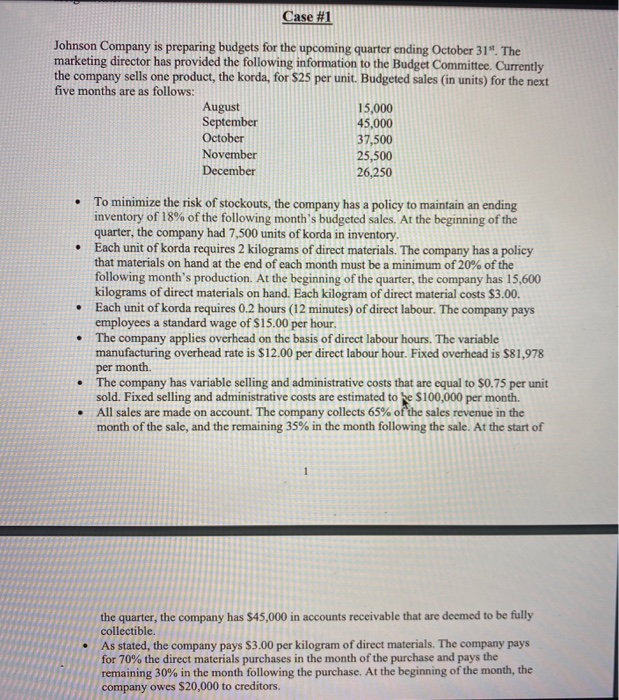

Case #1 . Johnson Company is preparing budgets for the upcoming quarter ending October 31". The marketing director has provided the following information to the Budget Committee. Currently the company sells one product, the korda, for $25 per unit. Budgeted sales in units) for the next five months are as follows: August 15,000 September 45,000 October 37,500 November 25,500 December 26,250 To minimize the risk of stockouts, the company has a policy to maintain an ending inventory of 18% of the following month's budgeted sales. At the beginning of the quarter, the company had 7,500 units of korda in inventory. Each unit of korda requires 2 kilograms of direct materials. The company has a policy that materials on hand at the end of each month must be a minimum of 20% of the following month's production. At the beginning of the quarter, the company has 15,600 kilograms of direct materials on hand. Each kilogram of direct material costs $3.00. Each unit of korda requires 0.2 hours (12 minutes) of direct labour. The company pays employees a standard wage of $15.00 per hour. The company applies overhead on the basis of direct labour hours. The variable manufacturing overhead rate is $12.00 per direct labour hour. Fixed overhead is $81,978 per month The company has variable selling and administrative costs that are equal to $0.75 per unit sold. Fixed selling and administrative costs are estimated to be $100,000 per month. All sales are made on account. The company collects 65% of the sales revenue in the month of the sale, and the remaining 35% in the month following the sale. At the start of 1 the quarter, the company has $45,000 in accounts receivable that are deemed to be fully collectible. As stated, the company pays $3.00 per kilogram of direct materials. The company pays for 70% the direct materials purchases in the month of the purchase and pays the remaining 30% in the month following the purchase. At the beginning of the month, the company owes $20,000 to creditors. (F) Prepare the ending finished goods inventory budget for the quarter-end. (G) Prepare a cost of goods sold budget for the quarter-end. (H) Prepare the selling and administrative expense budget for August, September, and October, and for the quarter-end. (1) Prepare a budgeted income statement for the quarter-end. (J) Prepare the schedule of expected cash collections on sales for August, September, and October, and for the quarter-end. Case #1 . Johnson Company is preparing budgets for the upcoming quarter ending October 31". The marketing director has provided the following information to the Budget Committee. Currently the company sells one product, the korda, for $25 per unit. Budgeted sales in units) for the next five months are as follows: August 15,000 September 45,000 October 37,500 November 25,500 December 26,250 To minimize the risk of stockouts, the company has a policy to maintain an ending inventory of 18% of the following month's budgeted sales. At the beginning of the quarter, the company had 7,500 units of korda in inventory. Each unit of korda requires 2 kilograms of direct materials. The company has a policy that materials on hand at the end of each month must be a minimum of 20% of the following month's production. At the beginning of the quarter, the company has 15,600 kilograms of direct materials on hand. Each kilogram of direct material costs $3.00. Each unit of korda requires 0.2 hours (12 minutes) of direct labour. The company pays employees a standard wage of $15.00 per hour. The company applies overhead on the basis of direct labour hours. The variable manufacturing overhead rate is $12.00 per direct labour hour. Fixed overhead is $81,978 per month The company has variable selling and administrative costs that are equal to $0.75 per unit sold. Fixed selling and administrative costs are estimated to be $100,000 per month. All sales are made on account. The company collects 65% of the sales revenue in the month of the sale, and the remaining 35% in the month following the sale. At the start of 1 the quarter, the company has $45,000 in accounts receivable that are deemed to be fully collectible. As stated, the company pays $3.00 per kilogram of direct materials. The company pays for 70% the direct materials purchases in the month of the purchase and pays the remaining 30% in the month following the purchase. At the beginning of the month, the company owes $20,000 to creditors. (F) Prepare the ending finished goods inventory budget for the quarter-end. (G) Prepare a cost of goods sold budget for the quarter-end. (H) Prepare the selling and administrative expense budget for August, September, and October, and for the quarter-end. (1) Prepare a budgeted income statement for the quarter-end. (J) Prepare the schedule of expected cash collections on sales for August, September, and October, and for the quarter-end