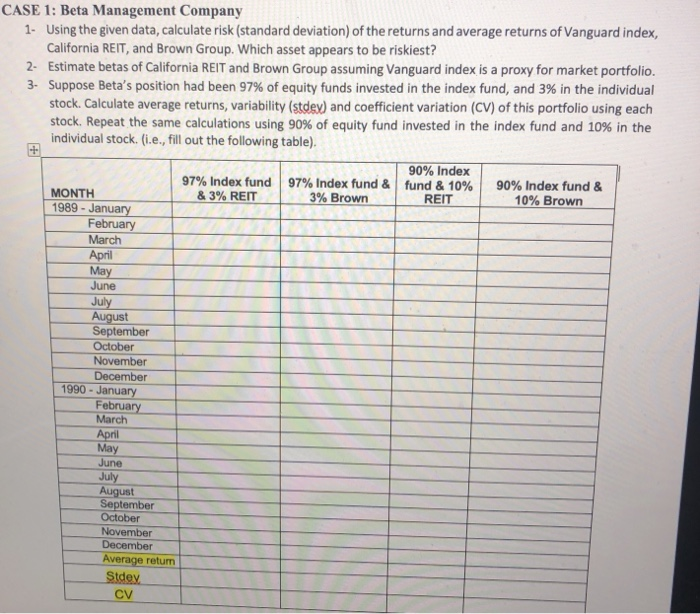

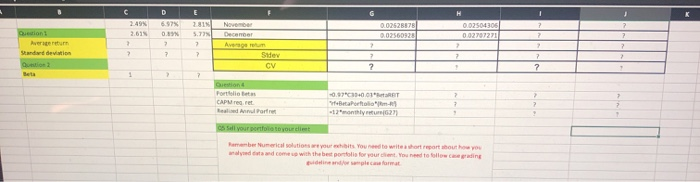

CASE 1: Beta Management Company 1. Using the given data, calculate risk (standard deviation) of the returns and average returns of Vanguard index, California REIT, and Brown Group. Which asset appears to be riskiest? 2- Estimate betas of California REIT and Brown Group assuming Vanguard index is a proxy for market portfolio. 3. Suppose Beta's position had been 97% of equity funds invested in the index fund, and 3% in the individual stock. Calculate average returns, variability (stdey) and coefficient variation (CV) of this portfolio using each stock. Repeat the same calculations using 90% of equity fund invested in the index fund and 10% in the individual stock. (i.e., fill out the following table). 90% Index 97% Index fund 97% Index fund & fund & 10% 90% Index fund & MONTH & 3% REIT 3% Brown REIT 10% Brown 1989 - January February March April May June July August September October November December 1990 - January February March April May June July August September October November December Average return Sider CV G H C 2.49% 697 0. E 281 5.73 Question 0.02528878 0.02560928 0.02504306 0.02707273 2 2 > 3 2 November Decor Average retum Sidev CV 2 Standard deviation Question 2 ? 2 2 7 2 1 7 Destion Portfolio -0.001BT CAP regret BetaPortal 12 (627 Sell your to your diet Pembe Numerical solutions you You need to write abortreport both you nayedad come with the best portfolio for your chant. You need to be grading CASE 1: Beta Management Company 1. Using the given data, calculate risk (standard deviation) of the returns and average returns of Vanguard index, California REIT, and Brown Group. Which asset appears to be riskiest? 2- Estimate betas of California REIT and Brown Group assuming Vanguard index is a proxy for market portfolio. 3. Suppose Beta's position had been 97% of equity funds invested in the index fund, and 3% in the individual stock. Calculate average returns, variability (stdey) and coefficient variation (CV) of this portfolio using each stock. Repeat the same calculations using 90% of equity fund invested in the index fund and 10% in the individual stock. (i.e., fill out the following table). 90% Index 97% Index fund 97% Index fund & fund & 10% 90% Index fund & MONTH & 3% REIT 3% Brown REIT 10% Brown 1989 - January February March April May June July August September October November December 1990 - January February March April May June July August September October November December Average return Sider CV G H C 2.49% 697 0. E 281 5.73 Question 0.02528878 0.02560928 0.02504306 0.02707273 2 2 > 3 2 November Decor Average retum Sidev CV 2 Standard deviation Question 2 ? 2 2 7 2 1 7 Destion Portfolio -0.001BT CAP regret BetaPortal 12 (627 Sell your to your diet Pembe Numerical solutions you You need to write abortreport both you nayedad come with the best portfolio for your chant. You need to be grading