Answered step by step

Verified Expert Solution

Question

1 Approved Answer

can you show me how to do both if sub-parts if possible, if not the B3b please. thank you B3. [15 marks total] In December

can you show me how to do both if sub-parts if possible, if not the B3b please.

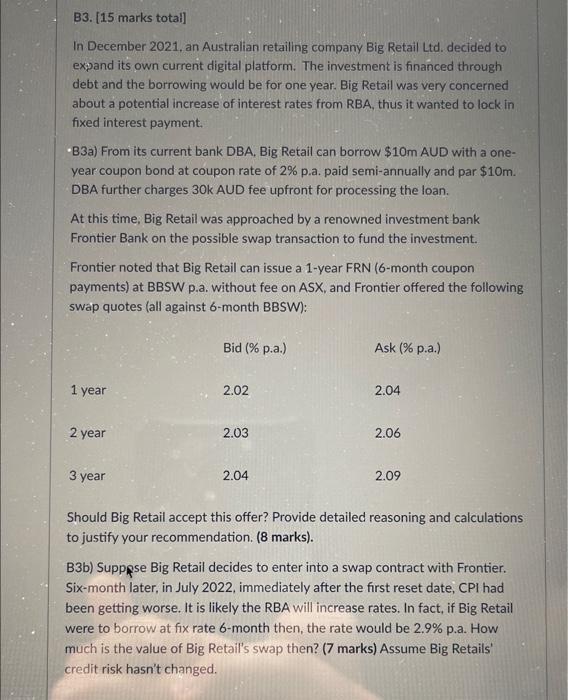

B3. [15 marks total] In December 2021, an Australian retailing company Big Retail Ltd. decided to expand its own current digital platform. The investment is financed through debt and the borrowing would be for one year. Big Retail was very concerned about a potential increase of interest rates from RBA, thus it wanted to lock in fixed interest payment. -B3a) From its current bank DBA, Big Retail can borrow $10m AUD with a oneyear coupon bond at coupon rate of 2% p.a. paid semi-annually and par $10m. DBA further charges 30k AUD fee upfront for processing the loan. At this time, Big Retail was approached by a renowned investment bank Frontier Bank on the possible swap transaction to fund the investment. Frontier noted that Big Retail can issue a 1-year FRN (6-month coupon payments) at BBSW p.a. without fee on ASX, and Frontier offered the following swap quotes (all against 6-month BBSW): Should Big Retail accept this offer? Provide detailed reasoning and calculations to justify your recommendation. ( 8 marks). B3b) Supppse Big Retail decides to enter into a swap contract with Frontier. Six-month later, in July 2022, immediately after the first reset date, CPI had been getting worse. It is likely the RBA will increase rates. In fact, if Big Retail were to borrow at fix rate 6 -month then, the rate would be 2.9% p.a. How much is the value of Big Retail's swap then? (7 marks) Assume Big Retails' credit risk hasn't changed. B3. [15 marks total] In December 2021, an Australian retailing company Big Retail Ltd. decided to expand its own current digital platform. The investment is financed through debt and the borrowing would be for one year. Big Retail was very concerned about a potential increase of interest rates from RBA, thus it wanted to lock in fixed interest payment. -B3a) From its current bank DBA, Big Retail can borrow $10m AUD with a oneyear coupon bond at coupon rate of 2% p.a. paid semi-annually and par $10m. DBA further charges 30k AUD fee upfront for processing the loan. At this time, Big Retail was approached by a renowned investment bank Frontier Bank on the possible swap transaction to fund the investment. Frontier noted that Big Retail can issue a 1-year FRN (6-month coupon payments) at BBSW p.a. without fee on ASX, and Frontier offered the following swap quotes (all against 6-month BBSW): Should Big Retail accept this offer? Provide detailed reasoning and calculations to justify your recommendation. ( 8 marks). B3b) Supppse Big Retail decides to enter into a swap contract with Frontier. Six-month later, in July 2022, immediately after the first reset date, CPI had been getting worse. It is likely the RBA will increase rates. In fact, if Big Retail were to borrow at fix rate 6 -month then, the rate would be 2.9% p.a. How much is the value of Big Retail's swap then? (7 marks) Assume Big Retails' credit risk hasn't changed thank you

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sustainable Finance And Banking

Authors: Marcel Jeucken

1st Edition

1853837660, 978-1853837661