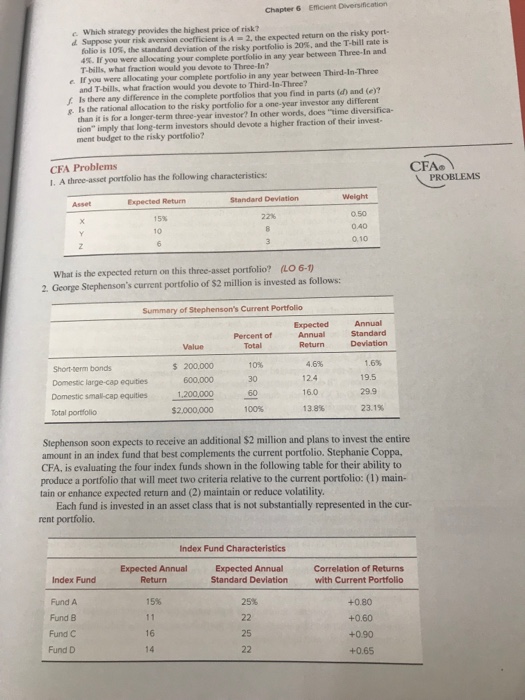

Cfa problem

Chapter 6 Efficient e. Which strategy provides the highest price of risk? d Suppose your risk aversion coefficient is A 2, the expected return on the risky port folio is 10%, the standard deviation of the risky portfolio is 20%, and te Thill at 4%. If you were allocating your complete portfolio in any year between Three-In and T-bills, what fraction would you devote to Three-In? e. If you were allocating your complete portfolio in any year between Third-In-Three and T-bills, what fraction would you devote to Third-In-Three? . Is there any difference in the complete portfolios that you find in parts (d) and (e)? g Is the rational allocation to the risky portfolio for a one-year investor any different than it is for a longer-term three-year investor? In other words, does "time diversifica- tion" imply that long-term investors should devote a higher fraction of their invest- ment budget to the risky portfolio? CFA CFA Problems I. A three-asset portfolio has the following characteristics: PROBLEMS Weight 0.50 0.40 0.10 Expected Return Standard Deviation 22% 10 What is the expected return on this three-asset portfolio? (LO 6-1) 2. George Stephenson's current portfolio of $2 million is invested as follows Summary of Stephenson's Current Portfolio Standard Deviation 1.6% 19.5 29.9 23.1% Percent of Short-term bonds Domestic large-cap equities Domestic smal-cap equities Total portfolio $ 200,000 600,000 1,200,000 $2,000,000 Return 46% 2.4 16.0 13.8% 30 60 100% soon expects to receive an additional $2 million and plans to invest the entire Stephenson amount in an index fund that best complements the current portfolio. Stephanie Coppa, CFA, is evaluating the four index funds shown in the following table for their ability to produce a portfolio that will meet two criteria relative to the current portfolio: (1) main- tain or enhance expected return and (2) maintain or reduce volatility Each fund is invested in an asset class that is not substantially represented in the cur- rent portfolio. Index Fund Characteristics Expected AnnualExpected Annual Correlation of Returns Standard Deviation with Current Portfolio +0.80 +0.60 +0.90 +0.65 Return Index Fund Fund A Fund B Fund C Fund D 15% 25% 16 25 14 Chapter 6 Efficient e. Which strategy provides the highest price of risk? d Suppose your risk aversion coefficient is A 2, the expected return on the risky port folio is 10%, the standard deviation of the risky portfolio is 20%, and te Thill at 4%. If you were allocating your complete portfolio in any year between Three-In and T-bills, what fraction would you devote to Three-In? e. If you were allocating your complete portfolio in any year between Third-In-Three and T-bills, what fraction would you devote to Third-In-Three? . Is there any difference in the complete portfolios that you find in parts (d) and (e)? g Is the rational allocation to the risky portfolio for a one-year investor any different than it is for a longer-term three-year investor? In other words, does "time diversifica- tion" imply that long-term investors should devote a higher fraction of their invest- ment budget to the risky portfolio? CFA CFA Problems I. A three-asset portfolio has the following characteristics: PROBLEMS Weight 0.50 0.40 0.10 Expected Return Standard Deviation 22% 10 What is the expected return on this three-asset portfolio? (LO 6-1) 2. George Stephenson's current portfolio of $2 million is invested as follows Summary of Stephenson's Current Portfolio Standard Deviation 1.6% 19.5 29.9 23.1% Percent of Short-term bonds Domestic large-cap equities Domestic smal-cap equities Total portfolio $ 200,000 600,000 1,200,000 $2,000,000 Return 46% 2.4 16.0 13.8% 30 60 100% soon expects to receive an additional $2 million and plans to invest the entire Stephenson amount in an index fund that best complements the current portfolio. Stephanie Coppa, CFA, is evaluating the four index funds shown in the following table for their ability to produce a portfolio that will meet two criteria relative to the current portfolio: (1) main- tain or enhance expected return and (2) maintain or reduce volatility Each fund is invested in an asset class that is not substantially represented in the cur- rent portfolio. Index Fund Characteristics Expected AnnualExpected Annual Correlation of Returns Standard Deviation with Current Portfolio +0.80 +0.60 +0.90 +0.65 Return Index Fund Fund A Fund B Fund C Fund D 15% 25% 16 25 14