Capital Investment, Discount Rates, Intangible and Indirect Benefits, Time Horizon, Contemporary Manufacturing Environment

Mallette Manufacturing, Inc., produces washing machines, dryers, and dishwashers. Because of increasing competition, Mallette is considering investing in an automated manufacturing system. Since competition is most keen for dishwashers, the production process for this line has been selected for initial evaluation. The automated system for the dishwasher line would replace an existing system (purchased one year ago for $6 million). Although the existing system will be fully depreciated in nine years, it is expected to last another 10 years. The automated system would also have a useful life of 10 years.

The existing system is capable of producing 100,000 dishwashers per year. Sales and production data using the existing system are provided by the Accounting Department:

| Sales per year (units) | 100,000 |

| Selling price | $300 |

| Costs per unit: |

| Direct materials | 80 |

| Direct labor | 90 |

| Volume-related overhead | 20 |

| Direct fixed overhead | 40* |

*All cash expenses with the exception of depreciation, which is $6 per unit. The existing equipment is being depreciated using straight-line with no salvage value considered.

The automated system will cost $34 million to purchase, plus an estimated $20 million in software and implementation. (Assume that all investment outlays occur at the beginning of the first year.) If the automated equipment is purchased, the old equipment can be sold for $3 million.

The automated system will require fewer parts for production and will produce with less waste. Because of this, the direct material cost per unit will be reduced by 25 percent. Automation will also require fewer support activities, and as a consequence, volume-related overhead will be reduced by $4 per unit and direct fixed overhead (other than depreciation) by $17 per unit. Direct labor is reduced by 60 percent. Assume, for simplicity, that the new investment will be depreciated on a pure straight-line basis for tax purposes with no salvage value. Ignore the half-life convention.

The firms cost of capital is 12 percent, but management chooses to use 20 percent as the required rate of return for evaluation of investments. The combined federal and state tax rate is 40 percent.

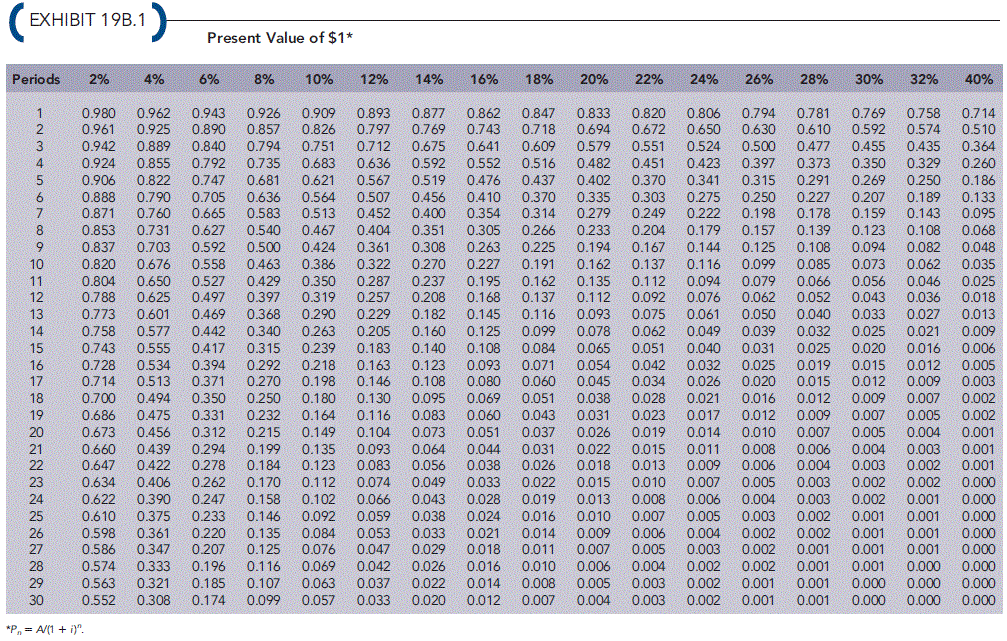

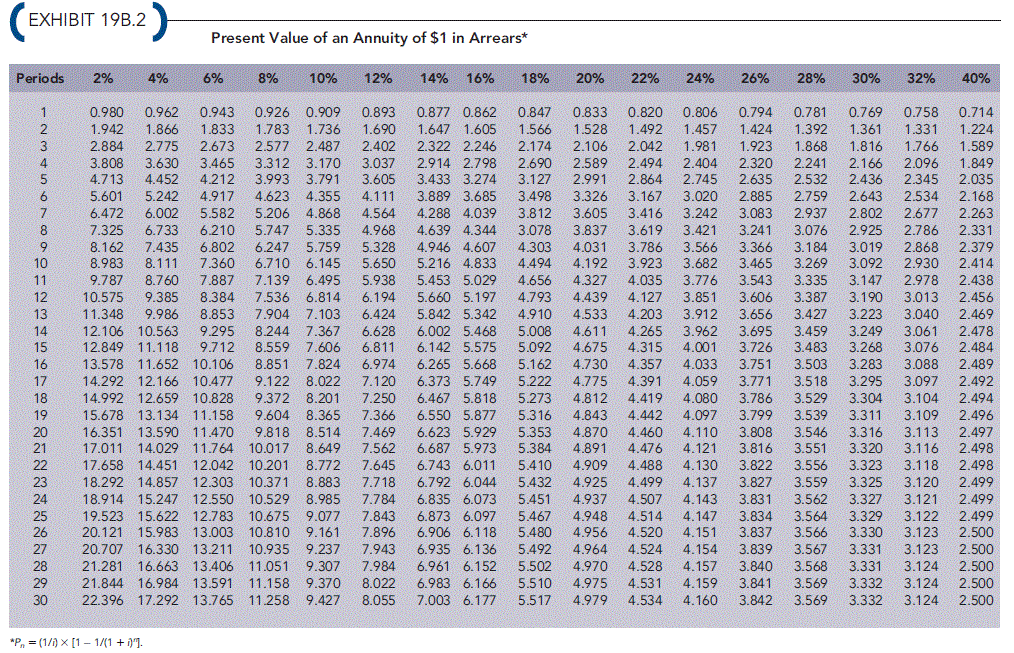

The present value tables provided in Exhibit 19B.1 and Exhibit 19B.2 must be used to solve the following problems.

Required:

1. Compute the net present value for the old system and the automated system.

| Old system | $ |

| New system | $ |

Which system would the company choose? Old system

2. Repeat the net present value analysis of Requirement 1, using 12 percent as the discount rate.

| Old system | $ |

| New system | $ |

3. Upon seeing the projected sales for the old system, the marketing manager commented: Sales of 100,000 units per year cannot be maintained in the current competitive environment for more than one year unless we buy the automated system. The automated system will allow us to compete on the basis of quality and lead time. If we keep the old system, our sales will drop by 10,000 units per year. Repeat the net present value analysis, using this new information and a 12 percent discount rate.

4. An industrial engineer for Mallette noticed that salvage value for the automated equipment had not been included in the analysis. He estimated that the equipment could be sold for $4 million at the end of 10 years. He also estimated that the equipment of the old system would have no salvage value at the end of 10 years. Repeat the net present value analysis using this information, the information in Requirement 3, and a 12 percent discount rate.

| New system | Increases | to | NPV = $ |

| Old system | Unchanged | to | NPV = $ |

EXHIBIT 19B.1 Present Value of $1* Periods 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24% 26% 28% 30% 32% 40% 0.980 0.962 0.9430.926 0.909 0.893 0.877 0.862 0.847 0.833 0.820 0.806 0.794 0.781 0.769 0.758 0.714 0.961 0.9250.890 0.8570.826 0.797 0.769 0.743 0.718 0.694 0.672 0.650 0.630 0.610 0.592 0.574 0.510 0.942 0.8890.8400.794 0.751 0.712 0.675 0.641 0.609 0.579 0.551 0.524 0.500 0.477 0.455 0435 0.364 0.924 0.8550.792 0.7350.683 0.636 0.592 0.552 0.516 0.482 0.451 0.423 0.397 0.373 0.350 0.3290.260 5 0.906 0.822 0.747 0.681 0.621 0.567 0.519 0.476 0.437 0.402 0.370 0.341 0.315 0.291 0.269 0.250 0.186 0888 0.790 0.705 0.636 0.564 0.507 0.456 0.410 0.370 0.335 0.303 0.275 0.250 0.227 0.207 0.189 0.133 0.871 0.760 0.665 0.583 0.513 0.452 0.400 0.354 0.314 0.279 0.249 0.222 0.198 0.178 0.159 0.1430.095 8 0.853 0.731 0.627 0.540 0.467 0.404 0.351 0.305 0.266 0.233 0.204 0.179 0.157 0.139 0.1230.108 0.068 9 0.837 0.703 0.592 0.500 0.424 0.361 0.308 0.263 0.225 0.194 0.167 0.144 0.125 0.108 0.094 0.082 0.048 0.820 0.676 0.558 0.463 0.386 0.322 0.270 0.2270.191 0.162 0.137 0.116 0.099 0.085 0.073 0.062 0.035 0.804 0.650 0.527 0.429 0.350 0.287 0.237 0.195 0.162 0.135 0.112 0.094 0.079 0.066 0.056 0.046 0.025 0.788 0.6250.497 0.3970.319 0.257 0.208 0.168 0.137 0.112 0.092 0.076 0.062 0.052 0.043 0.0360.018 3 10 12 13 0.773 0.601 0.469 0.368 0290 0229 0.182 0.145 OLI 16 0093 0075 0091 0050 0040 0083 D027 14 0.758 0.577 0.442 0.340 0.263 0.205 0.160 0.125 0.099 0.078 0.062 0.049 0.039 0.032 0.025 0.021 0.009 15 0.743 0.555 0.417 0.315 0.239 0.183 0.140 0.108 0.084 0.0650.0510.040 0.031 0.025 0.020 0.016 0.006 0.728 0.534 0.3940.292 0.218 0.163 0.123 0.093 0.071 0.054 0.042 0.032 0.025 0.019 0.015 0.0120.005 17 0.714 0.513 0.371 0.270 0.198 0.146 0.108 0.080 0.060 0.045 0.034 0.026 0.020 0.015 0.012 0.009 0.003 0.700 0.494 0.350 0.250 0.180 0.130 0.095 0.069 0.051 0.038 0.028 0.021 0.016 0.012 0.009 0.0070.002 0.686 0.4750.3310.232 0.164 0.116 0.083 0.060 0.043 0.031 0.023 0.017 0.012 0.009 0.007 0.005 0.002 0.673 0.4560.312 0.2150.149 0.104 0.073 0.051 0.037 0.026 0.019 0.014 0.010 0.007 0.005 0.004 0.001 0.660 0.439 0.294 0.199 0.135 0.093 0.0640.044 0.0310.022 0.015 0.011 0.008 0.006 0.004 0.003 0.001 0.647 0.422 0.278 0.184 0.123 0.083 0.056 0.038 0.026 0.018 0.013 0.009 0.006 0.004 0.003 0.002 0.001 0.634 0.406 0.262 0.170 0.112 0.074 0.049 0.033 0.022 0.015 0.010 0.007 0.005 0.003 0.002 0.0020.000 24 0.622 0.390 0.247 0.158 0.102 0.066 0.043 0.028 0.019 0.013 0.008 0.006 0.004 0.003 0.002 0.001 0.000 0.610 0.375 0.233 0.146 0.092 0.059 0.038 0.024 0.016 0.010 0.007 0.005 0.003 0.002 0.001 0.0010.000 0.598 0.361 0.220 0.135 0.084 0.053 0.0330.021 0.014 0.009 0.006 0.004 0.002 0.002 0.001 0.001 0.000 0.586 0.3470.2070.1250.076 0.047 0.029 0.018 0.011 0.007 0.005 0.003 0.002 0.001 0.001 0.001 0.000 0.574 0.333 0.1960.116 0.069 0.042 0.026 0.016 0.010 0.006 0.004 0.002 0.002 0.001 0.001 0.000 0.000 0.563 0.3210.185 0.1070.063 0.037 0.022 0.014 0.008 0.005 0.003 0.002 0.001 0.001 0.000 0.0000.000 0.552 0.308 0.1740.0990.057 0.033 0.020 0.012 0.007 0.004 0.003 0.002 0.001 0.001 0.0000.0000.000 18 20 23 25 26 27 28 29 30 EXHIBIT 19B.2 Present Value of an Annuity of $1 in Arrears Periods 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24% 26% 28% 30% 32% 40% 0.980 0.962 0.943 0.926 0.909 0.893 0.877 0.862 0.847 0.833 0.820 0.806 0.794 0.781 0.769 0.758 0.714 1.942 1.866 1833 1.783 1.736 1.690 1.647 1.605 1.566 1.528 1.492 1.457 1.424 1.392 1.361 1331 1.224 2.884 2.7752.6732.577 2.487 2.402 2.322 2.246 2.174 2.106 2.042 1.981 1.923 1.868 1.816 1.766 1.589 3.808 3.630 3.465 3.312 3.170 3.037 2.914 2.798 2.690 2.589 2.494 2.404 2.320 2.241 2.166 2.096 1.849 4.713 4.452 4.212 3.9933.7913.605 3.433 3.274 3.127 2.991 2.864 2.745 2.635 2.532 2.436 2.345 2.035 5.601 5.24249174.623 4.355 4.111 3.889 3.685 3.498 3.326 3.167 3.020 2.885 2.759 2.643 2.534 2.168 6.472 6.002 5.582 5.206 4.868 4.564 4.288 4.039 3.812 3.605 3.416 3.242 3.083 2.937 2.802 2.677 2.263 7.325 6.733 6210 5.747 5.335 4968 4.639 4.344 3078 3.837 3.619 3.421 3.241 3.076 2.925 2.786 2.331 8.162 7.4356.8026.2475.759 5.328 4.946 4.607 4.303 4.031 3.786 3.566 3.366 3.184 3.019 2.868 2.379 8.983 8.111 7.360 6.710 6.145 5.650 5.216 4833 4.494 4.192 3.923 3.682 3.465 3.269 3.092 2.930 2.414 9.787 8.760 7.887 7.139 6.495 5.938 5.453 5.029 4.656 4.327 4.035 3.776 3.543 3.335 3.147 2.978 2.438 4.127 3.851 3.606 3.387 3.190 3.013 2.456 11.348 9.986 8.853 7.904 7.1036.424 5.842 5.342 4.910 4.5334.203 3.912 3.6563.427 3.223 3.0402.469 14 12.106 10.5639.295 8.244 7.367 6.628 6.002 5.468 5.008 4.611 4.265 3.962 3.695 3.459 3.249 3.061 2.478 15 12.849 11.1189.712 8.559 7.606 6.811 6.142 5.575 5.092 4.675 4.315 4.001 3.726 3.483 3.268 3.076 2.484 16 13.578 11.652 10.106 8.851 7.824 6.974 6.265 5.668 5.162 4.730 4.357 4.033 3.751 3.503 3.283 3.088 2.489 17 14.292 12.166 10.4779.122 8.022 7.120 6.373 5.749 5.222 4.775 4.391 4.059 3.771 3.518 3.295 3.097 2.492 18 14.992 12.659 10.8289.372 8.201 7.250 6.467 5.818 5.273 4.812 4.419 4.080 3.786 3.529 3.304 3.104 2.494 19 15.678 13.134 11.1589.604 8.365 7.366 6.550 5.877 5.316 4.843 4.442 4.097 3.799 3.539 3.311 3.109 2.496 20 16.351 13.590 11470 9.818 8.514 7.469 6.623 5.929 5.353 4.870 4.460 4.110 3.808 3.546 3.316 3.113 2.497 21 17.011 14.029 11.764 10.017 8.649 7.562 6.687 5.973 5.384 4.891 4.476 4.121 3.816 3.551 3.320 3.116 2.498 22 17.658 14.451 12.042 10.201 8.772 7.645 6.743 6.011 5.410 4.909 4.488 4.130 3.822 3.556 3.323 3.118 2.498 18.292 14.857 12.303 10.371 8.883 7.718 6.792 6.0445.432 4.925 4.499 4.137 3.827 3.559 3.325 3.120 2.499 24 18.914 15.247 12.550 10.529 8.985 7.784 6.835 6.07354514.937 4.507 4.143 3.831 3.562 3.327 3.121 2.499 19.523 15.622 12.783 10.675 9.077 7.843 6.873 6.097 5.467 4.948 4.514 4.147 3.834 3.564 3.329 3.122 2.499 26 20.121 15.983 13.003 10.810 9.161 7.896 6.906 6.118 5.480 4.956 4.520 4.151 3.837 3.566 3.330 3.123 2.500 27 20.707 16.330 13.211 10.935 9.237 7.943 6.935 6.136 5.492 4.964 4.524 4.154 3.839 3.567 3.331 3.123 2.500 28 21.281 16.663 13.406 11.051 9.307 7.984 6.961 6.152 5.502 4.970 4.528 4.157 3.840 3.568 3.331 3.124 2.500 29 21.844 16.98413.591 11.158 9.370 8.022 6.983 6.166 5.510 4.975 4.531 4.159 3.841 3.569 3.332 3.124 2.500 30 22.396 17.29213.765 11.258 9.427 8.055 7.003 6.177 5.517 4979 4.534 4.160 3.842 3.569 3.332 3.124 2.500 2 4 10 12 10.575 9.385 8.384 7.536 6.814 6.194 5.660 5.197 4.793 4439 23 25