can you respond on the excel sheet please

please put the answer on the excel sheet

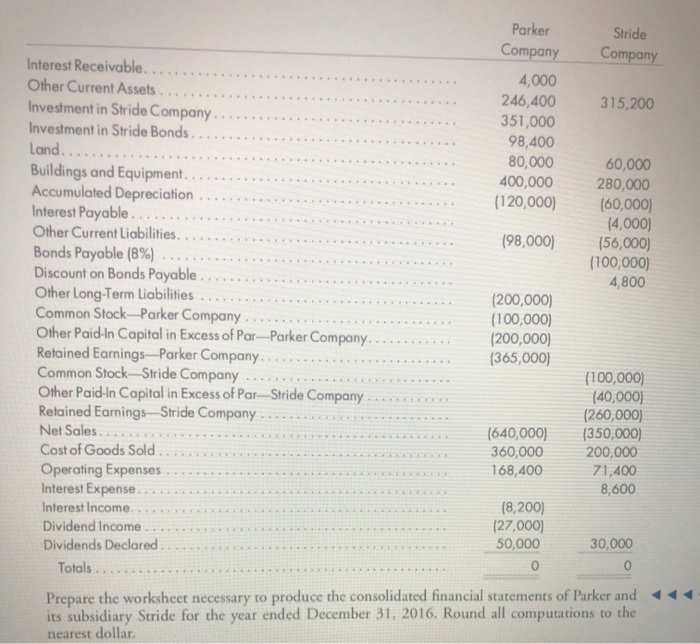

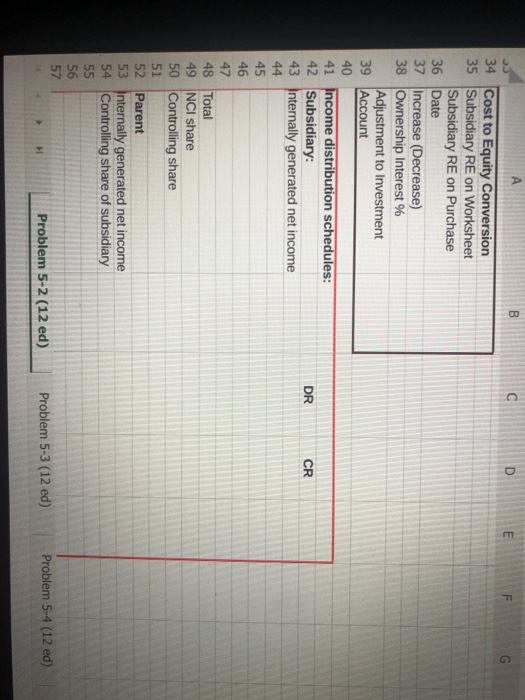

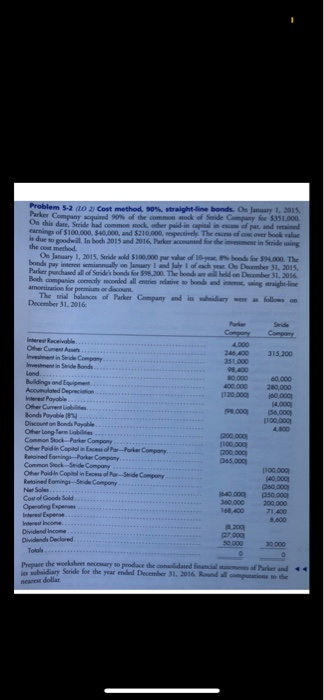

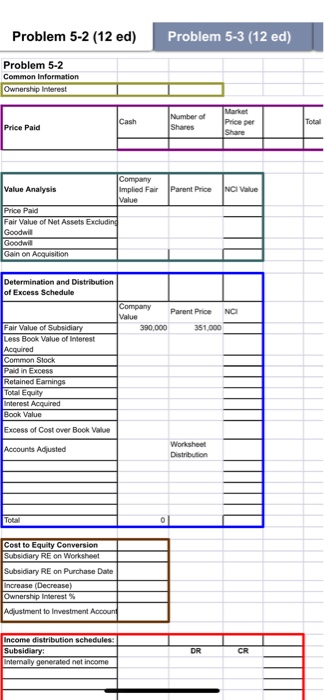

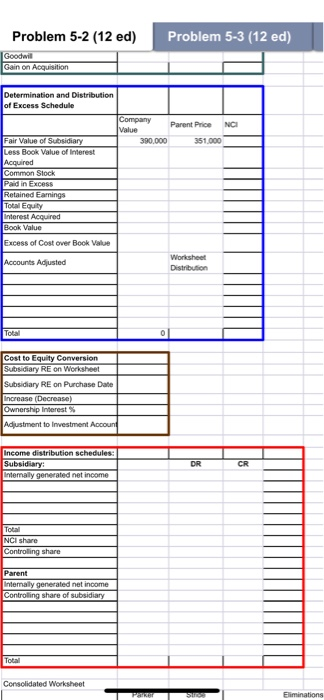

Note: No worksheet is required. Problem 5-2 (LO 2) Cost method, 90%, straight-line bonds. On January 1, 2015, Parker Company acquired 90% of the common stock of Stride Company for $351,000. On this date, Stride had common stock, other paid-in capital in excess of par, and retained earnings of $100,000, $40,000, and $210,000, respectively. The excess of cost over book value is due to goodwill. In both 2015 and 2016, Parker accounted for the investment in Stride using the cost method. On January 1, 2015, Stride sold $100,000 par value of 10-year, 8% bonds for $94,000. The bonds pay interest semiannually on January 1 and July 1 of each year. On December 31, 2015, Parker purchased all of Stride's bonds for $98,200. The bonds are still held on December 31, 2016. Both companies correctly recorded all entries relative to bonds and interest, using straight-line amortization for premium or discount. The trial balances of Parker Company and its subsidiary were December 31, 2016: as follows on Parker Stride Company Company Interest Receivable. Other Current Assets Investment in Stride Company 4,000 246,400 351,000 98,400 80,000 400,000 315,200 Investment in Stride Bonds. Land...... Buildings and Equipment. Accumulated Depreciation Interest Payable.... Other Current Liabilities Bonds Payable (8%) Discount on Bonds Payable. Other Long-Term Liabilities Common Stock-Parker Company Other Paid-In Capital in Excess of Par-Parker Company. Retained EarningsParker Company.. Common Stock-Stride Company Other Paid-In Capital in Excess of Par-Stride Company Retained Earnings Stride Company Net Sales. 60,000 280,000 (120,000) (60,000) (4,000) (56,000) (100,000) 4,800 (98,000) (200,000) (100,000) (200,000) (365,000) (100,000) (40,000) (260,000) (350,000) 200,000 (640,000) 360,000 168,400 Cost of Goods Sold Operating Expenses Interest Expense. . Interest Income. Dividend Income Dividends Declared 71,400 8,600 (8,200) (27,000) 50,000 30,000 Totals.. Prepare the worksheet necessary to produce the consolidated financial statements of Parker and its subsidiary Stride for the year ended December 31, 2016. Round all computations to the nearest dollar 06 fo E 13 Gain on Acquisition 14 Determination and Distribution of Excess 15 Schedule Company Value 16 17 Fair Value of Subsidiary Less Book Value of Interest 18 Acquired 19 Common Stock 20 Paid in Excess 21 Retained Earnings 22 Total Equity 23 Interest Acquired 24 Book Value Excess of Cost over Book 25 Value Parent Price NCI 390,000 351,000 Worksheet Distribution 26 Accounts Adjusted 32 Total Problem 5-2 (12 ed) Problem 5-4 (12 ed) Problem 5-3 (12 ed) 60 m A B D E 34 Cost to Equity Conversion 35 Subsidiary RE on Worksheet Subsidiary RE on Purchase 36 Date 37 Increase (Decrease) 38 Ownership Interest % Adjustment to Investment 39 Account 40 41 Income distribution schedules: 42 Subsidiary: 43 Internally generated net income DR CR 44 45 46 47 48 Total 49 NCI share 50 Controlling share 51 52 Parent 53 Internally generated net income 54 Controlling share of subsidiary 55 56 57 Problem 5-2 (12 ed) Problem 5-3 (12 ed) Problem 5-4 (12 ed) Problem 5-2 (10 n Cost method, 90%, straight-line bonds. On January 1, 2015 Parker Company acquired 90% of the common mock of Seride Company for s351.000 On this date, Sride had common mock, oder paid-in apial in eos of par, and retained earnings of $100,000, $40,000, and $210.000, respectivels The ecs of co over book value is due to the cost merk In both 2015 and 2016 Parker accountnd for the i ment in Seride using On January 1, 2015, Sride sold S100,000 par valae of 10-yea %bonde for 94000 The bonds pay interest semiannually on January 1 and July 1 of each year On Dember 31, 2015 Parker rpurchased all of Suide's bonds for $98,200. The bonds are ill held on Deoember 31, 2016 Bodh companies commctly reconded all entries relative so bonds and in, ing seraighe-line amoetization for premium or discount The rial halances of Parker Company and its sbidiary wee as follows on December 31, 2016 Parker Compony Sride Compony Interet Raceivoble Oher Cument Assets lnvement in Sride Compony Invesment in Side Bonds lond. . Buildings ond Equipment Accumulated Depreciotion Interest Payoble Oher Curent Liobilities Bonds Payoble (8n Discount on Bonds Payoble Oher Long-Term Liobiltes Common Stock-Parker Compony Oher Paidin Capital in Excess ofl Par-Parker Company Retained Earnings-Parker Compony Common Stock-Seide Compony Oher Paidin Copal in Encess ofl Par-Seide Compony Retained Eamings-Side Company Net Sales 4,000 246400 315,200 351.000 98,400 80.000 60,000 280,000 60,000 (4.000 (56.000 p00,000 4.800 400,000 020,000 000 (200,000 poo,000 go0.000 pas 000 (100,000) (40,000 260.000 ps0,000 40000 Cost of Goods Sold Openating Expen Interes Expense. Interest Income. Dividend Income Dividends Declared 360,000 200,000 168,400 71400 8,600 200 g7 000 50,000 30000 Totals Prenare the worksheet necessary to prodace dhe consolidated financial saens of Parker and in sbidiary Seride for the year ended December 31, 2016 Round all cmputations to the neanes dollar Problem 5-3 (12 ed) Problem 5-2 (12 ed) Problem 5-2 Common Information Ownership Interest Market Price per Share Number of Shares Cash Total Price Paid Company Implied Fair Value Value Analysis Parent Price NCI Value Price Paid Fair Value of Net Assets Excluding Goodwill Goodwil Gain on Acquisition Determination and Distribution of Excess Schedule Company Value Parent Price NCI Fair Value of Subsidiary Less Book Value of Interest Acquired Common Stock 351,000 390,000 Paid in Excess Retained Eamings Total Equity Interest Acquired Book Value Excess of Cost over Book Value Worksheet Accounts Adjusted Distribution Total Cost to Equity Conversion Subsidiary RE on Worksheet Subsidiary RE on Purchase Date Increase (Decrease) Ownership Interest % Adjustment to Investment Account Income distribution schedules Subsidiary: Intemaly generated net income DR CR Problem 5-2 (12 ed) Problem 5-3 (12 ed) Goodwill Gain on Acquisition Determination and Distribution of Excess Schedule Company Value Parent Price NCI Fair Value of Subsidiary Less Book Value of Interest Acquired Common Stock Paid in Excess Retained Eamings Total Equity Interest Acquired 390,000 351,000 Book Value Excess of Cost over Book Value Worksheet Accounts Adjusted Distribution Total 0 Cost to Equity Conversion Subsidiary RE on Worksheet Subsidiary RE on Purchase Date Increase (Decrease) Ownership Interest % Adjustment to Investment Account Income distribution schedules: Subsidiary: Intemaly generated net income DR CR Total NCI share Controling share Parent Internally generated net income Controling share of subsidiary Total Consolidated Worksheet Panker Eliminations Stroen Note: No worksheet is required. Problem 5-2 (LO 2) Cost method, 90%, straight-line bonds. On January 1, 2015, Parker Company acquired 90% of the common stock of Stride Company for $351,000. On this date, Stride had common stock, other paid-in capital in excess of par, and retained earnings of $100,000, $40,000, and $210,000, respectively. The excess of cost over book value is due to goodwill. In both 2015 and 2016, Parker accounted for the investment in Stride using the cost method. On January 1, 2015, Stride sold $100,000 par value of 10-year, 8% bonds for $94,000. The bonds pay interest semiannually on January 1 and July 1 of each year. On December 31, 2015, Parker purchased all of Stride's bonds for $98,200. The bonds are still held on December 31, 2016. Both companies correctly recorded all entries relative to bonds and interest, using straight-line amortization for premium or discount. The trial balances of Parker Company and its subsidiary were December 31, 2016: as follows on Parker Stride Company Company Interest Receivable. Other Current Assets Investment in Stride Company 4,000 246,400 351,000 98,400 80,000 400,000 315,200 Investment in Stride Bonds. Land...... Buildings and Equipment. Accumulated Depreciation Interest Payable.... Other Current Liabilities Bonds Payable (8%) Discount on Bonds Payable. Other Long-Term Liabilities Common Stock-Parker Company Other Paid-In Capital in Excess of Par-Parker Company. Retained EarningsParker Company.. Common Stock-Stride Company Other Paid-In Capital in Excess of Par-Stride Company Retained Earnings Stride Company Net Sales. 60,000 280,000 (120,000) (60,000) (4,000) (56,000) (100,000) 4,800 (98,000) (200,000) (100,000) (200,000) (365,000) (100,000) (40,000) (260,000) (350,000) 200,000 (640,000) 360,000 168,400 Cost of Goods Sold Operating Expenses Interest Expense. . Interest Income. Dividend Income Dividends Declared 71,400 8,600 (8,200) (27,000) 50,000 30,000 Totals.. Prepare the worksheet necessary to produce the consolidated financial statements of Parker and its subsidiary Stride for the year ended December 31, 2016. Round all computations to the nearest dollar 06 fo E 13 Gain on Acquisition 14 Determination and Distribution of Excess 15 Schedule Company Value 16 17 Fair Value of Subsidiary Less Book Value of Interest 18 Acquired 19 Common Stock 20 Paid in Excess 21 Retained Earnings 22 Total Equity 23 Interest Acquired 24 Book Value Excess of Cost over Book 25 Value Parent Price NCI 390,000 351,000 Worksheet Distribution 26 Accounts Adjusted 32 Total Problem 5-2 (12 ed) Problem 5-4 (12 ed) Problem 5-3 (12 ed) 60 m A B D E 34 Cost to Equity Conversion 35 Subsidiary RE on Worksheet Subsidiary RE on Purchase 36 Date 37 Increase (Decrease) 38 Ownership Interest % Adjustment to Investment 39 Account 40 41 Income distribution schedules: 42 Subsidiary: 43 Internally generated net income DR CR 44 45 46 47 48 Total 49 NCI share 50 Controlling share 51 52 Parent 53 Internally generated net income 54 Controlling share of subsidiary 55 56 57 Problem 5-2 (12 ed) Problem 5-3 (12 ed) Problem 5-4 (12 ed) Problem 5-2 (10 n Cost method, 90%, straight-line bonds. On January 1, 2015 Parker Company acquired 90% of the common mock of Seride Company for s351.000 On this date, Sride had common mock, oder paid-in apial in eos of par, and retained earnings of $100,000, $40,000, and $210.000, respectivels The ecs of co over book value is due to the cost merk In both 2015 and 2016 Parker accountnd for the i ment in Seride using On January 1, 2015, Sride sold S100,000 par valae of 10-yea %bonde for 94000 The bonds pay interest semiannually on January 1 and July 1 of each year On Dember 31, 2015 Parker rpurchased all of Suide's bonds for $98,200. The bonds are ill held on Deoember 31, 2016 Bodh companies commctly reconded all entries relative so bonds and in, ing seraighe-line amoetization for premium or discount The rial halances of Parker Company and its sbidiary wee as follows on December 31, 2016 Parker Compony Sride Compony Interet Raceivoble Oher Cument Assets lnvement in Sride Compony Invesment in Side Bonds lond. . Buildings ond Equipment Accumulated Depreciotion Interest Payoble Oher Curent Liobilities Bonds Payoble (8n Discount on Bonds Payoble Oher Long-Term Liobiltes Common Stock-Parker Compony Oher Paidin Capital in Excess ofl Par-Parker Company Retained Earnings-Parker Compony Common Stock-Seide Compony Oher Paidin Copal in Encess ofl Par-Seide Compony Retained Eamings-Side Company Net Sales 4,000 246400 315,200 351.000 98,400 80.000 60,000 280,000 60,000 (4.000 (56.000 p00,000 4.800 400,000 020,000 000 (200,000 poo,000 go0.000 pas 000 (100,000) (40,000 260.000 ps0,000 40000 Cost of Goods Sold Openating Expen Interes Expense. Interest Income. Dividend Income Dividends Declared 360,000 200,000 168,400 71400 8,600 200 g7 000 50,000 30000 Totals Prenare the worksheet necessary to prodace dhe consolidated financial saens of Parker and in sbidiary Seride for the year ended December 31, 2016 Round all cmputations to the neanes dollar Problem 5-3 (12 ed) Problem 5-2 (12 ed) Problem 5-2 Common Information Ownership Interest Market Price per Share Number of Shares Cash Total Price Paid Company Implied Fair Value Value Analysis Parent Price NCI Value Price Paid Fair Value of Net Assets Excluding Goodwill Goodwil Gain on Acquisition Determination and Distribution of Excess Schedule Company Value Parent Price NCI Fair Value of Subsidiary Less Book Value of Interest Acquired Common Stock 351,000 390,000 Paid in Excess Retained Eamings Total Equity Interest Acquired Book Value Excess of Cost over Book Value Worksheet Accounts Adjusted Distribution Total Cost to Equity Conversion Subsidiary RE on Worksheet Subsidiary RE on Purchase Date Increase (Decrease) Ownership Interest % Adjustment to Investment Account Income distribution schedules Subsidiary: Intemaly generated net income DR CR Problem 5-2 (12 ed) Problem 5-3 (12 ed) Goodwill Gain on Acquisition Determination and Distribution of Excess Schedule Company Value Parent Price NCI Fair Value of Subsidiary Less Book Value of Interest Acquired Common Stock Paid in Excess Retained Eamings Total Equity Interest Acquired 390,000 351,000 Book Value Excess of Cost over Book Value Worksheet Accounts Adjusted Distribution Total 0 Cost to Equity Conversion Subsidiary RE on Worksheet Subsidiary RE on Purchase Date Increase (Decrease) Ownership Interest % Adjustment to Investment Account Income distribution schedules: Subsidiary: Intemaly generated net income DR CR Total NCI share Controling share Parent Internally generated net income Controling share of subsidiary Total Consolidated Worksheet Panker Eliminations Stroen