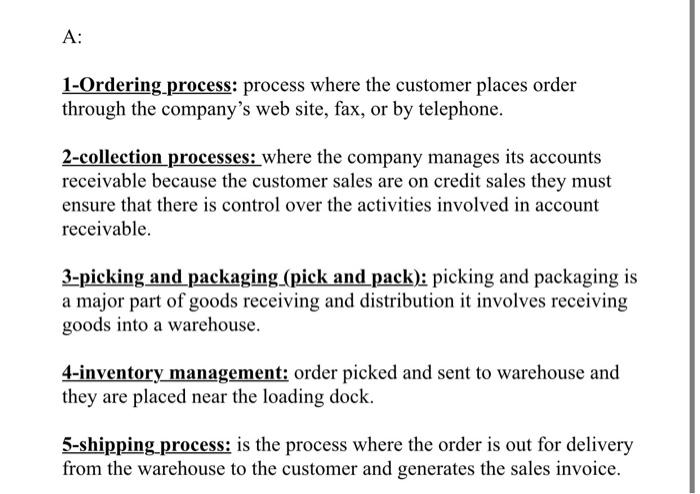

Case Study-1 Al Mustafa Corporation is a midsized, privately owned industrial instrument manufacturer supplying precision equipment to manufacturers in the Midwest. The administrative offices are located in a downtown building, and the production, shipping, and receiving departments are housed in a renovated warehouse a few blocks away. The corporation is 10 years old and performs its revenue cycle activities using its integrated ERP system as follows: Customers place orders on the company's Web site, by fax, or by telephone. All sales are on credit, FOB destination. During the past year, sales have increased dramatically, but 15% of credit sales have had to written off as uncollectible, including several large online orders to first-time customers who denied ordering or receiving the merchandise. Customer orders are picked and sent to the warehouse, where they are placed near the loading dock in alphabetical sequence by customer name. The loading dock is used both for outgoing shipments to customers and for receipt of incoming deliveries. There are 10 to 20 incoming deliveries every day, from a variety of sources. The increased volume of sales has resulted in a number of errors in which customers were sent the wrong items. There have also been some delays in shipping because items that supposedly were in stock could not be found in the warehouse. Although a perpetual inventory is maintained, there has been no physical count of inventory for two years. When an item is missing, the warehouse staff writes the information down in a log book. Once a week, the warehouse staff uses the log book to update the inventory records. The system is configured to prepare the sales invoice only after shipping employees enter the actual quantities sent to a customer, thereby ensuring that customers are billed only for items actually sent and not for anything on back order. A: 1-Ordering process: process where the customer places order through the company's web site, fax, or by telephone. 2-collection processes: where the company manages its accounts receivable because the customer sales are on credit sales they must ensure that there is control over the activities involved in account receivable. 3-picking and packaging.(pick and pack): picking and packaging is a major part of goods receiving and distribution it involves receiving goods into a warehouse. 4-inventory management: order picked and sent to warehouse and they are placed near the loading dock. 5-shipping process: is the process where the order is out for delivery from the warehouse to the customer and generates the sales invoice. b. Identify five risks associated with the five activities identified on a. (5 points)