Question

Can you please help with this problem I need it for Today , thank you very much , it is from the book investments 10th

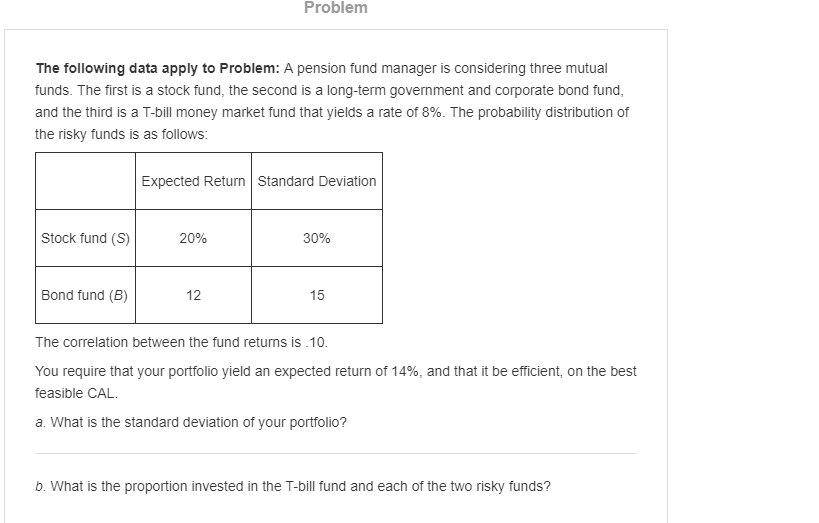

Can you please help with this problem I need it for Today , thank you very much , it is from the book investments 10th edition , may be you need more information to resolve it because it is the 9th question so I kindly ask to check if you need further information , Thank you

Can you please help with this problem I need it for Today , thank you very much , it is from the book investments 10th edition , may be you need more information to resolve it because it is the 9th question so I kindly ask to check if you need further information , Thank you

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Finance

Authors: Keith Pilbeam

3rd Edition

1403948372, 978-1403948373