Answered step by step

Verified Expert Solution

Question

1 Approved Answer

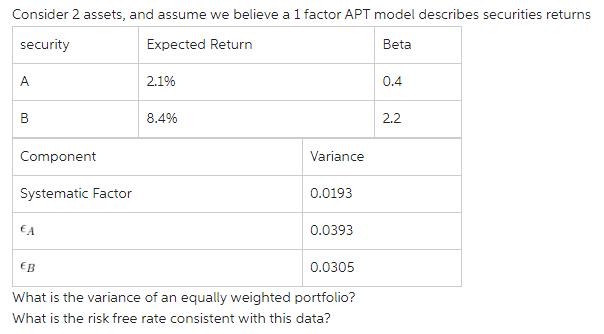

Consider 2 assets, and assume we believe a 1 factor APT model describes securities returns security Expected Return Betal A B Component Systematic Factor

Consider 2 assets, and assume we believe a 1 factor APT model describes securities returns security Expected Return Betal A B Component Systematic Factor EA EB 2.1% 8.4% Variance 0.0193 0.0393 0.0305 What is the variance of an equally weighted portfolio? What is the risk free rate consistent with this data? 0.4 2.2

Step by Step Solution

★★★★★

3.54 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Concepts In Federal Taxation

Authors: Kevin E. Murphy, Mark Higgins, Tonya K. Flesher

19th Edition

978-0324379556, 324379552, 978-1111579876