Answered step by step

Verified Expert Solution

Question

1 Approved Answer

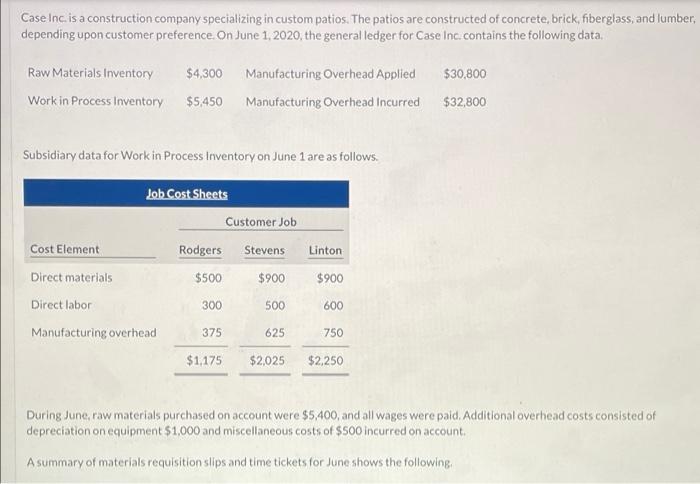

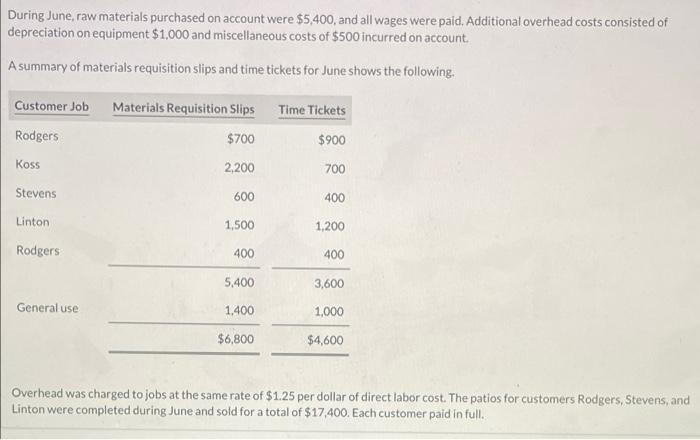

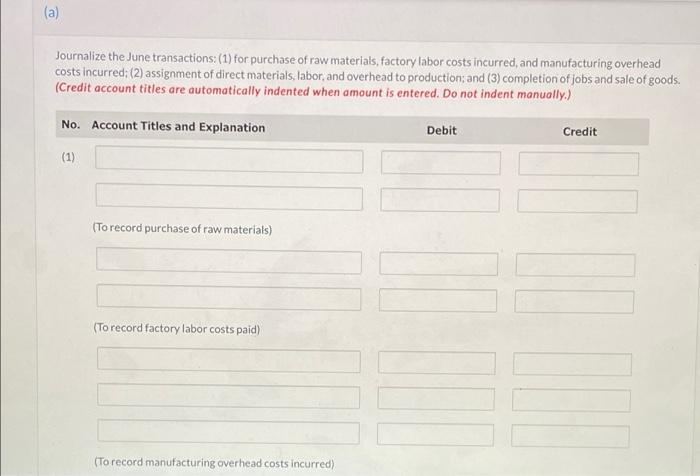

Case Inc. is a construction company specializing in custom patios. The patios are constructed of concrete, brick, fiberglass, and lumber, depending upon customer preference. On

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Value Added Auditing Standard Manual Of Risk Based Process Auditing CERM Academy Series On Enterprise Risk Management

Authors: Gregory Hutchins

3rd Edition

0965466582, 978-0965466585