Answered step by step

Verified Expert Solution

Question

1 Approved Answer

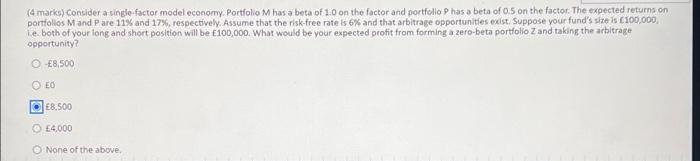

Can you please also provide calculations of your working. thann you in advance! (4 marks) Consider a single-factor model economy. Portfolio M has a beta

Can you please also provide calculations of your working. thann you in advance!

(4 marks) Consider a single-factor model economy. Portfolio M has a beta of 1.0 on the factor and portfolio P has a beta of 0.5 on the factor. The expected returns on portfolios M and Pare 11% and 17%, respectively. Assume that the risk-free rate is 6% and that arbitrage opportunities exist. Suppose your fund's size is 100,000, i.e. both of your long and short position will be 100,000. What would be your expected profit from forming a zero-beta portfolio Z and taking the arbitrage opportunity? O-8,500 O EO 8,500 4,000 O None of the above Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Statements

Authors: Inc. BarCharts

1st Edition

1423223837, 978-1423223832