Answered step by step

Verified Expert Solution

Question

1 Approved Answer

CASE 13 Insider Trading at the Galleon Group* INTRODUCTION The Galleon Group was a privately owned hedge fund firm that provided services and information

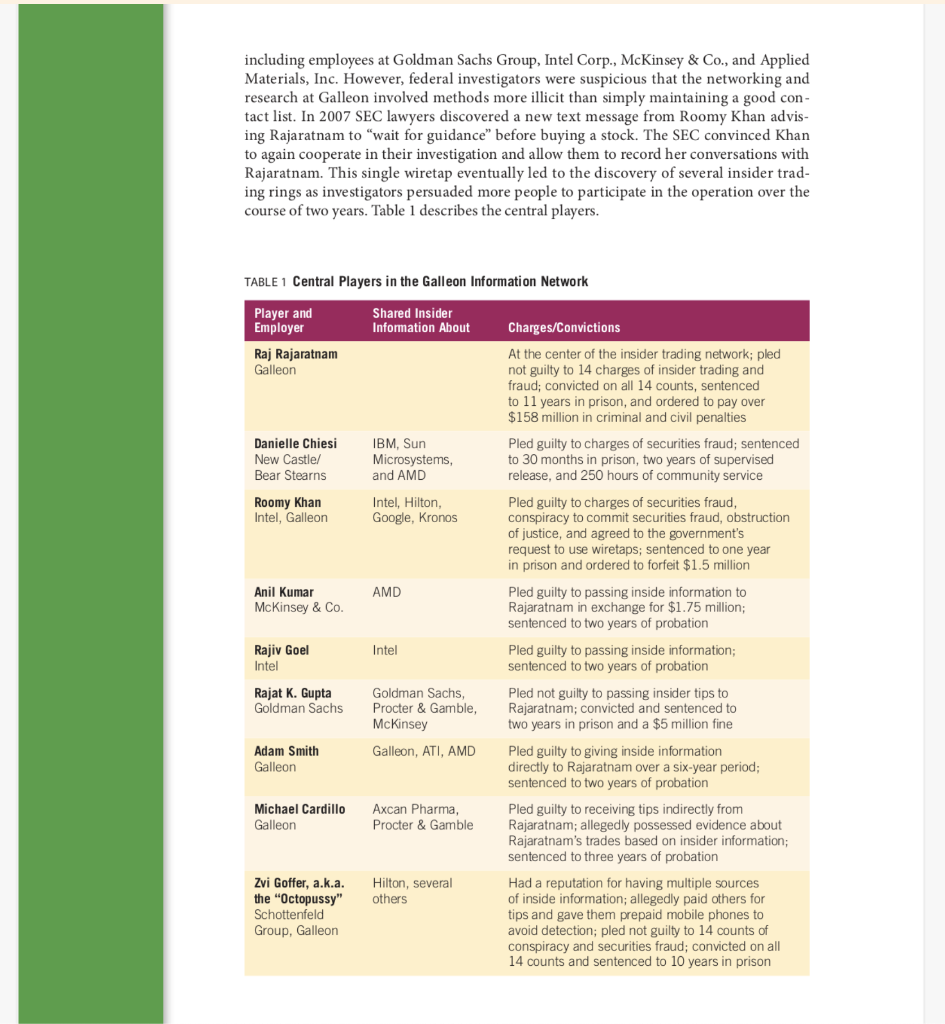

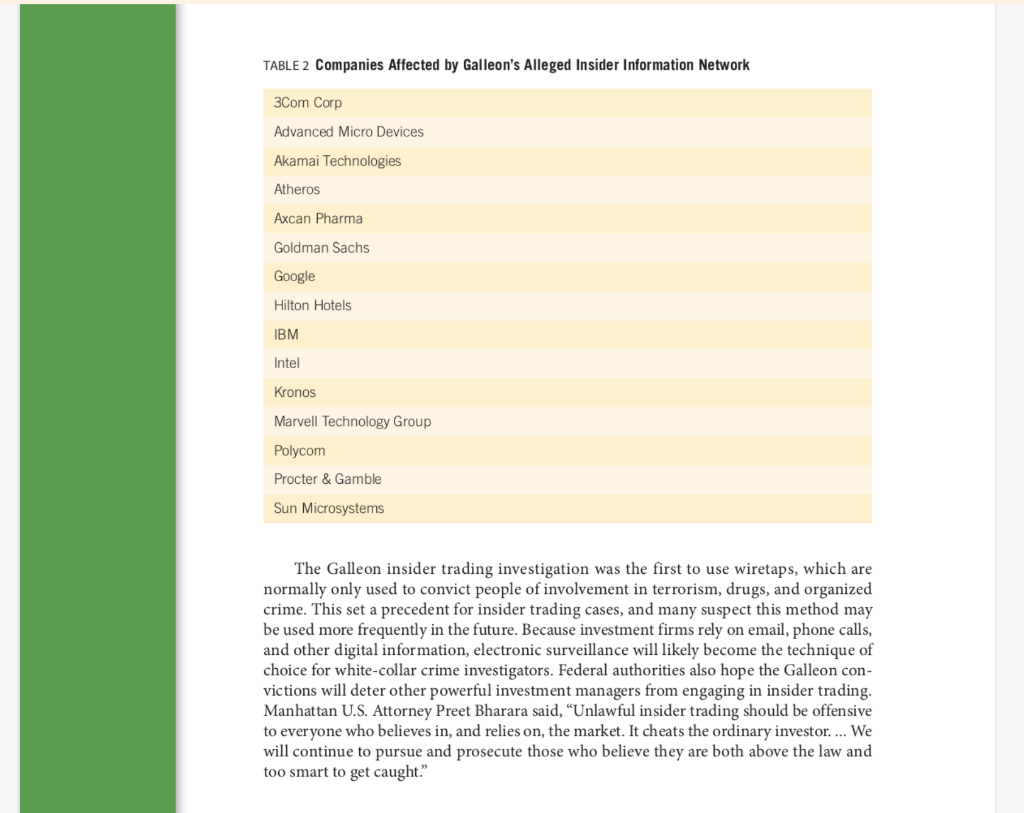

CASE 13 Insider Trading at the Galleon Group* INTRODUCTION The Galleon Group was a privately owned hedge fund firm that provided services and information about investments such as stocks, bonds, and other financial instruments. Galleon made money for itself and others by picking stocks and managing portfolios and hedge funds for investors. At its peak, Galleon was responsible for more than $7 billion in investor income. The company's philosophy was that it was possible to deliver supe- rior returns to investors without employing common high-risk tactics such as leverage or market timing. Founded in 1997, Galleon attracted employees from prestigious invest- ment firms such as Goldman Sachs, Needham & Co., and ING Barings. Every month the company held meetings where executives explained the status and strategy of each fund to investors. In addition, Galleon told investors that no employee would be personally trading in any stock or fund the investors held. In 2009 Raj Rajaratnam, the head of Galleon, was indicted on 14 counts of securities fraud and conspiracy, as well as sued by the Securities and Exchange Commission (SEC) for insider trading. He and five others were accused of using nonpublic information from com- pany insiders and consultants to make millions in personal profits. Rajaratnam's trial began in 2011, and although he pleaded not guilty, he was convicted on all 14 counts, fined over $158 million in civil and criminal penalties, and is currently serving an 11-year sentence. RAJ RAJARATNAM Rajaratnam, born in Sri Lanka to a middle-class family, received his bachelor's degree in engineering from the University of Sussex in England. In 1983 he earned his MBA from the University of Pennsylvania's Wharton School of Business. With a focus on the com- puter chip industry, he meticulously developed contacts. He went to manufacturing plants, talked to employees, and connected with executives who would later work with Galleon on their companies' initial public offerings. In 1985 the investment banking boutique Needham & Co. hired Rajaratnam as an ana- lyst. The corporate culture at Needham & Co. profoundly influenced Rajaratnam and his business philosophy. George Needham was obsessive about minimizing expenses, mak- ing employees stay in budget hotel rooms and take midnight flights to and from meetings. The company also urged analysts to gather as much information as possible. They were *This case was prepared by John Fraedrich, Harper Baird, and Michelle Urban. Isaac Emmanuel provided edito- rial assistance. It was prepared for classroom discussion rather than to illustrate either effective or ineffective han- dling of an administrative, ethical, or legal decision by management. All sources used for this case were obtained through publicly available material 2019. Case 13: Insider Trading at the Galleon Group encouraged to sift through garbage, question disgruntled employees, and even place people in jobs in target industries. Analysts went to professional meetings, questioned academics doing research and consulting, and set up clandestine agencies that collected information. At Needham & Co., Rajaratnam developed an aggressive networking and note-taking research strategy that enabled him to make accurate predictions about companies' financial situations. Rajaratnam rose rapidly through the ranks at Needham to become president of the company by 1991. Rajaratnam's personality also began to impact the company's culture. Rajaratnam once told a new analyst that Needham's name was on the company, but he was the real center of power, the one who "makes things happen." He began to push ethical limits when gathering information about companies. For example, concerns about Rajaratnam's activities ended stock brokerage Paine, Webber and Co.'s interest in buying Needham. Soon, similar worries spurred complaints from some inside Needham. By 1996, at least five Needham executives were concerned about Rajaratnam's conduct. Additionally, many of Needham's clients complained. Rajaratnam's multiple company roles as president, fund manager, and sometimes stock analyst were a potential conflict of interest situation; investment banks usually separate those roles to prevent clashes between the interests of clients and bank-run funds. In 1996, after 11 years at Needham, Rajaratnam left the com- pany and started the Galleon Group, taking several Needham employees with him. ACCUSATIONS OF INSIDER TRADING AT GALLEON At Galleon, Rajaratnam developed a flamboyant leadership style. During one meeting, Rajaratnam hired a dwarf to act as an analyst assigned to cover "small-cap" stocks. At another meeting, when Taser International, Inc. executives came to make an investment pitch, Rajaratnam offered $5,000 to anyone who would agree to be shocked. One trader, Keryn Limmer, volunteered to be shocked and was rendered unconscious. Rajaratnam also used his personal fortune to grow Galleon's business. For the 2007 Super Bowl, he threw a lavish party for wealthy investors and executives at a $250,000-a-week mansion on a man- made island in Biscayne Bay off the Florida coast. At the same time, Rajaratnam contributed to various causes promoting development in the Indian subcontinent, as well as programs benefiting lower-income South Asian youths in the New York area. He joined the board of the Harlem Children's Zone, an edu- cational nonprofit. He also raised nearly $7.5 million for victims of the 2004 South Asian tsunami. For his philanthropy, he was later honored with a symphony performance at the Lincoln Center in New York. However, Rajaratnam was already in trouble with the government. In 2005 he paid over $20 million to settle a federal investigation into a fake tax shelter used to hide $52 million from taxation. Rajaratnam and his business partner then sued their lawyers, claiming they had no idea the shelter was illegal; the pair was awarded $10 million in damages. Galleon also paid $2 million in 2005 to settle an SEC investigation into its stock trading practices. In addition, Intel discovered in 2001 that Roomy Khan, an Intel employee, had leaked infor- mation about sales and production to Rajaratnam. When Khan left Intel, she took a job with Galleon. Although Intel reported the incidents to the authorities, and Khan served six months of house arrest after pleading guilty to wire fraud and agreeing to cooperate in the investigation against Rajaratnam, the prosecutors could not prove that Rajaratnam actually made trades based on the inside information. As a result, the investigation was abandoned. Analysts live or die by the information they acquire on publicly traded firms. As such, there is a constant struggle to gather key information that can predict changes in stock prices, quarterly reports, and revenue. Rajaratnam had a deep network of acquaintances, including employees at Goldman Sachs Group, Intel Corp., McKinsey & Co., and Applied Materials, Inc. However, federal investigators were suspicious that the networking and research at Galleon involved methods more illicit than simply maintaining a good con- tact list. In 2007 SEC lawyers discovered a new text message from Roomy Khan advis- ing Rajaratnam to "wait for guidance" before buying a stock. The SEC convinced Khan to again cooperate in their investigation and allow them to record her conversations with Rajaratnam. This single wiretap eventually led to the discovery of several insider trad- ing rings as investigators persuaded more people to participate in the operation over the course of two years. Table 1 describes the central players. TABLE 1 Central Players in the Galleon Information Network Shared Insider Information About Player and Employer Raj Rajaratnam Galleon Danielle Chiesi New Castle/ Bear Stearns Roomy Khan Intel, Galleon Anil Kumar McKinsey & Co. Rajiv Goel Intel Rajat K. Gupta Goldman Sachs Adam Smith Galleon Michael Cardillo Galleon Zvi Goffer, a.k.a. the "Octopussy" Schottenfeld Group, Galleon IBM, Sun Microsystems, and AMD Intel, Hilton, Google, Kronos AMD Intel Goldman Sachs, Procter & Gamble, McKinsey Galleon, ATI, AMD Axcan Pharma, Procter & Gamble Hilton, several others Charges/Convictions At the center of the insider trading network; pled not guilty to 14 charges of insider trading and fraud; convicted on all 14 counts, sentenced to 11 years in prison, and ordered to pay over $158 million in criminal and civil penalties Pled guilty to charges of securities fraud; sentenced to 30 months in prison, two years of supervised release, and 250 hours of community service Pled guilty to charges of securities fraud, conspiracy to commit securities fraud, obstruction of justice, and agreed to the government's request to use wiretaps; sentenced to one year in prison and ordered to forfeit $1.5 million Pled guilty to passing inside information to Rajaratnam in exchange for $1.75 million; sentenced to two years of probation Pled guilty to passing inside information; sentenced to two years of probation Pled not guilty to passing insider tips to Rajaratnam; convicted and sentenced to two years in prison and a $5 million fine Pled guilty to giving inside information directly to Rajaratnam over a six-year period; sentenced to two years of probation Pled guilty to receiving tips indirectly from Rajaratnam; allegedly possessed evidence about Rajaratnam's trades based on insider information; sentenced to three years of probation Had a reputation for having multiple sources of inside information; allegedly paid others for tips and gave them prepaid mobile phones to avoid detection; pled not guilty to 14 counts of conspiracy and securities fraud; convicted on all 14 counts and sentenced to 10 years in prison ARREST AND TRIAL In October 2009, Raj Rajaratnam was arrested on 14 charges of securities and wire fraud. At the same time, the SEC filed civil insider trading charges against him. Rajaratnam was released on a $100 million bond and immediately hired several top defense attorneys and public relations specialists. His criminal trial began in March 2011. The laws on insider trading are vague and often make it difficult to convict white- collar criminals. Prosecutors had to prove Rajaratnam not only traded on information he knew was confidential but also that the information was important enough to affect the price of a company's stock. The government's main evidence consisted of 45 recorded. phone calls between individuals suspected of insider trading, including six witnesses who had already pled guilty and were aiding federal investigators. In many of these phone calls, Raj Rajaratnam discussed confidential information with investors and insiders before the information was released to the public. In one recording, Rajaratnam told employees to cover up evidence of insider trading. Another recording suggests Rajaratnam received a tip from someone on Goldman Sachs board that the company's stock price was going to decrease. That information had been presented at a confidential Goldman Sachs board meeting only a day earlier. The challenge for the prosecution was to prove Rajaratnam used these tips to make illicit trades. Wiretaps of conversations between Goldman Sachs board member Rajat Gupta and Rajaratnam, along with Rajaratnam's subsequent actions, imply this occurred. instance, during a board meeting on September 23, 2008, Goldman Sachs board mem- bers discussed a $5 billion preferred stock investment in Goldman Sachs by Berkshire Hathaway along with a public equity offering. According to the prosecution, a few minutes after the meeting, Gupta called Rajaratnam. That same day, just before the market closed, Galleon bought 175,000 shares in Goldman Sachs stock. The news about Berkshire Hatha- way was publicly announced after the market closed, and the next morning the stock went from $125.05 to $128.44. Galleon liquidated the stock and generated a profit of $900,000. The government had several key witnesses from the insider trading rings who cooper- ated with investigators. Before the start of Rajaratnam's trial, 19 members of the Galleon network pled guilty to charges of insider trading, and some agreed to testify against Rajaratnam. Anil Kumar, who pleaded guilty to providing insider information in exchange for over $1.75 million wired to a secret offshore account, told the jury that Rajaratnam offered to hire him as a consultant but told him that he did not want traditional industry research. Rajaratnam also told Kumar his ideas were worth a lot of money. The prosecution argued that Rajaratnam corrupted his friends and employees in order to make profits for himself and Galleon. In the closing argument, Assistant U.S. Attor- ney Reed Brodsky highlighted that Rajaratnam used his contacts to gain certainty in areas where everyone else had none. In order to convict Rajaratnam of insider trading, the government had to prove the information he received could only have been acquired via inside sources. Rajaratnam's defense maintained that some of the information Rajaratnam used was publicly available and he was not aware other information had not been publicly disclosed. The defense argued Galleon's public announcements, press releases, investor meetings, government fil- ings, and additional sources showed that the information had appeared days and weeks before Rajaratnam and others used that information. Good investment advisors are in the business of acquiring, analyzing, and making calculated predictions so their clients' investments increase. The defense attorneys argued that Rajaratnam's access to corporate executives was the reason his investors hired him. The defense also claimed these same TUIL executives were aware of the law and of their own duties to their employers and sharehold- ers, and they should have known what they could and could not say about their businesses, whereas Rajaratnam's obligations were to his investors. Rajaratnam lost money on some of the trades the government said were based on inside information. The defense argued that if he had insider information, the opposite should be true. The defense maintained that Galleon's analysts were right only about half of the time, and if they were cheating, they should have been right all of the time. The defense also questioned the validity of some of the prosecution's witnesses. For example, one witness confessed to the fabrication of a false affidavit, doctor's letter, tax forms, and bank letters, allegedly to protect his original statements to the prosecution. The defense argued that many of the prosecution's witnesses lied to save themselves from heavier prison terms for unrelated misdeeds. Anil Kumar testified that between 2004 and 2009, he gave material nonpublic information about several companies to Rajaratnam. However, although Galleon's records show that it paid Kumar consulting fees, he never shared these consulting fees with his McKinsey partners, instead hiding them in shell companies in overseas bank accounts and failing to report them on his tax returns. Then there is Rajiv Goel, who allegedly gave Rajaratnam material nonpublic information obtained from his employer, Intel. The defense brought out that Goel filed false tax returns unrelated to Rajaratnam and was therefore facing prison time (he was later sentenced to two years of probation). The only way out for these criminals caught red-handed, the defense argued, was to testify against Rajaratnam. THE VERDICT After 12 days of deliberation, the jury found Raj Rajaratnam guilty of all 14 counts of secu- rities fraud and conspiracy. The jurors later explained the length of their deliberation was because some of them could not comprehend how such an intelligent person could do something so destructive. Jurors cited the recorded conversations between Rajaratnam and his trading network as some of the most convincing evidence. In total, the counts carried a potential maximum sentence of 205 years in prison, although Rajaratnam was actually only sentenced to 11 years. In addition to his prison sentence, his criminal penalties amounted to $63.8 million. Rajaratnam also lost the SEC's parallel civil lawsuit for insider trading and was ordered to pay a record $92.8 million in damages, the largest judgment ever imposed against one person in an SEC insider trading case. He later agreed to pay an additional $1.45 million to settle yet more civil charges. These various judgments added up to over $158 million in total penalties. Rajaratnam and his defense team swiftly appealed the criminal conviction. Their argument centered on the aggressive wiretapping the federal investigators had employed to gather their evidence, a tactic never before used in an insider trading case. The appeal stated that judicial permission to place these wiretaps had been obtained deceptively in violation of Rajaratnam's constitutional rights, and thus the incriminating recorded con- versations should not have been usable by the prosecution at trial. The federal court of appeals, however, found Rajaratnam's arguments "unpersuasive" and upheld his convic- tion. The U.S. Supreme Court then declined to hear the case, making Rajaratnam's sen- tence final. Rajaratnam appealed the $92.8 million civil fine, claiming it is unfairly excessive and cumulative with the $63.8 million criminal penalty. He also tried to appeal his conviction, claiming that it had not been proven that benefits were passed on to the tippers. A judge rejected his argument. RAJAT GUPTA Rajat Gupta was a man of high profile and influence with an illustrious career, includ- ing a nine-year term as managing director (CEO) of McKinsey & Co., a prestigious global management consulting firm, and serving on the boards of Goldman Sachs, Procter & Gamble, American Airlines, the Rockefeller, and the Bill and Melinda Gates Foundation. Well-known, well-respected, and considered a man of integrity, he was esteemed through- out the financial services sector, as well as in India for being the first Indian-born CEO of a multinational corporation. This golden reputation came to an abrupt end when he was charged and convicted of insider trading activities in 2012. The charges were based on the phone call he made to Rajaratnam on September 23, 2008, regarding Berkshire Hathaway's purchase of Goldman Sachs stock. Immediately after this phone call, Galleon made a significant purchase of Goldman Sachs stock, turned a sizeable profit, and quickly liquidated the stock. Because of this sequence of events, and other similar incidents where Gupta contacted Rajaratnam just prior to especially profit- able trading decisions by Rajaratnam and Galleon, Gupta was implicated in insider trad- ing activity. After less than a day of deliberation, the jury convicted him of three counts of securities fraud and one count of criminal conspiracy. Rajat Gupta faced a maximum of 20 years for each fraud charge, and five years for the conspiracy charge, but was only sentenced to two years in prison, as well as fined a total of $24.9 million in civil and criminal penalties. Gupta's appeal rested on the use of wiretap evidence that his defense argued was hear- say and thus inadmissible at trial under evidentiary rules. His lawyers also maintained there was no evidence Gupta benefited in any way from giving the alleged insider tips and that the conviction was based entirely on circumstantial evidence. The appeal furthermore claimed the defense team was prevented from presenting several pieces of critical evidence, including that of Gupta's nonculpable state of mind, of the possibility that an alternative person had actually provided the insider tips, and of Gupta's integrity. Because the court allowed the wiretap recordings but did not allow this evidence, Gupta's defense argued that he deserved a new trial. Despite these arguments, the federal court of appeals upheld Gupta's conviction, and subsequently denied his petition for a rehearing. Gupta tried to appeal to the U.S. Supreme Court, but his request to remain free on bail during this appeal was denied, and he reported to prison on June 17, 2014. Rajat Gupta has since left prison and is seeking to reestablish his prominent reputation. He continues to fight the charges, and in 2016 the U.S. Second Court of Appeals agreed to reexamine its previous rejection of Gupta's appeal. Gupta's lawyer argued that Gupta did not receive any benefit from Rajaratnam for sharing information with him. Many consider Gupta's conviction-considering his prominence and influence-to be a powerful symbolic victory for federal prosecutors and the SEC, sending a message to the financial sector that no wrongdoer, no matter how powerful, is safe from recrimination. THE IMPACT OF THE GALLEON CASE The Galleon case is the largest investigation in history into insider trading within hedge funds. Twenty-six people were charged with fraud and conspiracy. Galleon closed in 2009 after investors quickly withdrew over $4 billion in investments from the company. In addi- tion, over a dozen companies' stocks were traded based on allegedly nonpublic informa- tion (see Table 2). These trades could have affected the financial status of the companies, their stock prices, and their shareholders. TABLE 2 Companies Affected by Galleon's Alleged Insider Information Network 3Com Corp Advanced Micro Devices Akamai Technologies Atheros Axcan Pharma Goldman Sachs Google Hilton Hotels IBM Intel Kronos Marvell Technology Group Polycom Procter & Gamble Sun Microsystems The Galleon insider trading investigation was the first to use wiretaps, which are normally only used to convict people of involvement in terrorism, drugs, and organized crime. This set a precedent for insider trading cases, and many suspect this method may be used more frequently in the future. Because investment firms rely on email, phone calls, and other digital information, electronic surveillance will likely become the technique of choice for white-collar crime investigators. Federal authorities also hope the Galleon con- victions will deter other powerful investment managers from engaging in insider trading. Manhattan U.S. Attorney Preet Bharara said, "Unlawful insider trading should be offensive to everyone who believes in, and relies on, the market. It cheats the ordinary investor. ... We will continue to pursue and prosecute those who believe they are both above the law and too smart to get caught." QUESTION Are the information-gathering techniques like Rajaratnam's common on Wall Street? If so, what could regulators, investors and executives do to reduce the practice? NEED 3 DETAILED PARAGRAPHS

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Yes InformationGathering Techniques Like Rajaratnams Are Common on Wall Street In the highly competitive and fastpaced world of Wall Street informatio...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Ethics Ethical Decision Making and Cases

Authors: O. C. Ferrell

11th Edition

1305500846, 1305500849, 9781305856233 , 978-1305500846