Case study and Background Porter (1979) argued that the essence of strategy formulation is coping with competition in the marketplace. He found that most business

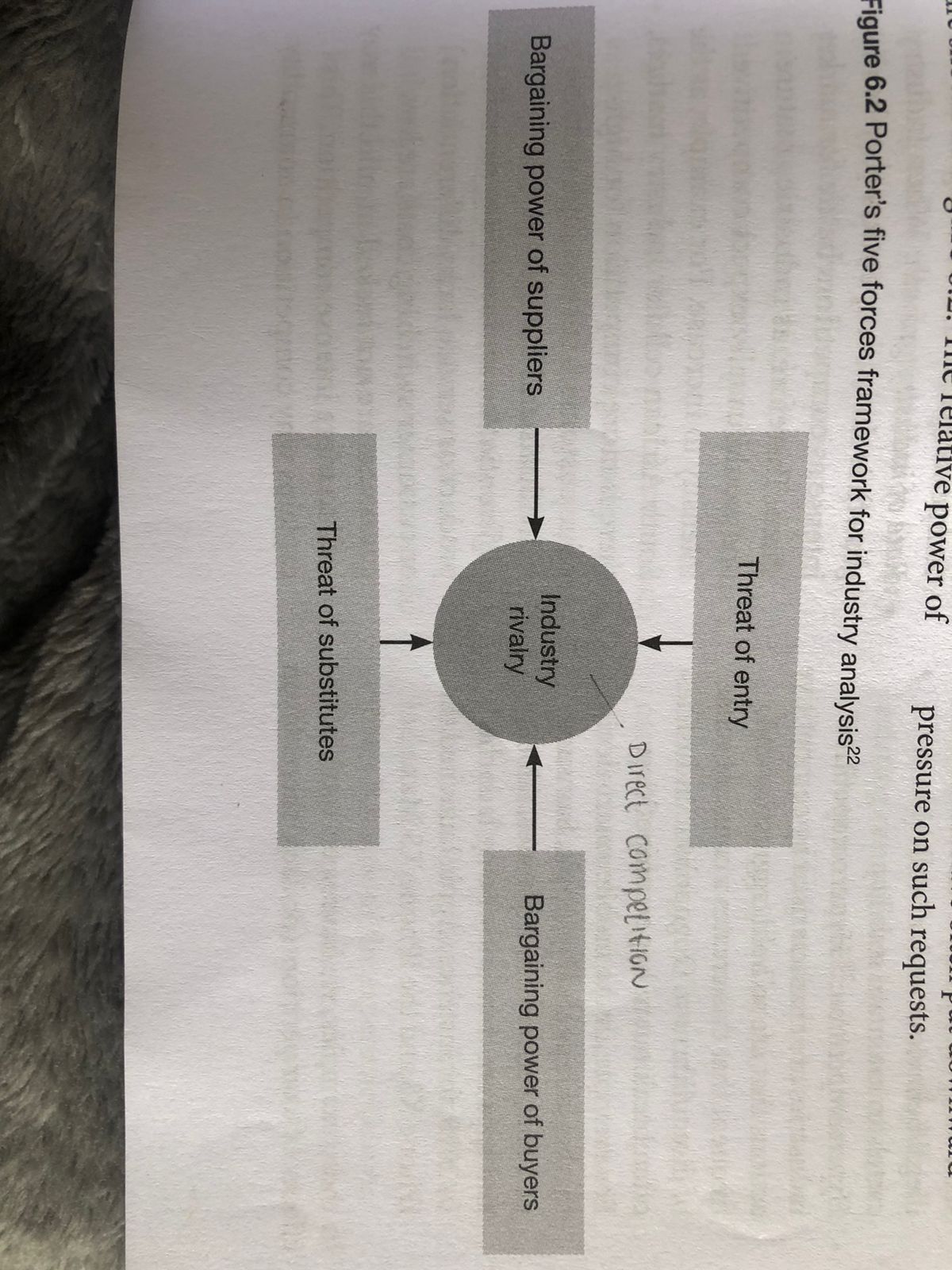

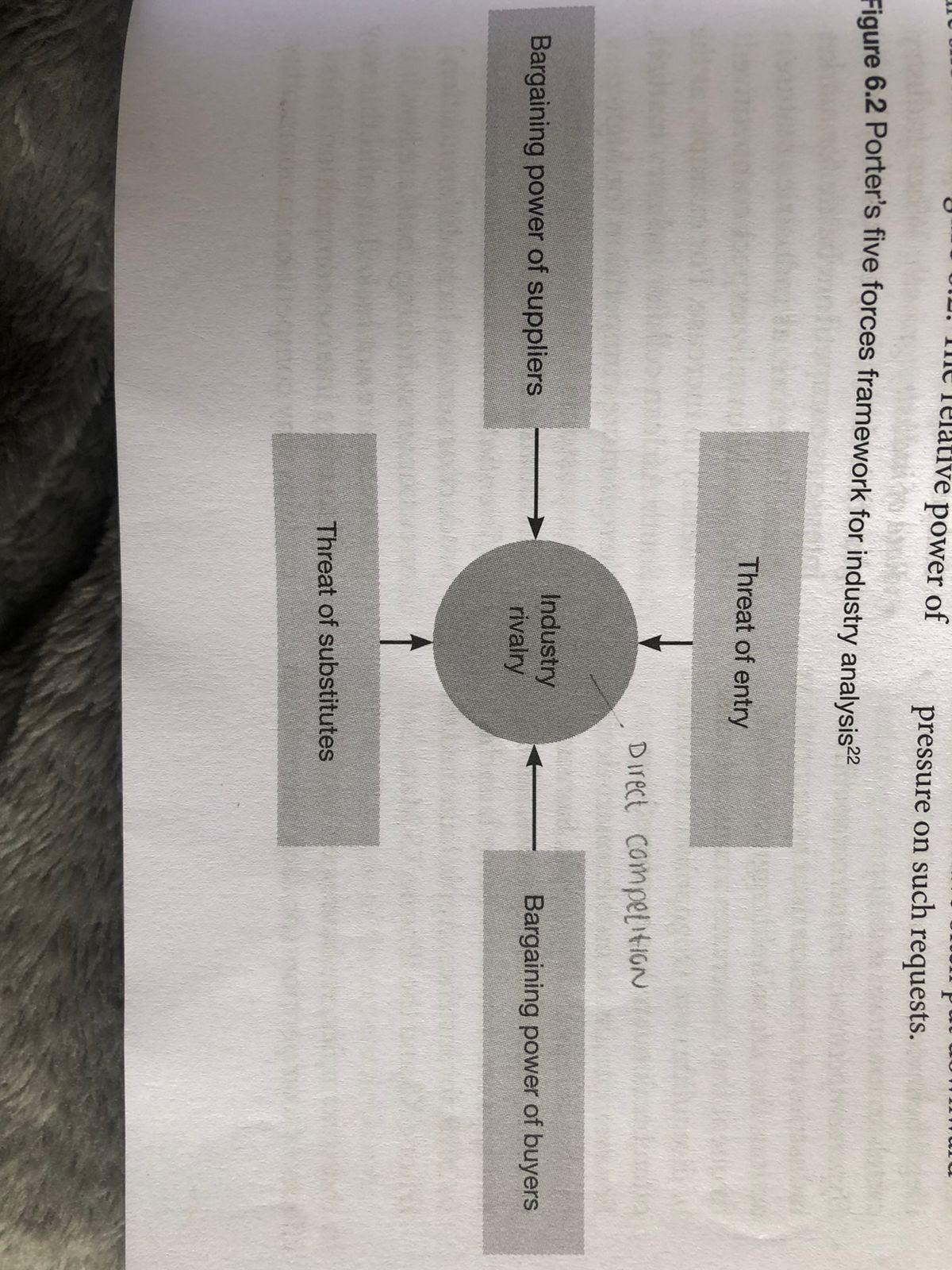

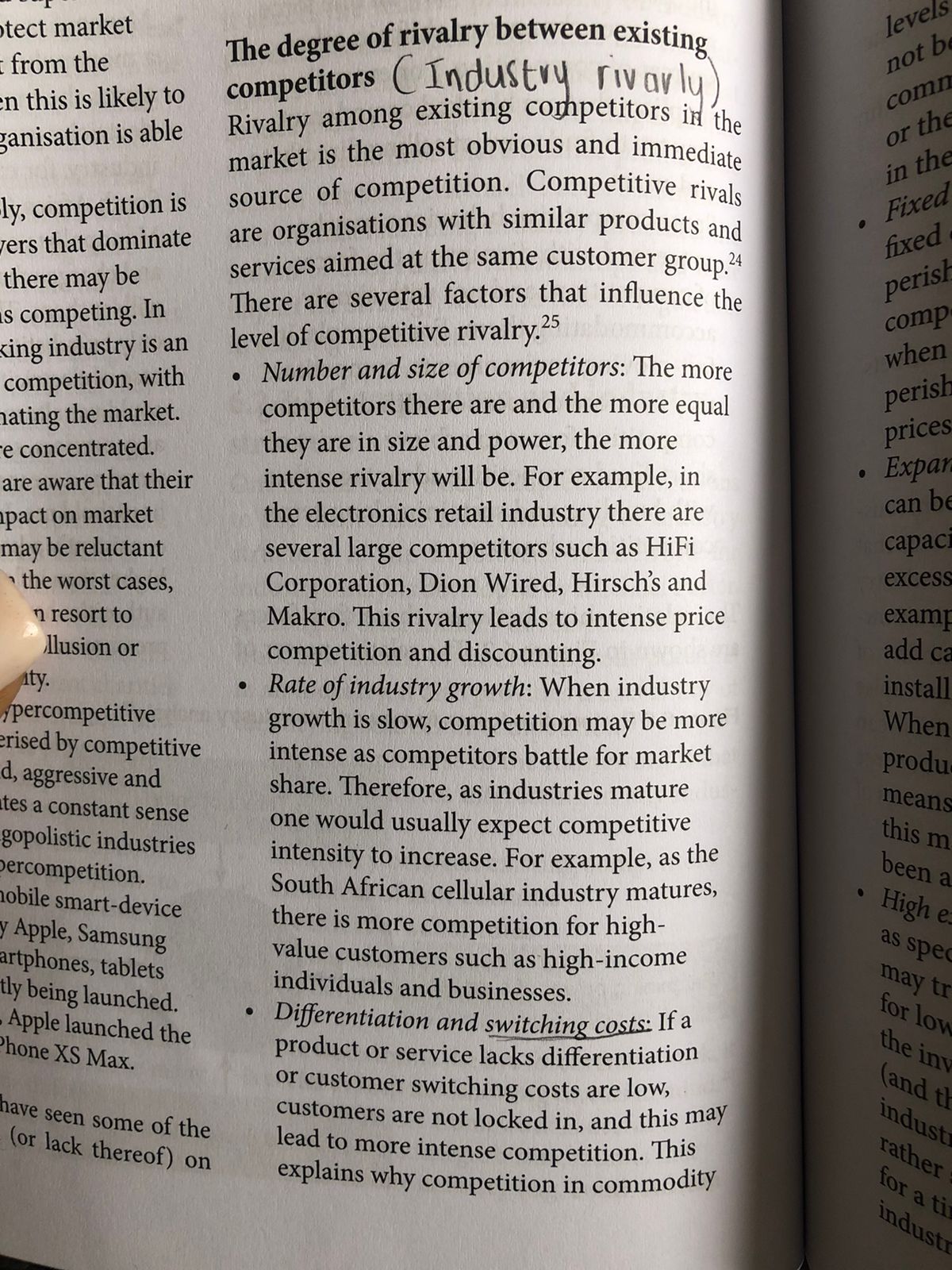

Case study and Background Porter (1979) argued that the essence of strategy formulation is coping with competition in the marketplace. He found that most business managers tended to view competition too narrowly and too pessimistically. Porter emphasised that while one would sometimes hear executives complaining to the contrary, intense competition in an industry is neither coincidence nor bad luck - moreover, in the fight for market share, competition is generally not manifested only in the other players, but rather, it is rooted in underlying economics, and competitive forces exist that go well beyond the established combatants in a particular industry. Source: Porter, M.E. 2008. The five competitive forces that shape strategy. Harvard Business Review, 86 (1): 78-93. "[I]n 2018, South Africa imported US$3.2 billion in processed foods, an increase of 5.5 percent from 2017, with the top five products being palm oil, food preparations, whiskies, beer made from malt, and animal guts, bladder and stomach parts. In the same year, the United States processed foods exports to South Africa, were valued at U.S. $111 million, and consisted of largely food preparations, whiskies, animal guts, bladder & stomach parts, sauces and mixed condiments, and nuts and seeds. Other products with good sales potential in South Africa include poultry meat, beer made from malt, organic products, oils, sardines prepared and preserved, dairy products, including dog and pet food." (Ntloedibe, 2019). "There are over 1,800 food production companies in South Africa. However, the top ten companies are responsible for more than 80 percent of the industry's production revenue. The industry employs 450,000 people in the subsectors of meat, fish, fruit, dairy products, grain mill products, and beverages. As a major producer and exporter of finished processed food products, South Africa's appetite for ingredients drives demand for a wide range of products inputs." (Ntloedibe, 2019). Source: Ntloedibe, M. 2019. South Africa: Food Processing Ingredients Report 2019. Global Agricultural Information Network, 28 March 2019. [Online]. Available at: https://gain.fas.usda.gov/Recent%20GAIN%20Publications/Food%20Processing%20Ingredients P retoria South%20Africa%20-%20Republic%20of 3-28-2019.pdf [Accessed 18 February 2022].21; 22; 23 2022 \"[W]e are a leading South African food manufacturer employing over 21 000 people, producing a wide range of branded and private label food products which we distribute through our own route- to-market supply chain specialist, Vector. Our strategy is founded on a clear sense of who we are and where we are going as a business. We aim to create the future lDur Way driven by Our Passion and Our Ambition and guided by Our Values. In our Passion to do "more", we are driven by a desire to improve people's access to nourishing food while achieving sustained business growth. The three \"mores\" of our Passion express our interlinked social and business agenda.\" (RCL Foods, 2021} Source: RCL Foods. 2021. Who we are. [Online]. Available at: httpszgrclfoodscom[our-businessgwho- weare [Accessed 13 February 2022]. (1.2.1 a} Conduct an industry analysis for the food industry in South Africa using the {25} Porter's Five Forces model. b} Provide application specific to RCL Foods to your industry analysis. (1.2.2 Critically examine the different industry key success factors for RCL foods by {10} applying the concept of "the three C's\". NB: There will be no marks allocated for just naming the three C's. e power of pressure on such requests. Figure 6.2 Porter's five forces framework for industry analysis22 Threat of entry Direct competition Industry Bargaining power of suppliers Bargaining power of buyers rivalry Threat of substitutestect market levels from the The degree of rivalry between existing not b n this is likely to competitors ( Industry rivarly ) comi ganisation is able Rivalry among existing competitors in the or the market is the most obvious and immediate in the ly, competition is source of competition. Competitive rivals ers that dominate are organisations with similar products and . Fixed fixed there may be services aimed at the same customer group. 24 is competing. In There are several factors that influence the perish comp xing industry is an level of competitive rivalry.25 competition, with . Number and size of competitors: The more when ating the market. competitors there are and the more equal perish e concentrated. they are in size and power, the more prices are aware that their intense rivalry will be. For example, in . Expar pact on market the electronics retail industry there are can be may be reluctant several large competitors such as HiFi capaci the worst cases, Corporation, Dion Wired, Hirsch's and excess n resort to Makro. This rivalry leads to intense price exam lusion or competition and discounting. add ca ity. . Rate of industry growth: When industry install percompetitive growth is slow, competition may be more When rised by competitive intense as competitors battle for market d, aggressive and produ share. Therefore, as industries mature tes a constant sense means one would usually expect competitive gopolistic industries this m ercompetition. intensity to increase. For example, as the been a obile smart-device South African cellular industry matures, . High e. y Apple, Samsung there is more competition for high- artphones, tablets value customers such as high-income as spec may tr tly being launched. individuals and businesses. Apple launched the . Differentiation and switching costs: If a for low Phone XS Max. product or service lacks differentiation the in or customer switching costs are low, (and th have seen some of the customers are not locked in, and this may indust (or lack thereof) on lead to more intense competition. This rather explains why competition in commodity for a ti industy competitors he first step she he industry and to determines markets is often intense. Short-term or services, viewpoint of the analysis - from whose insurance is an example of an industry as. Entry into spective is the analysis being conducted; where most competitive products are y, and there is doing that, each competitive force can be at similar and switching costs are relatively lysed using the factors driving competiti low (one phone call is often all that is g innovations. for example by rating them as high, medin required), leading to a high level of ins are low, competition. Aggregate service providers or numbers or low. The last step is then to conclude on " like Hippo (www.hippo.co.za) provide ces may be biggest competitive threats where they orig shoppers for short-term insurance with way to create nate from, and what the organisation can the necessary information from many perior about them. Each of the five forces will now be short-term insurance providers so that they can easily compare insurance quotes t market discussed in more depth (also see Figure 63) online. On the other hand, where certain m the The degree of rivalry between existing competitors have managed to create high is is likely to ation is able competitors ( Industry rivarly) levels of differentiation customers may Rivalry among existing competitors in the not be willing to switch because of their commitment to the brand or organisation, mpetition is market is the most obvious and immediate or they may be locked into contracts (e.g. at dominate source of competition. Competitive rivals in the cellular telephony industry). may be are organisations with similar products and Fixed costs or perishable products: Where eting. In services aimed at the same customer group." fixed costs are high or products are There are several factors that influence the perishable, there may be pressure on dustry is an level of competitive rivalry.25 competitors to cut costs. For example, ition, with . Number and size of competitors: The more when there is excess production of e market. competitors there are and the more equal perishable products such as milk or fruit, trated. they are in size and power, the more prices will drop to sell higher volumes. e that their intense rivalry will be. For example, in Expansion: Where production capacity market the electronics retail industry there are can be increased only in large chunks, luctant several large competitors such as HiFi capacity expansion may lead to temporary st cases, Corporation, Dion Wired, Hirsch's and excess capacity and price cutting. For it to Makro. This rivalry leads to intense price example, automotive producers can only n or competition and discounting. add capacity in relatively large chunks by Rate of industry growth: When industry installing a new production line or factory. titive growth is slow, competition may be more When such capacity additions are made, intense as competitors battle for market producers could use lower prices as a mpetitive share. Therefore, as industries mature means of generating higher volumes, in e and this manner using the capacity which has nt sense one would usually expect competitive been added. dustries intensity to increase. For example, as the . High exit barriers: Where exit barriers, such on. South African cellular industry matures, as specialised assets, are high, competitors device there is more competition for high- may try to compete for as long as possible sung value customers such as high-income for low or even negative returns. Given lets individuals and businesses. the investment that automotive producers ched. . Differentiation and switching costs: If a product or service lacks differentiation (and the government) have made in the ed the or customer switching costs are low, industry in South Africa, producers would customers are not locked in, and this may rather sell at a discount and lose money lead to more intense competition. This for a time than close down and exit the industry too soon. of the of) on explains why competition in commodityAnalysing the industry environment markets is often intense. Short-term insurance is an example of an industry . Diverse strategies: Where rivals are where most competitive products are diverse in strategies and origins, similar and switching costs are relatively "personality clashes' may occur as low (one phone call is often all that is they have different ideas about how to required), leading to a high level of compete and how the industry works. competition. Aggregate service providers For example, in the short-term insurance like Hippo (www.hippo.co.za) provide industry, OUTsurance, MiWay and other shoppers for short-term insurance with direct short-term insurers provide a the necessary information from many service that eliminates insurance brokers, whereas other organisations such as short-term insurance providers so that Mutual & Federal traditionally use they can easily compare insurance quotes brokers as their sales and service points online. On the other hand, where certain and believe that is in their best interest to competitors have managed to create high continue doing so. levels of differentiation customers may not be willing to switch because of their The threat of new entrants ( Threats new commitment to the brand or organisation, Whenever an industry becomes profitable, entry or they may be locked into contracts (e.g. there are incentives for other competitors to in the cellular telephony industry). enter the market. The success of their entry is Fixed costs or perishable products: Where dependent on the existing barriers to entry in fixed costs are high or products are an industry, of which there are several. 26 perishable, there may be pressure on Economies of scale: The economies of scale competitors to cut costs. For example, required to be successful can provide when there is excess production of a barrier to entry in some industries, perishable products such as milk or fruit, such as manufacturing capacity in the prices will drop to sell higher volumes. automotive industry. Expansion: Where production capacity Capital cost of entry: The capital cost can be increased only in large chunks, of entry into an industry can provide a capacity expansion may lead to temporary barrier to entry. This is especially true of excess capacity and price cutting. For capital-intensive industries such as gold example, automotive producers can only mining or electricity supply. add capacity in relatively large chunks by Control of distribution channels: Where installing a new production line or factory. existing competitors have control over When such capacity additions are made, distribution channels, whether through producers could use lower prices as a direct ownership or simply by virtue of means of generating higher volumes, in customer or supplier loyalty, this can this manner using the capacity which has provide a barrier to entry. been added. Good relationships: Where existing High exit barriers: Where exit barriers, such competitors have good relationships as specialised assets, are high, competitors with customers and suppliers, or where may try to compete for as long as possible customers and suppliers are locked for low or even negative returns. Given into relationships with competitors, for the investment that automotive producers example through contracts, new entrants (and the government) have made in the may find it difficult to break into the industry in South Africa, producers would industry. rather sell at a discount and lose money Time: Because of the experience curve, for a time than close down and exit the existing competitors that have been in industry too soon. the industry for longer may have cost orAnalysing the industry environment | 187 ustry power to exert downward pressure on the cost and stationery also does not affect the ection 6 prices of individual food producers (see quality of the furniture they produce. ars with Strategy in action The buying power of Information: The more information buyers ch as well large southern African supermarket chains have about suppliers' pricing structures itutes for is keeping small suppliers out on page 193). and input costs, the more powerful they Switching costs: The bargaining power of will be. bstitution buyers is high when the cost of switching mplements suppliers is low. This may include The bargaining power of suppliers e between situations where the product or service The relative bargaining power of suppliers roducts are is undifferentiated and generic, i.e. a determines the supplier opportunity cost. This rs have access commodity. affects input prices, and therefore the profita- Backward vertical integration: If there is bility, of competitors, as we can see from the when a new a threat of backward vertical integration Strategy in action case: The buying power of an existing the - in other words, the threat of a buyer large southern African supermarket chains is keeping small suppliers out (page 193). Similar same need acquiring the supplier or setting up their own sources of supply - then this will forces to those determining buyer power cameras fort increase the bargaining power of buyers. determine the bargaining power of suppliers: 30 his category Ratio of purchase price to total cost: Buyers, . Supplier concentration: The larger and when produc who themselves are often producers more concentrated suppliers are, the more posable or providers of services, will generally powerful they will be. Again, this power n consumers be less price sensitive, and as a result will be enhanced if there are many buyers. he during a less inclined to shop around, when the This is the case in the banking industry down or may purchase price of a product or service is where there are relatively few banks to ories of prodat a small fraction of their total production service many customers. (Also see the cost, and is not important to the quality of Case example AB InBev below.) their production. Buyers who are highly Switching costs: The bargaining power of profitable and interested in quality rather suppliers is high where the buyers' cost buyers than price are also less price sensitive. For of switching suppliers is high. This may ver of buyers Ice example, an organisation that produces include situations where products or on the prices furniture may be less sensitive to the price services are unique or so differentiated tors in an index of stationery, as it will only represent a that it would be difficult to develop re buyers are p small portion of their total production alternative sources of supply. affect the ability prices or tor CASE EXAMPLE: AB InBev erful buyers ......... e freedom to the In 2008, the Belgium-based brewer InBev acquired the American brewer, Anheuser- Busch, to become Anheuser-Busch InBev (AB InBev). In 2016, AB InBev acquired are determine SABMiller in a deal worth $103 billion (R1.4 trillion), sealing the union of the world's uyers.29 two biggest beer makers. The SABMiller name was dropped, but SAB still exists as an here there is ther me AB InBev subsidiary.31 As a dominant player in the South African beer market with key brands such as Castle and Black Label, and a distributor for Coca-cola through its soft- ul customers drink division Amalgamated Beverage Industries (ABI), AB InBev subsidiary SAB exerts uyers that pu a strong influence over the retailers of liquor and soft drinks. The manufacturer thus has much influence over the wholesale as well as the retail price of beer and soft drinks, and ay increase in-store merchandising strategies. This is a typical example of a situation where reduced ecially where suppliers buyer power means more profit to a supplier. DS SUCH188 | CHAPTER 6 . Forward vertical integration: The threat of . Porter's view is essentially one of the industry environment as a threat, and Man forward vertical integration could increase supplier bargaining power. This threat it focuses on those relationships that force fram exists when suppliers are not making reduce profits. It therefore largely ignores A sufficient profit margins, and could profit-enhancing relationships such as acquire their own channels or bypass cooperation. A P existing intermediaries to sell directly to It also mostly ignores the human elements value of strategy such as the role of management othe end-customers. For example, Apple and skills in strategy. your many other electronics and appliance sider manufacturers (such as LG and Samsung) . The framework seems to be predisposed fram have invested heavily in their own retail towards a top-down or prescriptive and spaces, which increases their bargaining approach to strategy - identifying com power with other retailers. opportunities and threats in the tors, Lack of substitutes: If there are no environment and formulating a response com substitutes available, this may increase to them. There is little room for emergent less supplier bargaining power. strategies. uct t Dependence on a single industry: There has never been consensus among For Sometimes the fortunes of suppliers may researchers on the effect of the industry on ple C be closely tied to a single industry or even organisational performance. devic a single customer (such as a coalmine Economists have questioned its theoretical smar being dependent on a single power foundation. It is based on the structure- incre station). For example, the manufacturers conduct-performance approach to pay of car seats are dependent on the industrial organisations, which has largely we ca automotive industry. In this case, this will been displaced by game theory. and reduce suppliers' bargaining power. relati Up to this point we have focused mostly on Us Despite the widespread acceptance and use- those relationships that reduce profits. The that c fulness of the five forces framework for indus- value net, however, emphasises complemen partn try analysis, it has not gone without criticism, tary relationships that enhance profitability. ship and it has several limitations:32 both . It is a static framework, viewing industries 6.2.3.2 Complementary with as stable and shaped by external forces. In relationships - the value net ity, th many industries today, the reality is that While the five forces framework focuses on to the industry structure and boundaries are constantly changing. substitutes as a competitive relationship, organ It assumes that organisations are economic theory also identifies comple- of the ments as a relationship.33 This relationship below essentially selfish and will always put their own interests first. This is not true of not- is not addressed by the five forces frame- Co for-profit and public-sector organisations. work. However, Brandenburger and Nalebuff Also, with the increasing focus on emphasised the importanc ortance of complementary mo sustainability, this perspective may be relationships in their value net concept. The somewhat outdated. value net concept examined similar constructs rel . While the framework approaches the to Porter's five forces framework, but also five forces as equal, this may not be true, focused on value-enhancing (complementary) especially for customers. There are many rather than value-destroying relationships observers who suggest that customers are (such as bargaining power). 34 Complementary may relationships are profit-enhancing because gan the most important component to any aspect of strategy. they increase the maximum price that custom- ers are willing to pay for a product or service

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance