Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Can you tell Why its B? Consider the following: market price is 1.63A$$, how could you arbitrage? (Hint: express the exchange rates in terms of

Can you tell Why its B?

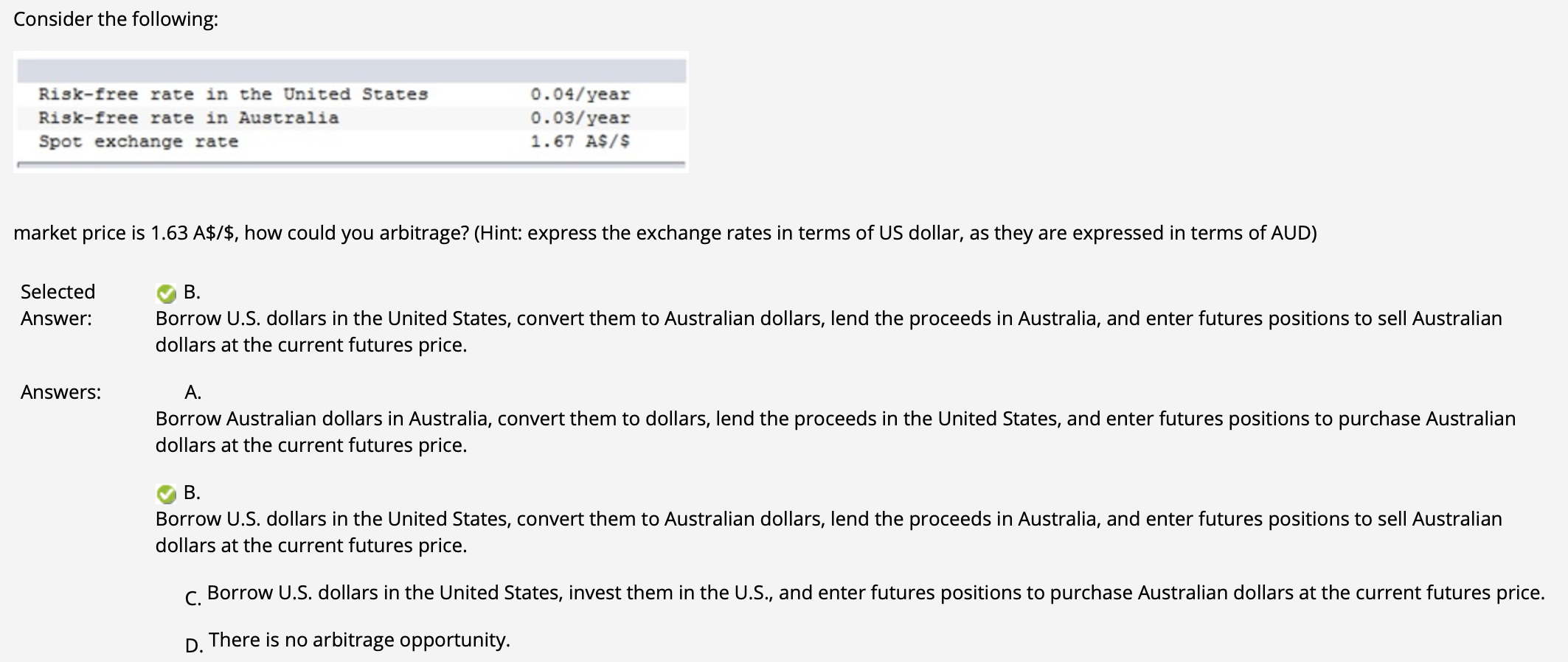

Consider the following: market price is 1.63A$$, how could you arbitrage? (Hint: express the exchange rates in terms of US dollar, as they are expressed in terms of AUD) Selected Answer: Answers: B. Borrow U.S. dollars in the United States, convert them to Australian dollars, lend the proceeds in Australia, and enter futures positions to sell Australian dollars at the current futures price. A. Borrow Australian dollars in Australia, convert them to dollars, lend the proceeds in the United States, and enter futures positions to purchase Australian dollars at the current futures price. B. Borrow U.S. dollars in the United States, convert them to Australian dollars, lend the proceeds in Australia, and enter futures positions to sell Australian dollars at the current futures price. C. Borrow U.S. dollars in the United States, invest them in the U.S., and enter futures positions to purchase Australian dollars at the current futures price. D. There is no arbitrage opportunityStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance A Quantitative Introduction Volume 2

Authors: Piotr Staszkiewicz, Lucia Staszkiewicz

1st Edition

0128027975, 978-0128027974