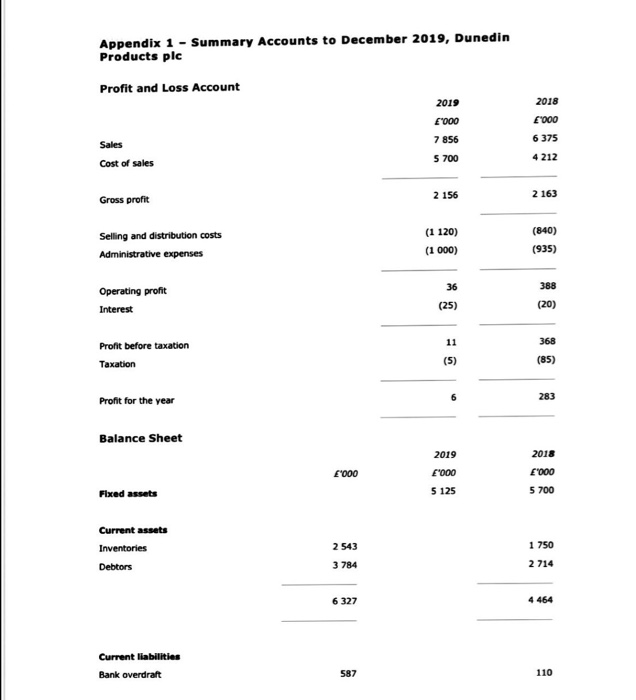

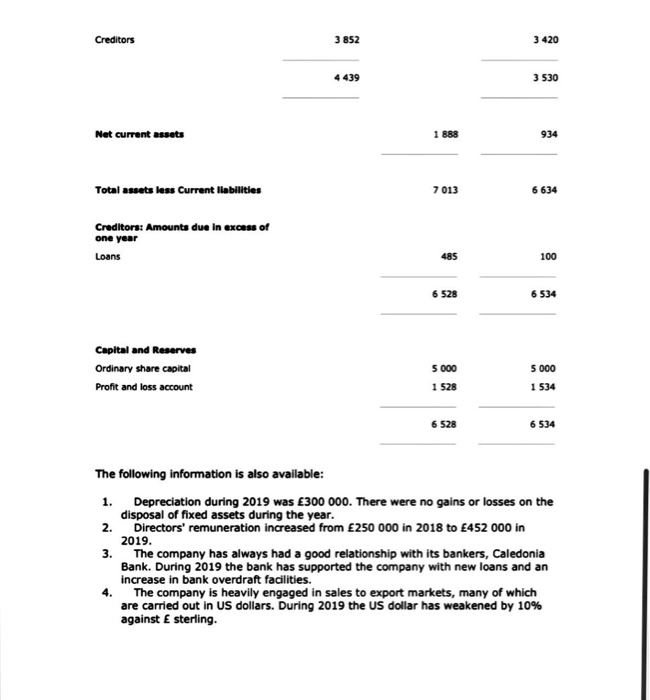

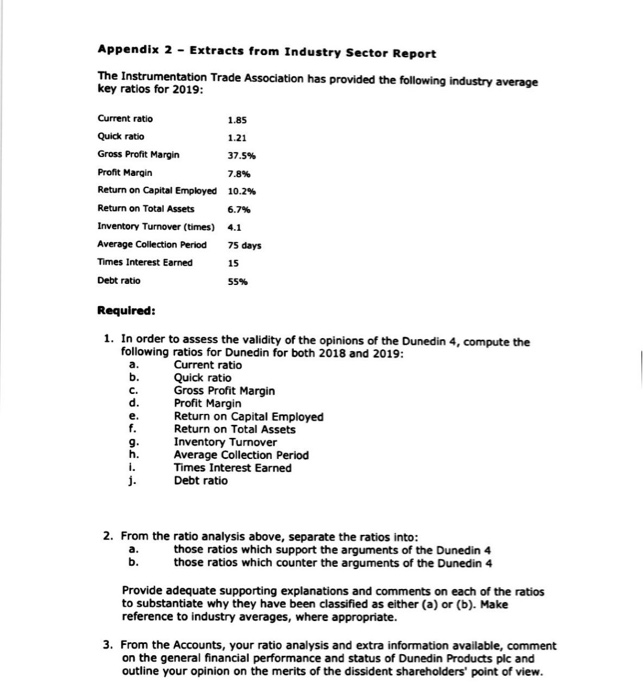

Case Study 1 This was the second meeting that the group of six had convened to discuss their investment in Dunedin Products plc. Each of them held shares in the company as a result of employments that had been terminated following disagreements with the company's founder and principal shareholder - Erwin O'Connor. Although they held only 4-5% each of the company's shares, their joint holding amounted to just over 25% - sufficient to cause a stir at the next annual general meeting. They had called themselves, the Dunedin 4; they were sure that other shareholders agreed with their view on the company's abysmal operating performance, but required a group around which to focus their dissatisfaction. "Look at these results,' exclaimed Sally Teviot, 'They're useless - when is this company ever going to be in a position to pay a dividend? "I'm really concerned,' said an exasperated Terry Goodyear. 'Erwin tricked me into paying a full price for my shares and I'll never get the money back now. "It's your own fault, Terry. He saw you coming,' retorted Sally. She had never been envious of Terry's commercial acumen. 'You can say that, Sally, but it's only your pride that's been folted by the way that Erwin fired you. You got your shares for next to nothing.' Terry was not prepared to let Sally's remark escape without some response. "Look, everyone. There's no point arguing with each other.' Paul Cox was always the reasonable voice. 'I think you'd all agree that none of us possesses the financial know-how to make much sense of the published accounts. We need some experienced help to assemble our case in a professional manner.' I agree, Paul.' Rosalind Carrot had been quiet till now. 'We'd all like to see a change at the company, but unless we present our case properly, nothing will happen. He's continuing to pay himself a higher and higher salary - and ignores the shareholders completely - we need to do something.' 'I know someone who could help,' chipped in Doug Gilchrist. "My daughter has just completed her MBA and she's spent a lot of time analysing companies results. She could review the 2019 Accounts for us.' "Could you ask her to do it sooner rather than later?' asked Paul, who was assuming the unwanted leadership role of this dissident group. I've got a summary of an industry sector report - that might be useful for her. Appendix 1 -Summary Accounts to December 2019, Dunedin Products plc Profit and Loss Account 2018 E000 2019 E000 7 856 5 700 6 375 Sales Cost of sales 4 212 Gross profit 2 156 2 163 Selling and distribution costs Administrative expenses (1 120) (1 000) (840) (935) Operating profit Interest Profit before taxation Taxation Profit for the year Balance Sheet E'000 2019 E'000 5 125 2018 E000 5 700 Fixed assets Current assets Inventories 2 543 1 750 2714 Debtors 3 784 6 327 Current liabilities Bank overdraft 587 110 Creditors 3852 3 420 4439 3 530 Net current assets 1 888 Total assets less Current liabilities 7013 6634 Creditors: Amounts due in excess of one year Loans 100 6 528 6 534 Capital and Reserves Ordinary share capital Profit and loss account 5 000 1 528 5 000 1 534 6 528 6 534 The following information is also available: 1. 2. 3. Depreciation during 2019 was 300 000. There were no gains or losses on the disposal of fixed assets during the year. Directors' remuneration increased from 250 000 in 2018 to 452 000 in 2019. The company has always had a good relationship with its bankers. Caledonia Bank. During 2019 the bank has supported the company with new loans and an increase in bank overdraft facilities. The company is heavily engaged in sales to export markets, many of which are carried out in US dollars. During 2019 the US dollar has weakened by 10% against Esterling. Appendix 2 - Extracts from Industry Sector Report The Instrumentation Trade Association has provided the following industry average key ratios for 2019: Current ratio Quick ratio Gross Profit Margin Profit Margin Return on Capital Employed Return on Total Assets Inventory Turnover (times) Average Collection Period Times Interest Earned Debt ratio 1.85 1.21 37.5% 7.8% 10.2% 6.7% 4.1 75 days 55% Required: b. 1. In order to assess the validity of the opinions of the Dunedin 4, compute the following ratios for Dunedin for both 2018 and 2019: a. Current ratio Quick ratio Gross Profit Margin Profit Margin Return on Capital Employed Return on Total Assets Inventory Turnover Average Collection Period Times Interest Earned Debt ratio 2. From the ratio analysis above, separate the ratios into: those ratios which support the arguments of the Dunedin 4 those ratios which counter the arguments of the Dunedin 4 Provide adequate supporting explanations and comments on each of the ratios to substantiate why they have been classified as either (a) or (b). Make reference to industry averages, where appropriate. 3. From the Accounts, your ratio analysis and extra information available, comment on the general financial performance and status of Dunedin Products plc and outline your opinion on the merits of the dissident shareholders' point of view