Question

Case 2.0: Introduction to Competitive Markets Demand and Supply Analysis Part A: Demand and Supply, and the Market Equilibrium suppose that the quantity demanded is

Case 2.0: Introduction to Competitive Markets Demand and Supply Analysis

Part A: Demand and Supply, and the Market Equilibrium

suppose that the quantity demanded is given by the equation, QD = 18 P. If you want, you can show this in schedule or table form in a spreadsheet, we get P = 36 2QD.

Now suppose that supply is given by QS = -6 + P for all P > 6.

Inverse supply is P = 6 + QS.

The graph below shows the inverse demand and supply curves:

18 P = -6 + P, which, rearranged, is (3/2) P = 24. Solve this equality to find the equilibrium price, and then put the price you find back into your equations for demand and supply to find the equilibrium quantity. Enter the numbers you find into the highlighted boxes in the diagram above???

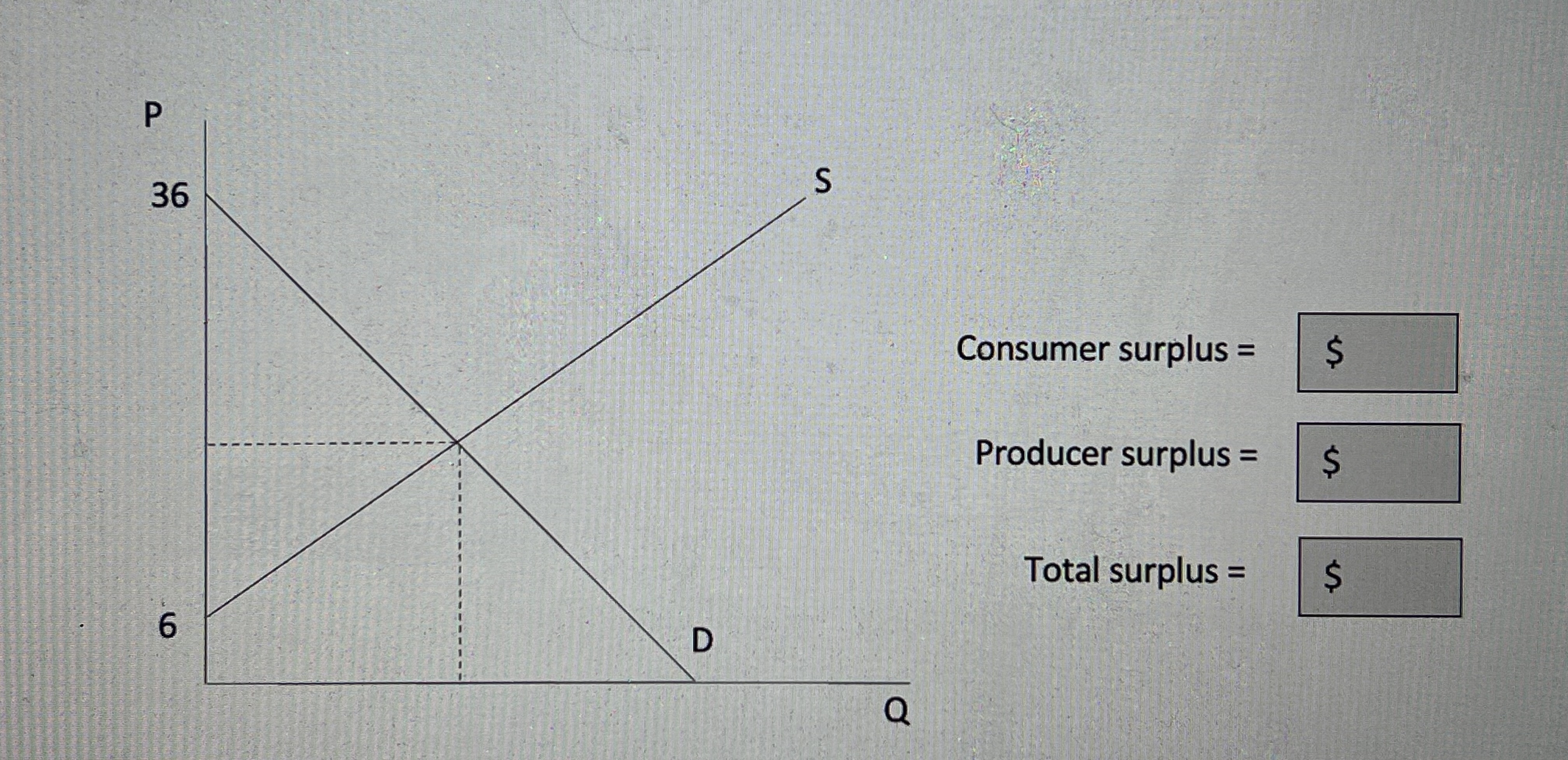

Part B: Welfare Analysis - Consumer and Producer Surplus

We break this gain out and measure it using consumer and producer surplus. Consumer surplus is the value of the consumers benefit minus the price the consumer pays; producer surplus is the price the firm receives over and above the opportunity (or marginal) cost of production. For example, suppose a consumer values a good at $7, and it costs a firm $4 to make the good. If the firm sells the good for $5 to the consumer in a competitive market, then for this unit of the good, consumer surplus is $2 and producer surplus is $1. (Note that producer surplus is similar to profit, except without an adjustment for fixed costs.) Measured across all units of a good on a diagram of a competitive market, consumer surplus is the area below the demand curve but above the equilibrium price line, and producer surplus is the area below the equilibrium price level but above the supply curve. If the demand and supply curves are straight lines, these areas are triangles, conveniently, and their respective areas are easy to calculate using the 1/2 x base x height formula for triangles.

Find these values for the market for which you found the equilibrium in the previous section???

Part C: Price Controls and Their Effects

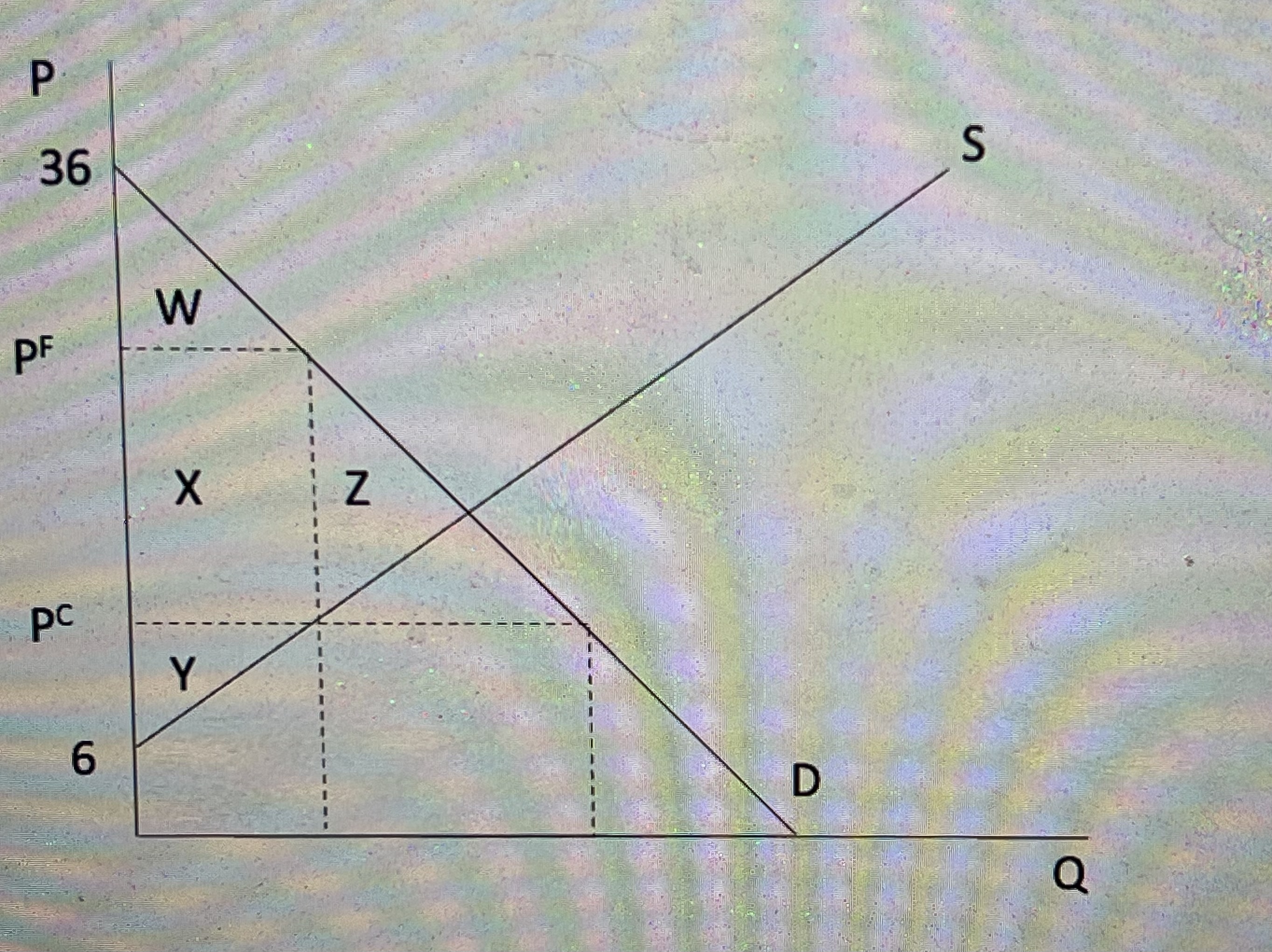

Suppose that the government decides to impose a price ceiling in this market that is, a maximum legal price that it rigorously enforces of $12 per unit. You will recall that QD = 18 P and thus P = 36 2QD, and QS = -6 + P and so P = 6 + QS. Lets find the effects of this price ceiling using a modified supply and demand diagram:??????

The most obvious effect of a price ceiling (PC on the diagram) below the equilibrium price is to create a shortage: more is demanded than is supplied at a price of $12. Lets find the shortage:

| The quantity demanded at $12 is | |

| The quantity supplied at $12 is | |

| The shortage at $12 is |

The intent of the law is to create greater consumer surplus, even if the total quantity sold is reduced this would be areas W + X. However, the overall shortage in the market is going to cause a problem for consumers: since theres not enough to go around at the price PC the people who most badly want the good will have to line up first to ensure they get the good or pay someone to get in line for them. (This is a classic image from the era of the Soviet Union (PF on the diagram)

| The full economic price is | $ |

To be clear: when there is a shortage, buyers who actually get the good will pay in two ways an actual dollar price (determined by the price ceiling) and the price of standing in line or doing whatever it takes to actually get the good. This latter price is sometimes called the non-pecuniary or non-monetary price. The full economic price is the sum of the two. So in this case

| The non-pecuniary price is | $ |

If we think of time spent waiting in line as a wasted resource, then we will not want to count it in consumer surplus. Pure consumer surplus now would in fact only be area W. [Note that Im using a somewhat stricter interpretation than the text here but I think Im right! ] So lets summarize our welfare findings so far:

| Producer surplus, area Y, is | $ |

| Consumer surplus, area W, is | $ |

| Total surplus, areas Y + W, is | $ |

Now lets consider areas X and Z in our diagram. Area Z would be split between consumer and producer surplus if the market went to its equilibrium, but that area is now lost entirely because of the decrease in production. The text calls this lost social welfare due to a price ceiling or more simply, deadweight loss. Deadweight loss is a measure of inefficiency due to market failure or intervention that destroys part of the welfare generated by trade. Area X might also be considered lost social welfare though, if the resources consumed by waiting in line could have been productively used elsewhere. In fact, this area is likely to be larger than the traditional deadweight loss triangle of area Z. Lets calculate both and summarize:

| Traditional deadweight loss, area Z, is | $ |

| Additional social welfare loss, area X, is | $ |

| Total lost welfare from the price ceiling: | $ |

Part D: Comparative Statics

Suppose demand is given by the equation QD = 12 + 2M P, which includes a new term, M, for income. One quick insight: this good must be a normal good because the positive coefficient on income indicates that demand rises as income goes up, as would be true for most goods, but not inferior goods. If M = 3, then putting that figure into the demand function we get QD = 18 P, and we have exactly the same demand we have been working with in our examples so far. Now lets suppose that income rises to M = 6.

Plugging M = 6 into the demand equation, we get QD = 24 P. Assume supply continues to be

QS = -6 + P. Inverse demand and supply will now be P = 48 2QD and P = 6 + QS. (And assume the price control from Part C no longer exists either.)

Our new diagram will look like this, with D1 showing the original demand and D2 showing the new demand curve:

Find the price and quantity at the new equilibrium, and put these values in the boxes in the diagram. Then calculate the new values for consumer, producer, and total surplus and enter them below.

| New consumer surplus: | $ |

| New producer surplus: | $ |

| New total surplus: | $ |

Consumer surplus = Producer surplus = Total surplus = Consumer surplus = Producer surplus = Total surplus =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How To Audit Document Control System Based On ISO 9001 2015

Authors: Folarin Omojoye

1st Edition

B09892NF88, 979-8525615175