Question

Case 113: Dyna Golf Joe Bell, president and chief executive officer of Dyna Golf, has called a meeting of the executive committee of his board

Case 113: Dyna Golf

Joe Bell, president and chief executive officer of Dyna Golf, has called a meeting of the executive committee of his board of directors. He is concerned about the price competition and declining sales of his golf wedge line of business. Bell summarizes the current situation by saying,

As you know, we set target prices to maintain a gross margin on sales of 35 percent. On some products, such as our drivers, we have been able to achieve the target price. We have been able to achieve higher prices on our putters than a target 35 percent gross margin would dictate. But our wedges are a totally different story.

Our factory is among the most efficient in the world. I think that some foreign companies are dumping wedges in the U.S. market, driving down prices and unit sales. Weve been reluctant to further cut our prices for fear of what this will do to our gross margins. Fortunately, weve been able to offset the decline in sales of wedges by significantly raising the price of our putters. We were pleasantly surprised when our customers readily accepted the price increases of our putters, and we havent experienced much reaction from our competitors on the putter price increases.

Steve Barber, an outside director on the board, asks:

Joe, I dont pretend to know a lot about the golf club business, but how confident are you in your cost data? If your costs are off, wont your prices be off as well?

Joe Bell responds:

Thats a good point, Steve, and one Ive been worried about. Weve been modernizing our production facilities and Ive asked our controller, Phil Meyers, to look into it and report back after he has undertaken a thorough analysis. My purpose for calling this meeting was to update you on our current situation and let you know what we are doing.

Background

Dyna Golf has been in business for 15 years. Its one plant manufactures three different types of golf clubs: drivers, wedges, and putters. Dyna does not produce a complete club with a shaft and grip. It makes the metal head that is sold to other companies that assemble and market the complete club. Dyna holds four patents on a unique golf club head design that forges together into one club head three different metals: steel, titanium, and brass. It also has a very distinctive appearance. These three metals weigh different amounts, and by designing a club head with the three metals, Dyna produces a club with unique swing and feel properties. While the Dyna club is unique and covered by patents, other manufacturers have recently introduced similar technology using comparable manufacturing methods.

The Dyna driver is sold to a single distributor that adds the shaft and grip and sells the driver to retail golf shops. Dyna first made its reputation with its driver. It became an instant hit with amateurs after a professional golfer won a tournament using the Dyna driver. Based on the name recognition from its driver, Dyna introduced a line of putters and then wedges. The wedges are sold to three different distributors and the putters to six different distributors. Specialty, high-end putters like Dynas have a retail price of $120 to $180 and drivers a retail price of $350 to $500. Golfers like to experiment with new equipment, especially when they are playing badly. Therefore, it is not uncommon for golfers to own several putters and switch among them during the year. Putter manufacturers seek to capitalize on this psychology with aggressive advertising campaigns. It is less common for players to switch among wedges as they do with putters. Because it takes several rounds of golf playing with a new wedge to get its feel and distance control, most players dont experiment as much with wedges as with putters, or even drivers.

Production process

All three clubs (drivers, wedges, and putters) use the same manufacturing process. Each of the three clubs consists of between 5 and 10 components. A component is a precisely machined piece of steel, brass, or titanium that Dyna buys from outside suppliers. The components are positioned in a jig, which is placed in a specially designed computer-controlled machine. This machine first heats the components to a very high temperature that fuses them together, then cools them, and polishes the finished club.

The factory is organized into five departments: Receiving, Engineering, Setup, Machining, and Packing. Before a production run begins, Receiving issues a separate order for each component comprising the club head and inspects each order when it arrives. Engineering ensures that the completed club heads meet the products specifications and maintains the operating efficiency of the machines. Because of the preciseness of the production process, Engineering is constantly having to issue Engineering change orders in response to small differences in purchased components. Setup first cleans out the machine and jigs, adjusts the machine to the correct settings to produce the desired club head, and then makes a few pieces to ensure the settings are correct. Machining contains several machines, page 525any of which can be used to manufacture drivers, wedges, or putters once it is equipped with the proper jigs and tools. Packing is responsible for packaging and shipping completed units.

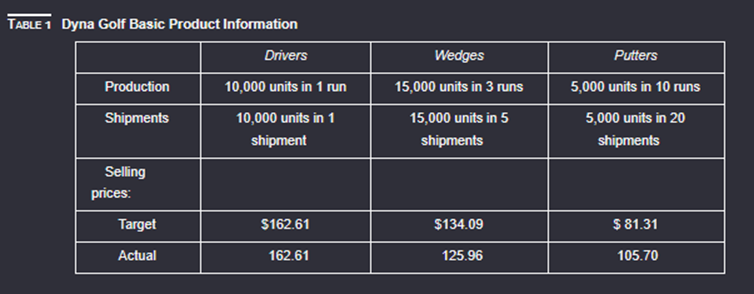

Table 1 summarizes the basic product information for the three products: production, shipments, target prices, and actual prices. For example, Dyna manufactured all 10,000 drivers in a single production run and shipped them all out in a single shipment. The 5,000 putters were manufactured in 10 separate runs and shipped in 20 shipments. Dyna set a target price for drivers to be $162.61 (wholesale price) and achieved it. However, it was not able to achieve its target price for wedges ($134.09 versus $125.96), but it exceeded its target price for putters ($105.70 versus $81.31).

Accounting system

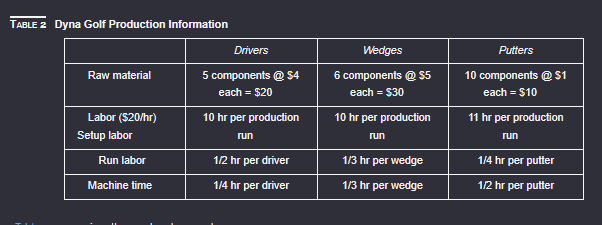

Table 2 summarizes raw material, setup and run labor, and machine time for each of the three products. Each product is produced in the machining department by assembling the metal components. Drivers require 5 components, whereas wedges and putters require 6 and 10 components, respectively. Before the production begins, the machine must be set up, requiring setup labor. Then to produce clubs, operating the machines requires both machine time and run labor time. Both setup and run labor cost $20 per hour. Machining has a total budget of $700,000, consisting of the depreciation on the machine, electricity, and maintenance. Drivers take more run labor time than machine time because several operators are required to operate the machinery when drivers are produced. During putter machining, the operator can be operating two machines at once.

Phil Meyers, Dynas controller, and Joe Bell meet a week after the executive committee meeting of the board of directors. Joe Bell asks Phil to report on what he has found. Phil begins,

Joe, as you know, our current accounting system assigns the direct material costs of the components and the direct labor for run time to the three products. Then it allocates all overhead costs, including setup time and machine costs, to the three products based on direct run labor dollars. page 526Setup labor is considered an indirect cost and is included in overhead. Based on these procedures we calculate our product costs for drivers, wedges, and putters to be $105.70, $87.16, and $52.85, respectively.

Ive been looking at our system and have become worried that our overhead rate is getting out of line. Its now over 750 percent of direct labor cost. Since weve introduced more automated machines, were substituting capital or overhead dollars for labor dollars. The Engineering department schedules its people based on change orders it receives. Drivers are pretty standard and only generate 25 percent of the change orders and wedges about 35 percent. Putters are our most complex production process and require the remainder of the change orders.

Im thinking we should refine our accounting system along the following lines. First, we should break out setup labor from the general overhead account and assign that directly to each product. We know how much time we are spending setting up each machine for each club-head run. Second, we should stop allocating receiving costs based on direct labor dollars but rather on raw material dollars. And third, the remaining overhead (excluding setup and receiving) should be allocated based on machine hours. If we make these three changes, I think well get a more accurate estimate of our products costs.

Joe Bell responded,

These seem to be some pretty major changes in our accounting system. Ill need some time to mull these over. Let me think about it and Ill let you know in a few days how to proceed.

Required:

What advice would you offer Joe Bell?

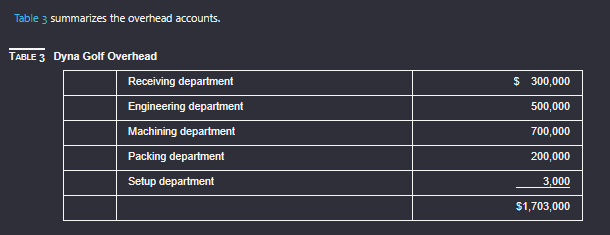

TABLE1 Dyna Golf Basic Product Information Table 3 summarizes the overhead accounts. TABLE3 Dyna Golf Overhead \begin{tabular}{|l|l|r|} \hline & Receiving department & $300,000 \\ \hline & Engineering department & 500,000 \\ \hline & Machining department & 700,000 \\ \hline & Packing department & 200,000 \\ \hline & Setup department & 3,000 \\ \hline & & $1,703,000 \\ \hline \end{tabular} TABLE2 Dyna Golf Production Information TABLE1 Dyna Golf Basic Product Information Table 3 summarizes the overhead accounts. TABLE3 Dyna Golf Overhead \begin{tabular}{|l|l|r|} \hline & Receiving department & $300,000 \\ \hline & Engineering department & 500,000 \\ \hline & Machining department & 700,000 \\ \hline & Packing department & 200,000 \\ \hline & Setup department & 3,000 \\ \hline & & $1,703,000 \\ \hline \end{tabular} TABLE2 Dyna Golf Production InformationStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Audit Or Iceland A Modern Myth Oberon Modern Plays

Authors: Andrew Westerside And Proto Type Theater

1st Edition

1786824671, 978-1786824677