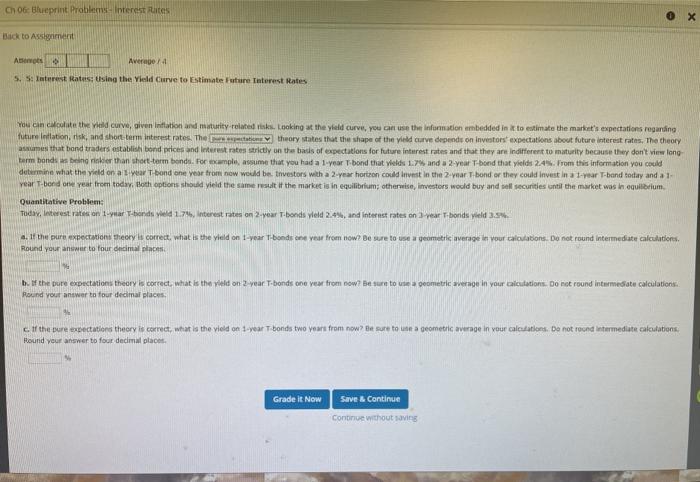

Ch 06: Blueprint Problems interest Rites Back to Assignment Abemos OLD Average 4 5. Sinterest Rates using the Yield Curve to estimate Future Teterest Rates You can be the Wildcurve, given inflation and maturity related risks. Looking at the yield Curve, you can use the information embedded in to estimate the market's expectations regarding future Intation, fisk, and short-term interest rates. The theory states that the shape of the yield curve depends on investors expectations about future interest rates. The theory aames that bond traders establishi bond prices and Interest rates strictly on the basis of expectations for future interest rates and that they are indifferent to maturity because they don't viw long armbands as being in than short-term bonds. For example, assume that you had a 1-year T-bond that yields 1.7% and 2-year T-bond that yields 245. From this information you could determine what the yield on a wabond one year from now would be tnvestors with a 2-year hortron could invest in the 2-year bond or they could invest in tear T-band today and a 1: Year T-bond one year from today. Both options should vield the same result if the market is in equilibrium; otherwise, investors would buy and sell securities until the market was in equilibrium Quantitative Problem: Today, Interest rates on lar T-bondsid 1.75, interest rates on 2.voar t.bonds yield 2.4% and interest rates on year T-bonds Vield 3.59 a. In the pura expectations theory is correct, what is the held on 1-year T-bonds one year from now? Be sure to use a geometrie average levour calculations. Do not found intermediate calculations, Round your answer to four decimal places b. If the pure expectations theory is correct, what is the yield on 2-year T-bonds one year from now Be sure to geometric average in your calculations. Do not found intermediate calculations. Round your answer to four decimal places cIf the pure expectations theory is correct, what is the vied on 1 year bonds two years from now? be sure to use a peometric average in your calculations. Do not round intermediate cakculations Round your answer to four decimal places Grade it Now Save & Continue Continue without saving Ch 06: Blueprint Problems interest Rites Back to Assignment Abemos OLD Average 4 5. Sinterest Rates using the Yield Curve to estimate Future Teterest Rates You can be the Wildcurve, given inflation and maturity related risks. Looking at the yield Curve, you can use the information embedded in to estimate the market's expectations regarding future Intation, fisk, and short-term interest rates. The theory states that the shape of the yield curve depends on investors expectations about future interest rates. The theory aames that bond traders establishi bond prices and Interest rates strictly on the basis of expectations for future interest rates and that they are indifferent to maturity because they don't viw long armbands as being in than short-term bonds. For example, assume that you had a 1-year T-bond that yields 1.7% and 2-year T-bond that yields 245. From this information you could determine what the yield on a wabond one year from now would be tnvestors with a 2-year hortron could invest in the 2-year bond or they could invest in tear T-band today and a 1: Year T-bond one year from today. Both options should vield the same result if the market is in equilibrium; otherwise, investors would buy and sell securities until the market was in equilibrium Quantitative Problem: Today, Interest rates on lar T-bondsid 1.75, interest rates on 2.voar t.bonds yield 2.4% and interest rates on year T-bonds Vield 3.59 a. In the pura expectations theory is correct, what is the held on 1-year T-bonds one year from now? Be sure to use a geometrie average levour calculations. Do not found intermediate calculations, Round your answer to four decimal places b. If the pure expectations theory is correct, what is the yield on 2-year T-bonds one year from now Be sure to geometric average in your calculations. Do not found intermediate calculations. Round your answer to four decimal places cIf the pure expectations theory is correct, what is the vied on 1 year bonds two years from now? be sure to use a peometric average in your calculations. Do not round intermediate cakculations Round your answer to four decimal places Grade it Now Save & Continue Continue without saving