for the two components: XL-D XL-C Units produced 100,000 25,000 Direct material costs per unit $12 $14 Direct Labor information Direct labor hours per unit-Production Direct labor-hours per unit--Assembly Direct labor rate per hour - all labor $20 Other Activity Information Machine hours per unit-Production Machine-hours per unit-Assembly Testing hours per unit Shipping weight per unit (pounds) Wastewater generated per unit (Ballons) 0.1 0.4 0.1 0.4 $20 1.6 1.6 0.4 3.0 1.0 10.0 0.4 3.0 1.6 0.0 Annual overhead costs for the two departments follow: Production Department Assembly Department $1,050,000 $500,000 The company president believes that it's foolish to continue producing two essentially equivalent products. At the same time, the corporate image is somewhat tarnished because of a toxic dump found at another site (not the Valley plant). The president would like to be able to point to the Valley plant as an example of company research and development (R&D) working to provide an environmentally friendly product. The controller points out to the president that the company's financial position is shaky, and it cannot afford to make products in any way other than the most cost-efficient one C. The company decides to compute product costs assuming they implement an Activity Based Costing (ABC) system. The company first assigns all overhead to one of six cost pools. The overhead cost pools and the cost drivers selected for those cost pools are: Overhead Cost Pool Cost Pool Total Supervision $ 340,000 Material Handling $ 133,000 Testing $ 150,000 Wastewater treatment $ 300,000 Equipment depreciation $ 500,000 Shipping $ 127,000 Cost Pool Driver Direct labor hours Direct material cost Testing hours Wastewater generated (gal) Machine hours Weight (pounds) What would the per unit product cost be reported for each product if this ABC system were implemented? Assume that the production mix and costs would remain as originally planned. Use the tab "Requirement C" in the Excel template to answer this question. Set up a chart similar to Exhibit 9.16 in the textbook (see page 368) to show your answer. Do not round intermediate calculations, which means you need to use cell referencing for calculations. D. Please briefly discuss the advantages and disadvantages of the three cost allocation methods above, including traditional single plantwide rate cost allocation, two-stage departmental allocation, and activity-based costing. What is your suggestion for the president if you were the controller? Write you answer on a Word document that you will submit to the assignment submission on Blackboard. Using the information in the cost flow diagram, Nancy assigns costs to the two products. The direct costs, material and labor, are, of course, the same as in the original system and the two-stage system described earlier in the chapter. There is a difference, however, in the assignment of overhead costs. No longer can Nancy multiply the number of units of the cost driver in a unit of product by the cost driver rate because not all cost drivers are identified at the unit level (i.e., they are not all volume related). In the production cost report that Nancy prepares ( Exhibit 9.16), she first calculates the total cost of production for each product and then divides the total cost by the number of units produced to arrive at the unit cost. She could also have calculated the cost driver rate per unit of product for each of the cost drivers and then calculated the unit cost of the product directly. Page 368 Exhibit 9.16 Third Quarter Unit Cost Report, Activity-Based Costing-CenterPoint Manufacturing Facility Exhibit 9.16 Third Quarter Unit Cost Report, Activity-Based Costing-CenterPoint Manufacturing Facility B A Sport Pro 1 2 S 1,500,000 $ 2,400,000 3. Direct material 4 Direct labor 5 Assembly $750,000 $ 600.000 6 Packaging 990,000 360,000 7 Total direct labor $ 1,740,000 $ 960,000 8 Direct costs $ 3.240,000 $ 3,360,000 9 Overhead 10 Assembly building 11 Assembling @ $ 30 per MH) $ 180,000 $ 900.000 12 Setting up machines (@ $ 900 per setup hour) 36,000 360,000 13 Handling material (@$ 3,000 per run) 24.000 120,000 14 Packaging building 15 Inspecting and packing (@ $5 per direct labor-hour) 300,000 114.000 16 Shipping (@$ 1.320 per shipment) 132.000 264.000 17 Total ABC overhead S672.000 $ 1.758,000 18 Total ABC cost $ 3,912.000 $ 5.118.000 19 Number of units 100,000 40.000 21 39.12 $ 127.95 20 Unit cost