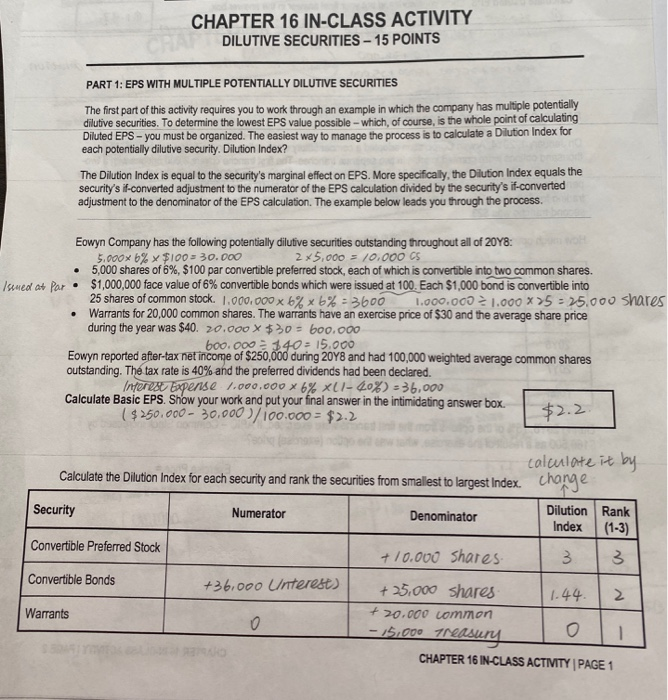

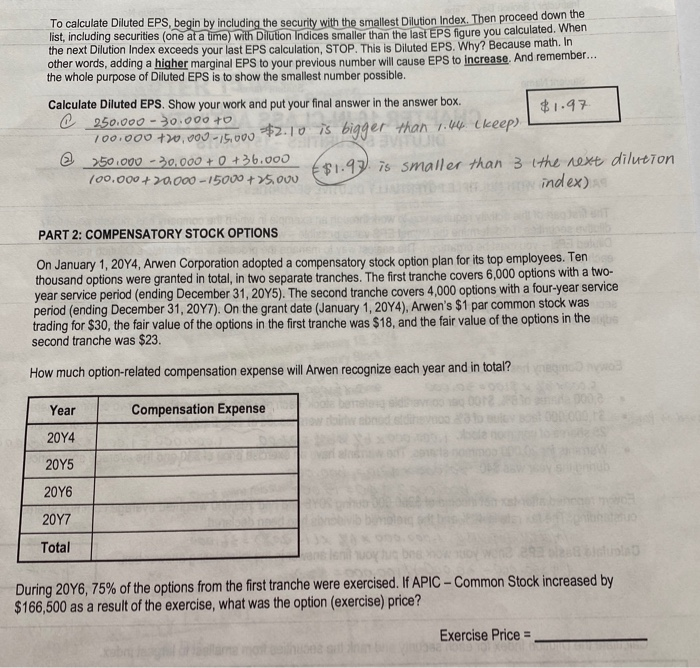

CHAPTER 16 IN-CLASS ACTIVITY DILUTIVE SECURITIES - 15 POINTS PART 1: EPS WITH MULTIPLE POTENTIALLY DILUTIVE SECURITIES The first part of this activity requires you to work through an example in which the company has multiple potentially dilutive securities. To determine the lowest EPS value possible - which, of course, is the whole point of calculating Diluted EPS - you must be organized. The easiest way to manage the process is to calculate a Dilution Index for each potentially dilutive security. Dilution Index? The Dilution Index is equal to the security's marginal effect on EPS. More specifically, the Dilution Index equals the security's if-converted adjustment to the numerator of the EPS calculation divided by the security's if-converted adjustment to the denominator of the EPS calculation. The example below leads you through the process. Eowyn Company has the following potentially dilutive securities outstanding throughout all of 2048: 5.000x 6% x $100 - 30.000 2x5.000 - 10.000 CS 5,000 shares of 6%, $100 par convertible preferred stock, each of which is convertible into two common shares. Isted at Par $1,000,000 face value of 6% convertible bonds which were issued at 100. Each $1,000 bond is convertible into 25 shares of common stock. 1.000.000 x 6% x 6% - 3600 1.000.000 1.000 x 75 = 25.000 shares Warrants for 20,000 common shares. The warrants have an exercise price of $30 and the average share price during the year was $40. 20.000 x $30 - boo.000 boo.000 140: 15.000 Eowyn reported after-tax net income of $250,000 during 2048 and had 100,000 weighted average common shares outstanding. The tax rate is 40% and the preferred dividends had been declared. Interest Expense 1.000.000 x 6% XII-20%) = 36,000 Calculate Basic EPS. Show your work and put your final answer in the intimidating answer box ($250.000 - 30,000)/100.000 = $2.2 $2.2 (1-3) calculate it by Calculate the Dilution Index for each security and rank the securities from smallest to largest Index change Security Numerator Dilution Rank Denominator Index Convertible Preferred Stock +10.000 shares 3 3 Convertible Bonds +36.000 Unterest) + 25.000 shares 1.44 2 Warrants 20.000 common 0 - 15,000 Treasury o 1 CHAPTER 16 IN-CLASS ACTIVITY | PAGE 1 + To calculate Diluted EPS, begin by including the security with the smallest Dilution Index. Then proceed down the list, including securities (one at a time with Dilution Indices smaller than the last EPS figure you calculated. When the next Dilution Index exceeds your last EPS calculation, STOP. This is Diluted EPS. Why? Because math. In other words, adding a higher marginal EPS to your previous number will cause EPS to increase. And remember... the whole purpose of Diluted EPS is to show the smallest number possible. Calculate Diluted EPS. Show your work and put your final answer in the answer box $1.97 250.000 - 30.000 +0 100.000 +70,000 -15.000 $2.10 is bigger than 1.44 ekeep) @ 250.000 - 20.000 + 0 + 36.000 $1.99) is smaller than 3 (the next dilution 100.000 + 70.000-15000 +75.000 index) PART 2: COMPENSATORY STOCK OPTIONS On January 1, 2014, Arwen Corporation adopted a compensatory stock option plan for its top employees. Ten thousand options were granted in total, in two separate tranches. The first tranche covers 6,000 options with a two- year service period (ending December 31, 20Y5). The second tranche covers 4,000 options with a four-year service period (ending December 31, 20Y7). On the grant date (January 1, 20Y4), Arwen's $1 par common stock was trading for $30, the fair value of the options in the first tranche was $18, and the fair value of the options in the second tranche was $23. How much option-related compensation expense will Arwen recognize each year and in total? 02 Year Compensation Expense 20Y4 2045 20Y6 2047 Total During 20Y6, 75% of the options from the first tranche were exercised. If APIC - Common Stock increased by $166,500 as a result of the exercise, what was the option (exercise) price? Exercise Price = CHAPTER 16 IN-CLASS ACTIVITY DILUTIVE SECURITIES - 15 POINTS PART 1: EPS WITH MULTIPLE POTENTIALLY DILUTIVE SECURITIES The first part of this activity requires you to work through an example in which the company has multiple potentially dilutive securities. To determine the lowest EPS value possible - which, of course, is the whole point of calculating Diluted EPS - you must be organized. The easiest way to manage the process is to calculate a Dilution Index for each potentially dilutive security. Dilution Index? The Dilution Index is equal to the security's marginal effect on EPS. More specifically, the Dilution Index equals the security's if-converted adjustment to the numerator of the EPS calculation divided by the security's if-converted adjustment to the denominator of the EPS calculation. The example below leads you through the process. Eowyn Company has the following potentially dilutive securities outstanding throughout all of 2048: 5.000x 6% x $100 - 30.000 2x5.000 - 10.000 CS 5,000 shares of 6%, $100 par convertible preferred stock, each of which is convertible into two common shares. Isted at Par $1,000,000 face value of 6% convertible bonds which were issued at 100. Each $1,000 bond is convertible into 25 shares of common stock. 1.000.000 x 6% x 6% - 3600 1.000.000 1.000 x 75 = 25.000 shares Warrants for 20,000 common shares. The warrants have an exercise price of $30 and the average share price during the year was $40. 20.000 x $30 - boo.000 boo.000 140: 15.000 Eowyn reported after-tax net income of $250,000 during 2048 and had 100,000 weighted average common shares outstanding. The tax rate is 40% and the preferred dividends had been declared. Interest Expense 1.000.000 x 6% XII-20%) = 36,000 Calculate Basic EPS. Show your work and put your final answer in the intimidating answer box ($250.000 - 30,000)/100.000 = $2.2 $2.2 (1-3) calculate it by Calculate the Dilution Index for each security and rank the securities from smallest to largest Index change Security Numerator Dilution Rank Denominator Index Convertible Preferred Stock +10.000 shares 3 3 Convertible Bonds +36.000 Unterest) + 25.000 shares 1.44 2 Warrants 20.000 common 0 - 15,000 Treasury o 1 CHAPTER 16 IN-CLASS ACTIVITY | PAGE 1 + To calculate Diluted EPS, begin by including the security with the smallest Dilution Index. Then proceed down the list, including securities (one at a time with Dilution Indices smaller than the last EPS figure you calculated. When the next Dilution Index exceeds your last EPS calculation, STOP. This is Diluted EPS. Why? Because math. In other words, adding a higher marginal EPS to your previous number will cause EPS to increase. And remember... the whole purpose of Diluted EPS is to show the smallest number possible. Calculate Diluted EPS. Show your work and put your final answer in the answer box $1.97 250.000 - 30.000 +0 100.000 +70,000 -15.000 $2.10 is bigger than 1.44 ekeep) @ 250.000 - 20.000 + 0 + 36.000 $1.99) is smaller than 3 (the next dilution 100.000 + 70.000-15000 +75.000 index) PART 2: COMPENSATORY STOCK OPTIONS On January 1, 2014, Arwen Corporation adopted a compensatory stock option plan for its top employees. Ten thousand options were granted in total, in two separate tranches. The first tranche covers 6,000 options with a two- year service period (ending December 31, 20Y5). The second tranche covers 4,000 options with a four-year service period (ending December 31, 20Y7). On the grant date (January 1, 20Y4), Arwen's $1 par common stock was trading for $30, the fair value of the options in the first tranche was $18, and the fair value of the options in the second tranche was $23. How much option-related compensation expense will Arwen recognize each year and in total? 02 Year Compensation Expense 20Y4 2045 20Y6 2047 Total During 20Y6, 75% of the options from the first tranche were exercised. If APIC - Common Stock increased by $166,500 as a result of the exercise, what was the option (exercise) price? Exercise Price =