Case Solution and analysis review

Rothschild realized that the amount involved in the contract was such that an adverse move in the pound exchange rate could put Dozier in a loss position for 1986 if the transactions were left unhedged. On the other hand, he also became aware of the fact that hedging had its own costs. Still, a decision had to be made. He knew that no action implied that an unhedged position was the best alternative for the company. What are those decisions?

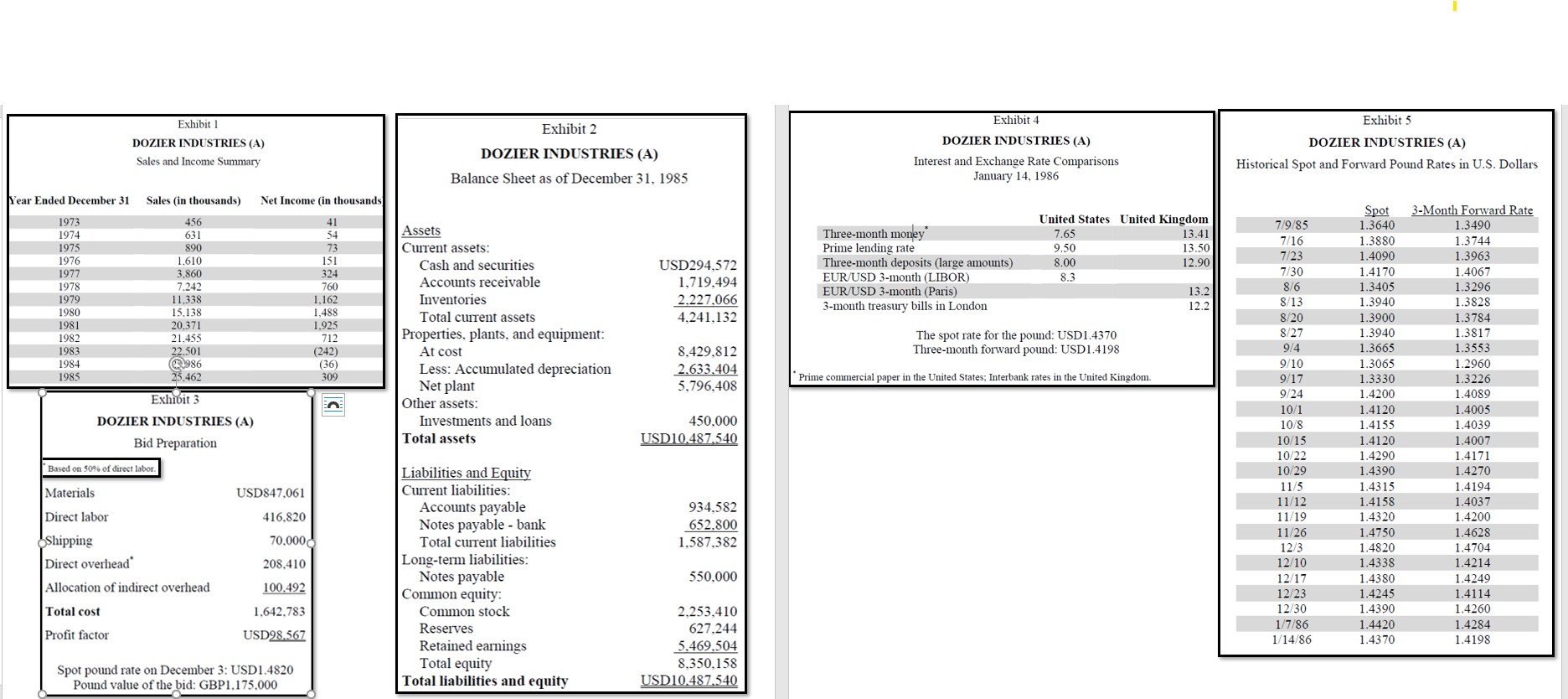

Dozier Industries En Richard Rothschild, the chief financial officer of Dozier Industries, returned to his office after meeting with two officers of Southeastern National Bank. He had requested the meeting to discuss financial issues related to Dozier's first major international sales contract, which had been confirmed the previous day, January 13, 1986. Initially, Rothschild had contacted Robert Leigh, a vice president of the bank, who had primary responsibilities for Dozier's business with Southeastern National. Leigh, feeling that he lacked the international expertise to answer all the questions Rothschild might raise, had suggested that John Gunn of the bank's International Division be included Foreign Exchange Risk and Hedging On January 13, the day the bid was accepted, the value of the pound was (U.S. dollars) USD1.4480. But the pound had weakened over the previous six weeks (see Exhibit 5). Rothschild was concerned that the value of the pound might depreciate even further during the next 90 days, and it was this worry that prompted his discussion at the bank. He wanted to find out what techniques were available to Dozier to reduce the exchange risk created by the outstanding pound receivable Gunn, the intemational specialist, had explained that Rothschild had several alternatives. First, of course, he could do nothing. This would leave Dozier vulnerable to pound fluctuations, which would entail losses if the pound depreciated, or gains if it appreciated versus the dollar. On the other hand, Rothschild could choose to hedge his exchange risk The meeting had focused on the exchange risk related to the new sales contract. Dozier's bid of (British pounds) GBP1.175 million to install an internal security system for a large manufacturing firm in the United Kingdom had been accepted. In accordance with the contract, the British firm had transferred a 10% deposit (GBP117.500), the balance due when the system was completed. Dozier's production vice president, Mike Miles, had assured Rothschild that there would be no difficulty in o completing the project within the 90-day period stipulated in the bid. As a result, Rothschild was planning on receiving GBP1.0575 million on April 14, 1986. Gunn explained that a hedge involved taking a position opposite to the one that was creating the foreign exchange exposure. This could be accomplished either by engaging in a forward contract or via a spot transaction Since Dozier had an outstanding pound receivable, the appropriate hedging transactions would be to sell pounds forward 90 days or to secure a 90-day pound loan. By selling pounds forward, Dozier would incur an obligation to deliver pounds 90 days from now at the rate established today. This would ensure that Dozier would receive a set dollar value for its pound receivable, regardless of the spot rate that existed in the future. Company History Dozier Industries, a relatively young firm specializing in electronic security systems, was established in 1973 by Charles L. Dozier, who was still president and the owner of 78% of the stock. The remaining 22% was held by other members of management. Dozier had formerly been a design engineer for a large electronics firm. In 1973 he began his own company to market security systems and began by concentrating on military sales. The company experienced rapid growth for almost a decade. But in 1982, as Dozier faced increased competition in this market, management attempted to branch out to design systems for small private firms and households. Dozier's inexperience in this market, combined with poor planning efforts, slowed sales growth and led to a severe reduction in profits (see Exhibit 1). The company shifted its focus to larger corporations and met with better success. In 1985, the company showed a profit for the first time in three years, and management was confident that the company had turned the corner. Exhibit 2 contains the balance sheet at the end of 1985. The spot hedge worked similarly in that it also created a pound obligation 90 days hence. Dozier would borrow pounds and exchange the proceeds into dollars at the spot rate. On April 13, Dozier would use its pound receipts to repay the loan. Any gains or losses on the receivable due to a change in the value of the pound would be offset by equivalent losses or gains on the loan payment. Leigh assured Rothschild that Southeastern National would be able to assist Dozier in implementing whatever decision Rothschild made. Dozier had a USD3 million line of credit with Southeastern National. John Gunn indicated that there would be no difficulty for Southeastern to arrange the pound loan for Dozier through its correspondent bank in London. He believed that such a loan would be at 1.5% above the U.K prime rate. In order to assist Rothschild in making his decision, Gunn provided him with information on interest rates, spot and forward exchange rates, as well as historical and forecasted information on the pound (see Exhibits 4, 5, and 6). Rothschild was aware that in preparing the bid, Dozier had allowed for a profit margin of only 6% in order to increase the likelihood of winning the bid and hence, developing an important foreign contact. The bid was submitted on December 3, 1985. In arriving at the bid, the company had estimated the cost of the project, added an amount as profit, but kept in mind the highest bid that could conceivably win the contract. The calculations were made in dollars and then converted to pounds at the spot rate existing on December 3 (see Exhibit 3), since the UK company had stipulated payment in pounds. O The company's management believed that sales to foreign corporations represented good prospects for future growth. Consequently, in the spring of 1985, Dozier had launched a marketing effort overseas. The selling effort had not met with much success until the confirmation of the contract discussed previously. The new sales contract, although large in itself, had the potential of being expanded in the future because the company involved was a large multinational firm with manufacturing facilities in many countries. Rothschild realized that the amount involved in the contract was such that an adverse move in the pound exchange rate could put Dozier in a loss position for 1986 if the transactions were left unhedged. On the other hand, he also became aware of the fact that hedging had its own costs. Still, a decision had to be made. He knew that no action implied that an unhedged position was the best alternative for the company. Exhibit 1 Exhibit 4 Exhibit 5 Exhibit 2 DOZIER INDUSTRIES (A) Sales and Income Summary DOZIER INDUSTRIES (A) DOZIER INDUSTRIES (A) Interest and Exchange Rate Comparisons January 14, 1986 DOZIER INDUSTRIES (A) Historical Spot and Forward Pound Rates in U.S. Dollars Balance Sheet as of December 31, 1985 Year Ended December 31 Sales (in thousands) Net Income in thousands 1973 1974 456 631 890 1.610 3.860 7.242 11.338 15.138 20.371 21.455 22.501 1975 1976 1977 1978 1979 12 1980 1981 1982 1983 1984 1985 41 54 73 151 324 760 1.162 1.488 1.925 712 (242) (36) 309 USD294,572 1,719,494 2.227.066 4.241.132 United States United Kingdom 7.65 13.41 9.50 13.50 8.00 12.90 8.3 13.2 12.2 Three-month money Prime lending rate Three-month deposits (large amounts) EUR/USD 3-month (LIBOR) EUR/USD 3-month (Paris) 3-month treasury bills in London Assets Current assets: Cash and securities Accounts receivable Inventories Total current assets Properties, plants, and equipment: At cost Less: Accumulated depreciation Net plant Other assets: Investments and loans Total assets The spot rate for the pound: USD1.4370 Three-month forward pound: USD1.4198 7/9/85 7/16 7/23 7/30 8/6 8/13 8/20 8/27 9/4 9/10 9/17 9/24 10/1 10/8 10/15 10/22 10/29 8.429.812 2.633.404 5.796,408 986 25.462 Prime commercial paper in the United States, Interbank rates in the United Kingdom. Exhibit 3 DOZIER INDUSTRIES (A) Bid Preparation 450.000 USD10.487.540 Spot 1.3640 1.3880 1.4090 1.4170 1.3405 1.3940 1.3900 1.3940 1.3665 1.3065 1.3330 1.4200 1.4120 1.4155 1.4120 1.4290 1.4390 1.4315 1.4158 1.4320 1.4750 1.4820 1.4338 1.4380 1.4245 1.4390 1.4420 1.4370 3-Month Forward Rate 1.3490 1.3744 1.3963 1.4067 1.3296 1.3828 1.3784 1.3817 1.3553 1.2960 1.3226 1.4089 1.4005 1.4039 1.4007 1.4171 1.4270 1.4194 1.4037 1.4200 1.4628 1.4704 1.4214 1.4249 1.4114 1.4260 1.4284 1.4198 Based on 50% of direct labor. 11/5 Materials USD847,061 Direct labor 416,820 934,582 652.800 1.587.382 70.000 Shipping Direct overhead Allocation of indirect overhead 208.410 Liabilities and Equity Current liabilities: Accounts payable Notes payable - bank Total current liabilities Long-term liabilities: Notes payable Common equity: Common stock Reserves Retained earnings Total equity Total liabilities and equity 550.000 11/12 11/19 11/26 12/3 12/10 12/17 12/23 12/30 1/7/86 1/14/86 100.492 Total cost 1.642,783 Profit factor USD98.567 2.253.410 627,244 5,469,504 8,350,158 USD10.487.540 Spot pound rate on December 3: USD1.4820 Pound value of the bid: GBP1.175.000 Dozier Industries En Richard Rothschild, the chief financial officer of Dozier Industries, returned to his office after meeting with two officers of Southeastern National Bank. He had requested the meeting to discuss financial issues related to Dozier's first major international sales contract, which had been confirmed the previous day, January 13, 1986. Initially, Rothschild had contacted Robert Leigh, a vice president of the bank, who had primary responsibilities for Dozier's business with Southeastern National. Leigh, feeling that he lacked the international expertise to answer all the questions Rothschild might raise, had suggested that John Gunn of the bank's International Division be included Foreign Exchange Risk and Hedging On January 13, the day the bid was accepted, the value of the pound was (U.S. dollars) USD1.4480. But the pound had weakened over the previous six weeks (see Exhibit 5). Rothschild was concerned that the value of the pound might depreciate even further during the next 90 days, and it was this worry that prompted his discussion at the bank. He wanted to find out what techniques were available to Dozier to reduce the exchange risk created by the outstanding pound receivable Gunn, the intemational specialist, had explained that Rothschild had several alternatives. First, of course, he could do nothing. This would leave Dozier vulnerable to pound fluctuations, which would entail losses if the pound depreciated, or gains if it appreciated versus the dollar. On the other hand, Rothschild could choose to hedge his exchange risk The meeting had focused on the exchange risk related to the new sales contract. Dozier's bid of (British pounds) GBP1.175 million to install an internal security system for a large manufacturing firm in the United Kingdom had been accepted. In accordance with the contract, the British firm had transferred a 10% deposit (GBP117.500), the balance due when the system was completed. Dozier's production vice president, Mike Miles, had assured Rothschild that there would be no difficulty in o completing the project within the 90-day period stipulated in the bid. As a result, Rothschild was planning on receiving GBP1.0575 million on April 14, 1986. Gunn explained that a hedge involved taking a position opposite to the one that was creating the foreign exchange exposure. This could be accomplished either by engaging in a forward contract or via a spot transaction Since Dozier had an outstanding pound receivable, the appropriate hedging transactions would be to sell pounds forward 90 days or to secure a 90-day pound loan. By selling pounds forward, Dozier would incur an obligation to deliver pounds 90 days from now at the rate established today. This would ensure that Dozier would receive a set dollar value for its pound receivable, regardless of the spot rate that existed in the future. Company History Dozier Industries, a relatively young firm specializing in electronic security systems, was established in 1973 by Charles L. Dozier, who was still president and the owner of 78% of the stock. The remaining 22% was held by other members of management. Dozier had formerly been a design engineer for a large electronics firm. In 1973 he began his own company to market security systems and began by concentrating on military sales. The company experienced rapid growth for almost a decade. But in 1982, as Dozier faced increased competition in this market, management attempted to branch out to design systems for small private firms and households. Dozier's inexperience in this market, combined with poor planning efforts, slowed sales growth and led to a severe reduction in profits (see Exhibit 1). The company shifted its focus to larger corporations and met with better success. In 1985, the company showed a profit for the first time in three years, and management was confident that the company had turned the corner. Exhibit 2 contains the balance sheet at the end of 1985. The spot hedge worked similarly in that it also created a pound obligation 90 days hence. Dozier would borrow pounds and exchange the proceeds into dollars at the spot rate. On April 13, Dozier would use its pound receipts to repay the loan. Any gains or losses on the receivable due to a change in the value of the pound would be offset by equivalent losses or gains on the loan payment. Leigh assured Rothschild that Southeastern National would be able to assist Dozier in implementing whatever decision Rothschild made. Dozier had a USD3 million line of credit with Southeastern National. John Gunn indicated that there would be no difficulty for Southeastern to arrange the pound loan for Dozier through its correspondent bank in London. He believed that such a loan would be at 1.5% above the U.K prime rate. In order to assist Rothschild in making his decision, Gunn provided him with information on interest rates, spot and forward exchange rates, as well as historical and forecasted information on the pound (see Exhibits 4, 5, and 6). Rothschild was aware that in preparing the bid, Dozier had allowed for a profit margin of only 6% in order to increase the likelihood of winning the bid and hence, developing an important foreign contact. The bid was submitted on December 3, 1985. In arriving at the bid, the company had estimated the cost of the project, added an amount as profit, but kept in mind the highest bid that could conceivably win the contract. The calculations were made in dollars and then converted to pounds at the spot rate existing on December 3 (see Exhibit 3), since the UK company had stipulated payment in pounds. O The company's management believed that sales to foreign corporations represented good prospects for future growth. Consequently, in the spring of 1985, Dozier had launched a marketing effort overseas. The selling effort had not met with much success until the confirmation of the contract discussed previously. The new sales contract, although large in itself, had the potential of being expanded in the future because the company involved was a large multinational firm with manufacturing facilities in many countries. Rothschild realized that the amount involved in the contract was such that an adverse move in the pound exchange rate could put Dozier in a loss position for 1986 if the transactions were left unhedged. On the other hand, he also became aware of the fact that hedging had its own costs. Still, a decision had to be made. He knew that no action implied that an unhedged position was the best alternative for the company. Exhibit 1 Exhibit 4 Exhibit 5 Exhibit 2 DOZIER INDUSTRIES (A) Sales and Income Summary DOZIER INDUSTRIES (A) DOZIER INDUSTRIES (A) Interest and Exchange Rate Comparisons January 14, 1986 DOZIER INDUSTRIES (A) Historical Spot and Forward Pound Rates in U.S. Dollars Balance Sheet as of December 31, 1985 Year Ended December 31 Sales (in thousands) Net Income in thousands 1973 1974 456 631 890 1.610 3.860 7.242 11.338 15.138 20.371 21.455 22.501 1975 1976 1977 1978 1979 12 1980 1981 1982 1983 1984 1985 41 54 73 151 324 760 1.162 1.488 1.925 712 (242) (36) 309 USD294,572 1,719,494 2.227.066 4.241.132 United States United Kingdom 7.65 13.41 9.50 13.50 8.00 12.90 8.3 13.2 12.2 Three-month money Prime lending rate Three-month deposits (large amounts) EUR/USD 3-month (LIBOR) EUR/USD 3-month (Paris) 3-month treasury bills in London Assets Current assets: Cash and securities Accounts receivable Inventories Total current assets Properties, plants, and equipment: At cost Less: Accumulated depreciation Net plant Other assets: Investments and loans Total assets The spot rate for the pound: USD1.4370 Three-month forward pound: USD1.4198 7/9/85 7/16 7/23 7/30 8/6 8/13 8/20 8/27 9/4 9/10 9/17 9/24 10/1 10/8 10/15 10/22 10/29 8.429.812 2.633.404 5.796,408 986 25.462 Prime commercial paper in the United States, Interbank rates in the United Kingdom. Exhibit 3 DOZIER INDUSTRIES (A) Bid Preparation 450.000 USD10.487.540 Spot 1.3640 1.3880 1.4090 1.4170 1.3405 1.3940 1.3900 1.3940 1.3665 1.3065 1.3330 1.4200 1.4120 1.4155 1.4120 1.4290 1.4390 1.4315 1.4158 1.4320 1.4750 1.4820 1.4338 1.4380 1.4245 1.4390 1.4420 1.4370 3-Month Forward Rate 1.3490 1.3744 1.3963 1.4067 1.3296 1.3828 1.3784 1.3817 1.3553 1.2960 1.3226 1.4089 1.4005 1.4039 1.4007 1.4171 1.4270 1.4194 1.4037 1.4200 1.4628 1.4704 1.4214 1.4249 1.4114 1.4260 1.4284 1.4198 Based on 50% of direct labor. 11/5 Materials USD847,061 Direct labor 416,820 934,582 652.800 1.587.382 70.000 Shipping Direct overhead Allocation of indirect overhead 208.410 Liabilities and Equity Current liabilities: Accounts payable Notes payable - bank Total current liabilities Long-term liabilities: Notes payable Common equity: Common stock Reserves Retained earnings Total equity Total liabilities and equity 550.000 11/12 11/19 11/26 12/3 12/10 12/17 12/23 12/30 1/7/86 1/14/86 100.492 Total cost 1.642,783 Profit factor USD98.567 2.253.410 627,244 5,469,504 8,350,158 USD10.487.540 Spot pound rate on December 3: USD1.4820 Pound value of the bid: GBP1.175.000