Question

Case Number 08: LaJolla Engineering Services Meaghan OConnor had inherited a larger set of problems in the Engineering Equipment Division than she had ever expected.

Case Number 08: LaJolla Engineering Services

Meaghan OConnor had inherited a larger set of problems in the Engineering Equipment Division than she had ever expected. After taking over as the CFO of the Division in March 2004, Meaghan had discovered that LaJollas Engineering Equipment Divisions Latin American subsidiaries were the source of recent losses and growing income threats. The rather unusual part of the growing problem was that both the losses and the threats were arising from currency translation.

Latin American Subsidiaries

LaJolla was a multinational engineering services company with an established reputation in electrical power system design and construction. Although most of LaJollas business was usually described as services, and therefore using or owning few real assets, that was not the case with the Engineering Equipment Division. This specific business unit was charged with owning and operating the very high-cost and specialized heavy equipment involved in certain electrical power transmission and distribution system construction. In Meaghans terminology, she was in charge of the Big Iron in a company of consultants.

LaJollas recent activity had been focused in four countries: Argentina, Jamaica, Venezuela, and Mexico. And unfortunately, the last few years had not been kind to the value of these currenciesparticularly against the U.S. dollar. Each of LaJollas subsidiaries in these countries was local currency functional. Each subsidiary generated the majority of its revenues from local service contracts, and many of the operating expenses were also local. But each of the units had invested in some of the specialized equipmentthe so-called Big Ironwhich had led to net exposed assets when LaJolla had completed its consolidation of foreign activities each year for financial reporting purposes. The translation gains and losses (mostly losses in recent years as the Argentine peso, Jamaican dollar, Venezuelan bolivar, and Mexican peso had weakened against the U.S. dollar), had accumulated in the cumulative translation adjustment line item on the companys consolidated books. But the problem had become more real of late.

Ordinarily, these translation losses would not have been a large managerial issue for LaJolla and Meaghan, except for a minor document filing error in Argentina in the fall of 2003. LaJolla, like many multinational companies operating in Argentina in recent years, had simply given up on conducting any real business of promise in the severely depressed post-crisis Argentina. It had essentially closed up shop there in the summer of 2003. But its legal counsel in Buenos Aires had made a mistake. Instead of ceasing current operations and mothballing the existing assets of LaJolla Engineering Argentina, the local counsel had filed papers stating that LaJolla was liquidating the business. Although a minor issue in terms of distinction, according to U.S. GAAP and FAS 52, LaJolla would now have to realize in current earnings the cumulative translation losses that had grown over the years from the Argentine business. And they were substantial. It had resulted in the recognition of $7 million in losses in the fourth quarter of 2003; LaJollas management had not been happy.

LaJolla 2004

As a result of this recent experience, LaJolla was taking a close look at all of the translation gains and losses of its various business units worldwide. Once again, the companys Latin American operations were the focal point, as collectively many of the Latin currencies had weakened recently against the dollar, although the dollar itself was quite weak against the euro. Jamaica, Venezuela, and Mexico each posed their individual problems and challenges, but all posed translation adjustment threats to LaJolla.

Jamaica

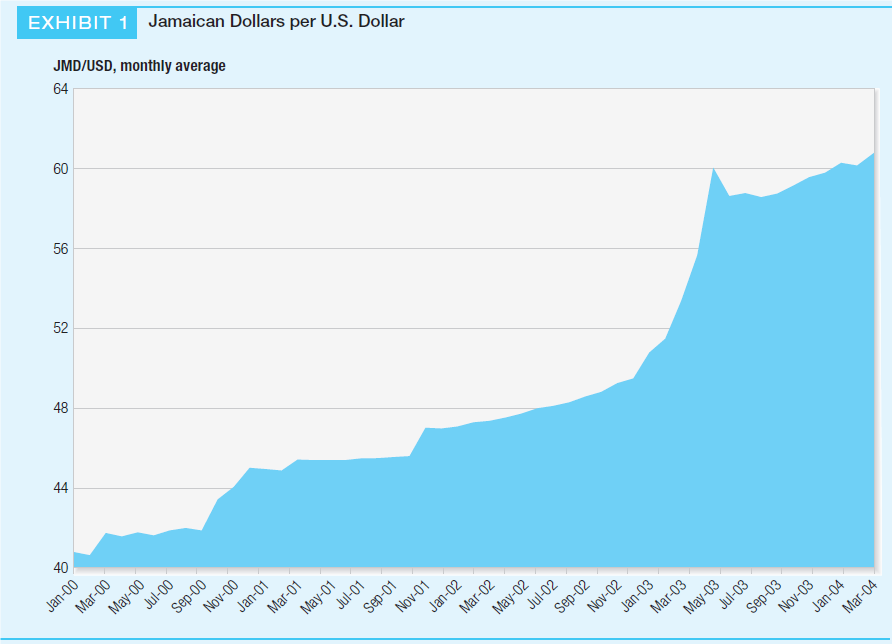

The company had been fairly concerned about the Jamaican business and its contracts from the very beginning. The company had initially agreed to take all revenues in Jamaican dollars (sealing the local currency functional currency designation), but after the fall of the Jamaican dollar in early 2003 had renegotiated a risk-sharing agreement. The agreement restructured the relationship to one where, although LaJolla would continue to be paid in local currency, the two companies would share any changes in the exchange rate beginning in the fourth quarter of 2003 when establishing the charges as invoiced. Regardless, the continuing decline of the Jamaican dollar (as seen in Exhibit 1) had created substantial translation losses for LaJolla in Jamaica.

Mexico

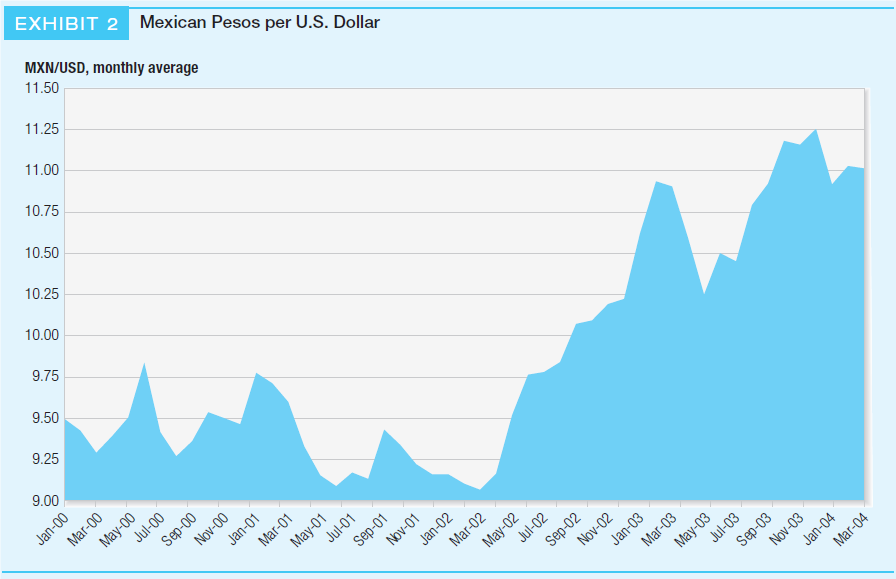

Although the Mexican peso had been quite stable for a number of years, it clearly had started to slide against the dollar in 2002 and 2003, as illustrated in Exhibit 2. Meaghan had become particularly frustrated with the Mexican situation the deeper she looked into it. LaJolla had only initiated the subsidiarys operations in Mexico in early 2000, yet the reported translation losses from Mexico had grown much more rapidly than what she would have expected. She had also become quite agitated when she realized that the financial reports coming from her Mexican offices were seemingly writing-up the translation losses every quarter. When she had asked questions, first by phone and then later in person, her local financial controller simply stopped talking (she was working through an interpreter), claiming they simply did not understand her questions. Meaghan was no beginner in international finance, and also knew that Mexican financial statements did regularly index foreign currency denominated accounts in line with government published indexes of asset values related to currencies. She wondered if the indexing could be at the source of the rapid growth in translation losses.

Venezuela

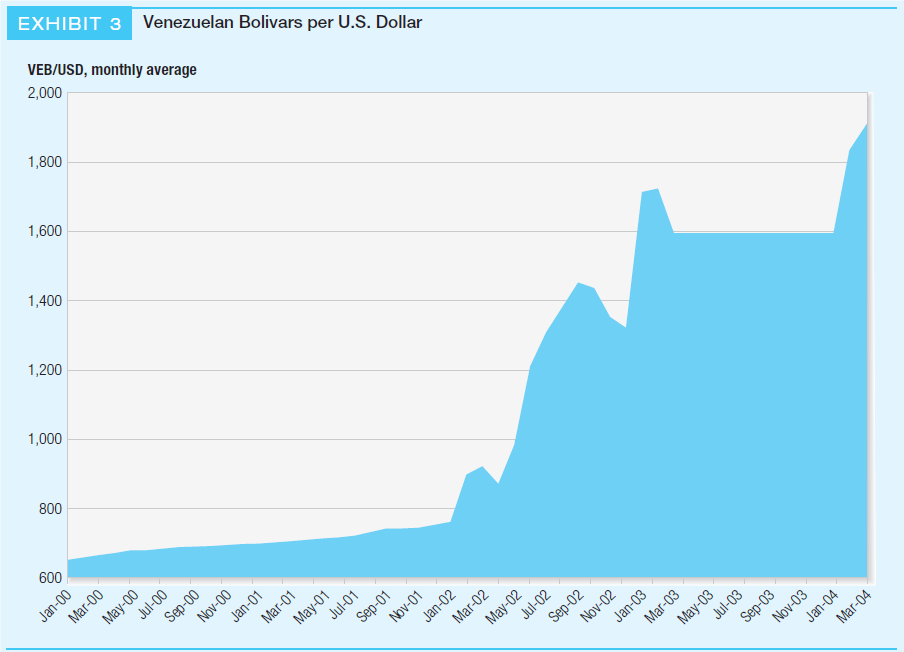

The continuing political crisis in Venezuela surrounding the presidency of Hugo Chavez had taken its toll on the Venezuelan bolivar, as seen in Exhibit 3. Not only was LaJolla suffering declining U.S. dollar proceeds from its Venezuelan operations, but also it had continued to suffer severe late payments from the various government agencies to which the company was exclusively providing services. The average invoice was now taking more than 180 days to be settled, and the bolivars decline had added to the losses. Translation losses were accumulating here, again from a subsidiary whose functional currency was the local currency. The LaJolla controller in Venezuela had faxed a proposal which would involve changing the currency used for the books in Venezuela to U.S. dollars, as well as a suggestion that they consider moving the subsidiary offshore (out of Venezuela) for accounting and consolidation purposes. He had suggested either the Cayman Islands or the Netherlands Antilles just off the coast. All in all, Meaghan was beginning to think she made a big mistake when she had accepted the promotion to CFO of this division. She turned her eyes once more to look out over the Pacific to ponder what alternatives she might have to manage these exposures, and whatif anythingshe should do immediately.

Case Questions

- Do you think Meaghan should spend time and resources attempting to manage translation losses, what many consider purely an accounting phenomenon?

- How would you characterize or structure your analysis of each of the individual country threats to LaJolla? What specific features of their individual problems seem to be intertwined with currency issues?

- What would you recommend that Meaghan do?

- What is the central problem involved in consolidating the financial statements of a foreign subsidiary?

PLEASE ANSWER THIS CASE STUDY AND PROVIDE ANSWERS TO ALL FOURS CASE QUESTIONS MENTIONED ABOVE.

EXHIBIT 1 Jamaican Dollars per U.S. Dollar JMD/USD, monthly average 64 60 56 52 48 44 40 Jan-00 May-00 Nov-00 Mar-00 Jul-00 Sep-00 Jan-01 Mar-01 May-01 Jul-01 Sep-01 Nov-01 Jan-02 Mar-02 May-02 Jul-02 Sep-02 Nov-02 Jan-03 Mar-03 May-03 Jul-03 Sep-03 Nov-03 Jan-04 Mar-04 EXHIBIT 2 Mexican Pesos per U.S. Dollar MXN/USD, monthly average 11.50 11.25 11.00 10.75 10.50 10.25 10.00 9.75 9.50 9.25 9.00 Jan-00 May-03 Mar-03 Jul-03 Sep-03 Nov-03 Jan-04 Mar-04 Mar-00 May-00 Jul-00 Sep-00 Nov-00 Jan-01 Mar-01 May-01 Jul-01 Sep-01 Nov-01 Jan-02 Mar-02 May-02 Jul-02 Sep-02 Nov-02 Jan-03 EXHIBIT 3 Venezuelan Bolivars per U.S. Dollar VEB/USD, monthly average 2,000 1,800 1,600 1,400 1,200 1,000 800 600 Jan-00 May-00 Sep-03 Jul-03 Mar-00 Nov-03 Jan-04 Mar-04 Jul-00 Sep-00 Nov-00 Jan-01 Mar-01 May-01 Jul-01 Sep-01 Nov-01 Jan-02 Mar-02 May-02 Jul-02 Sep-02 Nov-02 Jan-03 Mar-03 May-03Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Theory And Practice

Authors: Prasanna Chandra

8th Edition

0071078401, 978-0071078405