Question: Case Study Total Acquisition Costing at Green Pump Company Inc. Please read the case study pack and address the following questions: From the interview transcripts

Case Study

Total Acquisition Costing at

Green Pump Company Inc.

Please read the case study pack and address the following questions:

- From the interview transcripts provided produce a model which represents the total known acquisition cost incurred by the Green Pump Company for the purchase of castings.

- For each element of the total acquisition cost model generated in 1 above, identify the potential cost drivers.

- What conclusions can be drawn from the results, and what initiatives could be undertaken to reduce the total cost.

Total Acquisition Costing

Quality Manager interview

| Qu.

| What sort of quality control do you use on the castings that the Green Pump Company purchases? |

| Ans.

| There is a check on all incoming batches of castings using a standard sampling plan based on British Standards. If a batch is rejected these are then 100% inspected, which will take an additional amount of time then either the batch is returned to the supplier or a concession is raised. |

| Qu.

| Are any quality assurance audit visits done on our casting suppliers? |

| Ans.

| I have recently appointed a supplier quality assurance engineer who has taken responsibility for this, but as yet he has done no work with our casting suppliers. |

| Qu.

| How effective are the sample inspections? Do they identify most of the defective casting supplies? |

| Ans.

| They are very effective, one in three batches is rejected by incoming goods inspection for some sort of defect. Most of these have a concession raised on them, but about a quarter of these are returned to the supplier. The cost of any transport, etc. is recharged to the supplier, but the administration of this is very time consuming. The Quality Department fills in a form detailing the problem and a copy of this is sent to the supplier and to our finance and purchasing departments and is also a major cause of invoicing and payment problems with our suppliers. Not every defect can be easily identified however; because of the time required only a small number of samples can be checked on the co-ordinate measuring machine and although there should be a check for porosity, I have not been able to purchase the necessary equipment to check this. This is a problem since porosity is one of the commonest defects on castings. |

| Qu.

| How much time does this represent for your inspectors? |

| Ans.

| I have five inspectors who spend all their time on castings and two additional ones who help them for around 50% of their time. |

Machine Shop Supervisor

| Qu.

| Can you explain how the machine shop is affected by some of the quality problems with castings? |

| Ans.

| The most important is porosity in the casting. There are normally no visible signs that a batch of castings is porous, so it is impossible to pick this up before we start machining the batch. If it is discovered then it is often after a significant amount of machining has already been completed. We then reject the batch and send them back to the supplier, but he will only reimburse us for the material cost and any machining time we have wasted on the casting cannot be reclaimed. This has been particularly difficult with impeller machining because this machine is already a bottle-neck and any time lost is very difficult to recover. It has even been necessary in the past to carry on machining a porous batch and then to reject those which were totally unacceptable because there was no time to get another batch from our supplier and the job was needed so urgently. |

| Qu.

| How much does it cost to scrap these castings in lost machining time? |

| Ans.

| It is almost impossible to value the time and aggravation it causes but we know from our recording system that we get 3.7% scrap due to porosity and the average cost of machining on most of our castings is around $254.50 |

Purchasing Manager

| Qu.

| What is the procedure followed for purchasing castings within the Green Pump Company? |

| Ans.

| Casting suppliers are normally determined when a new product is being designed. The drawings and specifications are sent to a number of suppliers with a request for quotation. When the responses are received, we normally select the supplier with the lowest cost? |

| Qu.

| Does this mean that there is normally only one supplier per part number? |

| Ans.

| No, because of the unreliability of most of our suppliers, we try to have at least two suppliers for each part number. This has been possible with most of our agricultural components, but with the volumes of some of our industrial pumps this has not been possible and there is only one supplier. |

| Qu.

| Do you need to maintain high stocks to overcome the reliability of these suppliers? |

| Ans.

| In order to ensure that there are always enough castings on hand we try to maintain at least one months stock, which means that on average there is at least three months stock of raw castings in the factory. |

| Qu.

| Do you know what the cost of storing this stock is? |

| Ans.

| The way we calculate this is to allow 25% of the value of stock as the cost of holding it (per year). |

| Qu.

| Does this mean that a lot of redundant stock is held due to parts becoming redundant? |

| Ans.

| Some of our casting stock does become obsolete. In the last year we had to scrap $64,500 of castings that were no longer of any value. There is still some stock that is not of much value that was kept as it still has some value for service parts, although it is not part of our normal production. |

| Qu.

| What transport cost is there to have your castings delivered? |

| Ans. | Nearly all our castings are collected by one of the companys own dedicated vehicles. The cost allocation from the companys transport budget is $103,312. Two of our suppliers, Northern Castings and Quality Castings Limited, are on delivered terms however; on those we pay carriage costs additional to the price of the castings. The estimated carriage costs are roughly 7% of product price. |

| Qu.

| What do you do about re-negotiating prices with suppliers? |

| Arts.

| Normally, if the increase seems reasonable, it will be accepted, although of course we will try to negotiate down the size of the increase. I have an overall objective for the cost of direct purchases however and I have to make sure that the total change in purchased cost enables us to achieve this. This means that with each supplier two to three days needs to be spent re-negotiating contracts and preparing for these meetings. |

| Qu.

| Is there much expediting of casting orders? |

| Ans.

| Yes, as I explained earlier, our casting suppliers are some of the most unreliable and the buyers in the department need to spend a large amount of their time expediting their orders. |

| Qu.

| How much time is spent in this activity? |

| Ans. | I have two buyers who are primarily concerned with castings. They spend 85% of their time on castings. Their time is spent placing the original orders and then chasing these orders. This is particularly important in castings as there is a greater amount of variety than other components and so it is more difficult to have the right parts in stock. They are not normally as involved with the negotiation of contracts which I or my deputy tend to handle. |

- Green Pump Company

- Total Acquisition Costing

- Basic Company Data

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

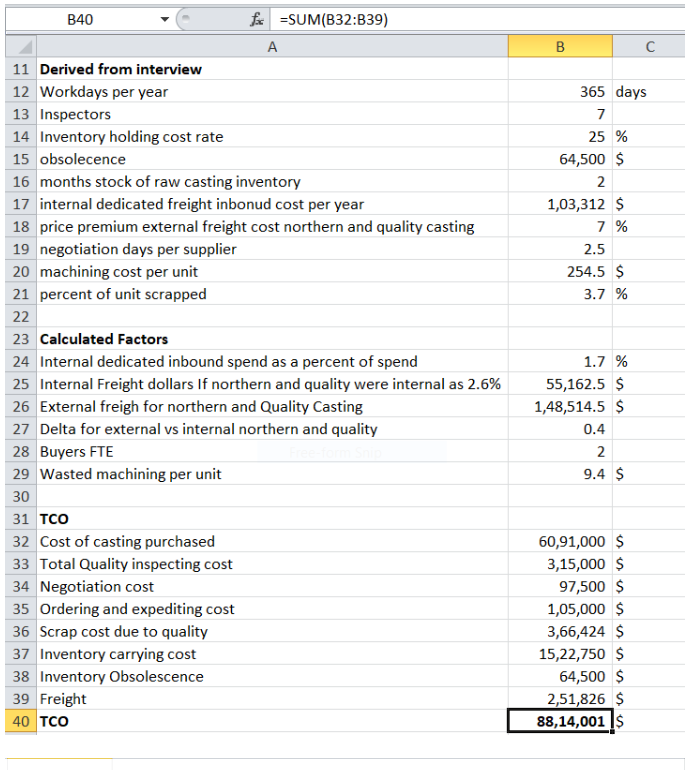

explain in detail the calculation that came up with the following numbers on the spreadsheet

\begin{tabular}{|c|c|c|c|} \hline & fx=SUM(B32:B39) & & \\ \hline 4 & A & B & C \\ \hline 11 & Derived from interview & & \\ \hline 12 & Workdays per year & 365 & days \\ \hline 13 & Inspectors & 7 & \\ \hline 14 & Inventory holding cost rate & 25 & % \\ \hline 15 & obsolecence & 64,500 & $ \\ \hline 16 & months stock of raw casting inventory & 2 & \\ \hline 17 & internal dedicated freight inbonud cost per year & 1,03,312 & $ \\ \hline 18 & price premium external freight cost northern and quality casting & 7 & % \\ \hline 19 & negotiation days per supplier & 2.5 & \\ \hline 20 & machining cost per unit & 254.5 & $ \\ \hline 21 & percent of unit scrapped & 3.7 & % \\ \hline \multicolumn{4}{|l|}{22} \\ \hline 23 & Calculated Factors & & \\ \hline 24 & Internal dedicated inbound spend as a percent of spend & 1.7 & % \\ \hline 25 & Internal Freight dollars If northern and quality were internal as 2.6% & 55,162.5 & $ \\ \hline 26 & External freigh for northern and Quality Casting & 1,48,514.5 & $ \\ \hline 27 & Delta for external vs internal northern and quality & 0.4 & \\ \hline 28 & Buyers FTE & 2 & \\ \hline 29 & Wasted machining per unit & 9.4 & $ \\ \hline \multicolumn{4}{|l|}{30} \\ \hline 31 & TCO & & \\ \hline 32 & Cost of casting purchased & 60,91,000 & $ \\ \hline 33 & Total Quality inspecting cost & 3,15,000 & $ \\ \hline 34 & Negotiation cost & 97,500 & $ \\ \hline 35 & Ordering and expediting cost & 1,05,000 & $ \\ \hline 36 & Scrap cost due to quality & 3,66,424 & $ \\ \hline 37 & Inventory carrying cost & 15,22,750 & $ \\ \hline 38 & Inventory Obsolescence & 64,500 & $ \\ \hline 39 & Freight & 2,51,826 & $ \\ \hline 40 & TCO & 88,14,001 & 7$ \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts