Answered step by step

Verified Expert Solution

Question

1 Approved Answer

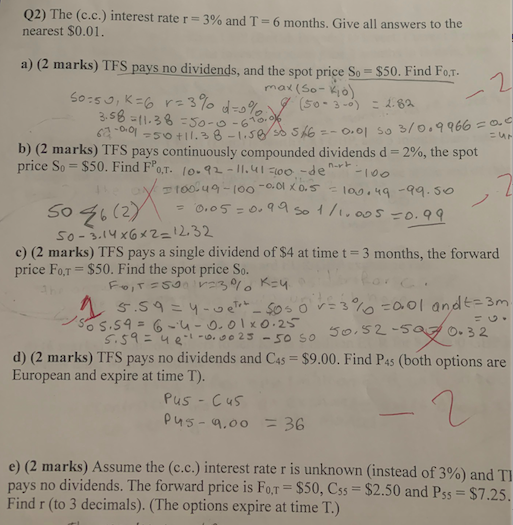

can you help me how to do that 02) The (c.c.) interest rate r = 3% and T = 6 months. Give all answers to

can you help me how to do that

can you help me how to do that

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Strategy Mapping For Learning Organizations Building Agility Into Your Balanced Scorecard

Authors: Phil Jones

1st Edition

0566088118,1409459292