Question

CB Solutions. Heather O'Reilly, the treasurer of CB Solutions, believes interest rates are going to rise, so she wants to swap her future floating-rate interest

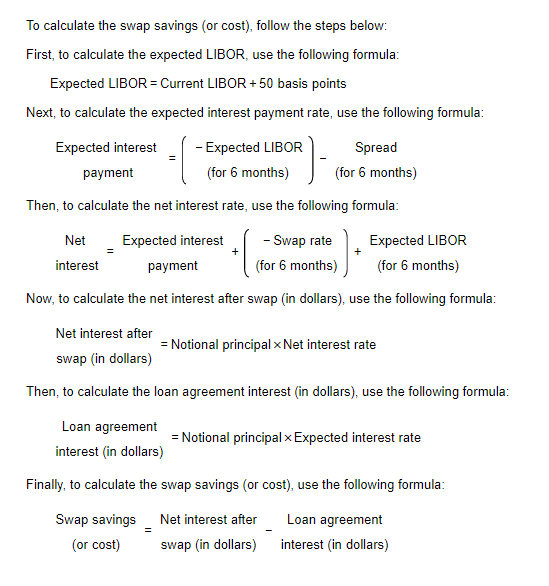

CB Solutions. Heather O'Reilly, the treasurer of CB Solutions, believes interest rates are going to rise, so she wants to swap her future floating-rate interest payments for fixed rates. Presently, she is paying per annum on $5,100,000 of debt for the next two years, with payments due semiannually. LIBOR is currently 3.992% per annum. Spread paid over LIBOR, per annum is 2.000%. Heather has just made an interest payment today, so the next payment is due six months from now. Heather finds that she can swap her current floating-rate payments for fixed payments of 7.008% per annum. (CB Solutions' weighted average cost of capital is 12%, which Heather calculates to be 6% per 6-month period, compounded semiannually).

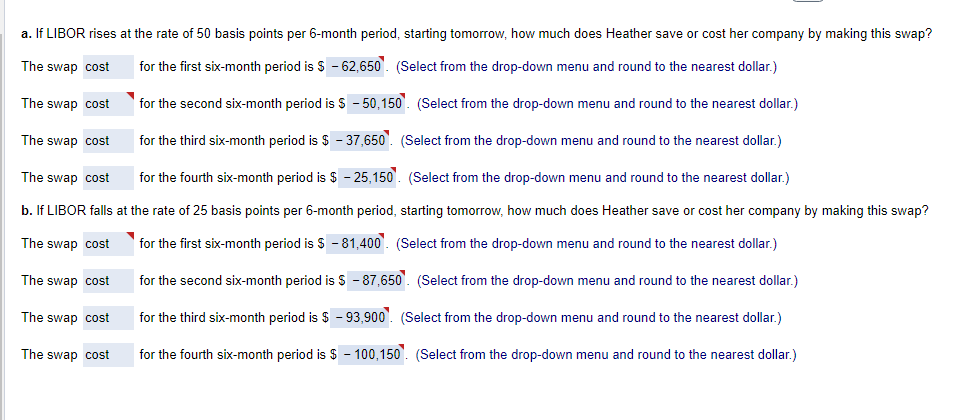

a. If LIBOR rises at the rate of 50 basis points per 6-month period, starting tomorrow, how much does Heather save or cost her company by making this swap?

b. If LIBOR falls at the rate of 25 basis points per 6-month period, starting tomorrow, how much does Heather save or cost her company by making this swap?

ANSWER EACH QUESTION

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Forex Trading Manual The Rules Based Approach To Making Money Trading Currencies

Authors: Javier H. Paz

1st Edition

0071782923,0071782931