Answered step by step

Verified Expert Solution

Question

1 Approved Answer

CHAPTER 18! PLEASE HELP THIS IS DUE SOON Continuing Case 65. Retirement Income Forecast Jamie Lee and Ross, now 57 and still very active, have

CHAPTER 18! PLEASE HELP THIS IS DUE SOON

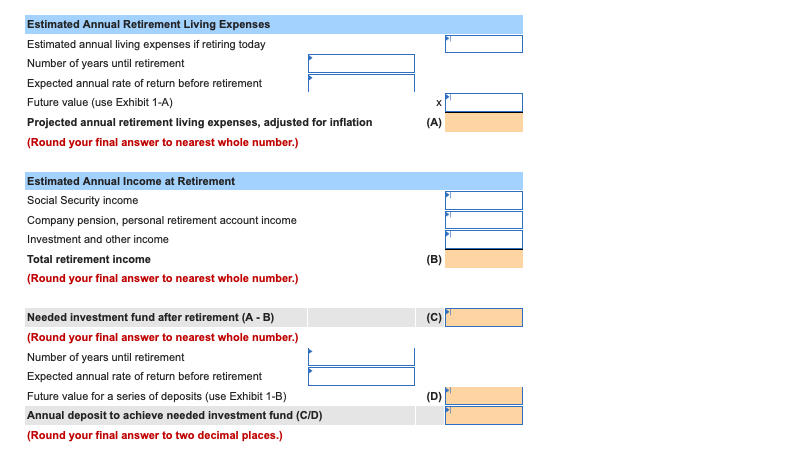

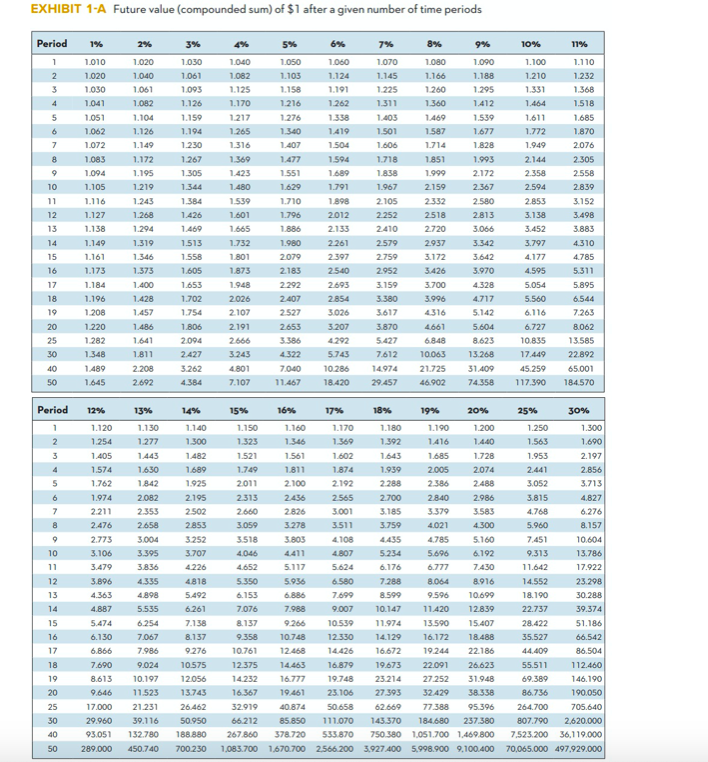

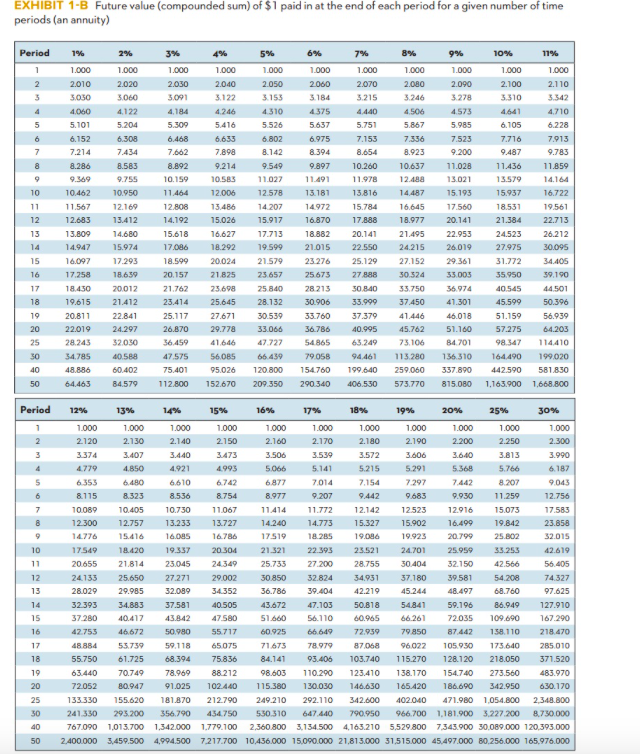

Continuing Case 65. Retirement Income Forecast Jamie Lee and Ross, now 57 and still very active, have plenty of time on their hands now that the triplets are away at college. They both realized that time has just flown by; over twenty-four years have passed since they married! Looking back over the past years, they realized that they have worked hard in their careers, Jamie Lee as the proprietor of a cupcake caf and Ross, self-employed as a web-page designer. They have enjoyed raising their family and strived to be financially sound as they are looking to retirement that is just around the corner. They saved regularly and invested wisely over the years. They rebounded nicely from the economic crisis over the past few years, as they watched their investments closely and adjusted their strategies when they felt it necessary. They purchase vehicles with cash and do not carry credit card balances, choosing instead to use them for convenience only. The triplets are pursuing their master's degrees and have tuition covered through work/study programs at the university. Jamie Lee and Ross are just a few short years from realizing their goals of retiring at 65 and purchasing a home at the beach! They are reviewing their financial situation to ensure they will be ready for retirement. They anticipate being able to live comfortably with 80% of their current expenses. The rate of return on their investments until they retire is 4%. They expect this percentage to drop to 3% after retirement. Use this information, along with Exhibit 1-A, Exhibit 1-B, and the information provided below to determine the annual deposit amount Jamie Lee and Ross will need to make until they retire in order to make up the shortfall between their estimated expenses and income needed during retirement. Each answer must have a value for the assignment to be complete. Enter "O" for any unused categories. Current Expense Amounts (Jamie Lee and Ross Combined). Fixed expenses: $3,200/month Variable expenses: $2,200/month Estimated Income Amounts (Jamie Lee and Ross Combined) Social Security: $2,300/month Current IRA balance: $91,000 Estimated IRA withdrawal: $300/month Other investments: $27,400/year Estimated Annual Retirement Living Expenses Estimated annual living expenses if retiring today Number of years until retirement Expected annual rate of return before retirement Future value (use Exhibit 1-A) Projected annual retirement living expenses, adjusted for inflation (Round your final answer to nearest whole number.) (A) Estimated Annual Income at Retirement Social Security income Company pension, personal retirement account income Investment and other income Total retirement income (Round your final answer to nearest whole number.) Needed investment fund after retirement (A - B) (Round your final answer to nearest whole number.) Number of years until retirement Expected annual rate of return before retirement Future value for a series of deposits (use Exhibit 1-B) Annual deposit to achieve needed investment fund (C/D) (Round your final answer to two decimal places.) EXHIBIT 1-A Future value (compounded sum) of $1 after a given number of time periods 1 Period 1 2 3 4 5 1% 1 010 1 .020 1030 1041 1051 1.062 1.072 1.083 1 094 2% 1020 1.040 1.061 1.082 .104 1.126 1.149 1.172 1195 11% 1.110 1.232 1368 1518 3% 1030 1.061 1 093 1.126 1.159 1.194 .230 .267 1305 4% 1040 1.082 1.125 1.170 1.217 1.265 1316 1.369 1423 5% 10 1050 1 103 1.158 1.216 1.276 10% 1.100 1.210 1.331 1.464 1.611 1 13.40 1.407 1.772 1.949 8 1 1477 1551 9 10 1.105 1.219 1.344 1.480 1.629 11 1.116 1.243 1 384 1.539 12 1.1271.2681.426 1.601 13 1 .138 1.294 1469 1665 1.149 1.319 1.513 1732 151.1611 .3461.5581801 16 1.173 1373 1605 1 873 17 1.184 1.400 1.653 1948 18 1.196 1.428 1.702 2 026 1.208 1.457 1.754 2107 1220 1.486 1.806 2191 25 1.282 1.641 2094 2666 30 1 .348 1.811 2.427 3243 40 1.489 2.208 3.262 4.801 50 1.645 2.692 4.384 7.107 1710 1.796 1886 1.980 2079 2.183 2292 2407 2.527 2653 3.386 4.322 7.040 11.467 6% 7% 8% 9% 1060 1070 1070 1080 1080 1.090 1.090 1124 .145 1.1661.188 1.191 1225 1.260 1.295 1.262 1.311 1.360 1.412 1358 1.403 1469 1.5.39 1419 1501 1.587 1.677 1504 1 .606 1714 TRR 1.594 1.718 1.851 1.993 1689 1838 1999 2.172 1.791 1.967 2159 2.367 1898 2.105 2332 2.580 2012 2.252 2518 2.813 2133 2410 2720 3.066 2261 2579 2 937 3.342 2397 2759 3.172 3.642 2540 2.952 3.426 3.970 2693 3.159 3 .700 4.328 2854 3.380 3.996 4717 3.026 3.617 4.316 5.142 3.207 38704661 5.604 42925.427 68.48 8.623 .743 7.612 10.063 13.268 10.286 14974 21.725 31.409 18.420 29.457 46.902 7 4.358 2.144 2358 2.594 2.853 3.138 3.452 3.797 4.177 4.595 5.054 5.560 6.116 6.727 10.835 17.449 45.259 117.390 1.685 1.870 2076 2.305 2.558 2.839 3152 3.498 3.883 4310 4.785 5.311 5.895 6544 7.263 20 8.062 5 13.585 22.892 65.001 184.570 Period 12% 1.120 1.254 13% 1.130 1.277 14% 1.140 1.500 2 1.405 1.443 1482 16.30 1.574 1.762 1.974 2.211 1689 1.925 2.195 2.502 2853 3.252 3.707 1842 2082 2.353 2658 3,004 3.395 3.836 D E o o ovan 2.773 3.106 3.479 4226 4.335 4818 3.896 4.363 4887 15% 1150 1.323 1.323 1.521 1.740 2011 2.313 2.660 3.059 3.518 4.046 4.652 5.350 6.153 7,076 8. 137 9.358 10.761 12375 14.232 1 6.367 32.919 66.212 267.860 ,083.700 16% 1160 13.46 1.346 1.561 1811 2.100 2.436 2826 3.278 3.803 4.411 5 117 5.936 6.886 7.988 9.266 10.748 12.468 14.463 16.777 19.461 40.874 85.850 378.720 1.670.700 17% 18% 19% 20% 1170 1.180 .190 1 .200 1360 1.369 1392 1392 1416 1.4.40 1.602 1 643 1.685 1.728 1874 1939 2.005 2074 2.192 2.288 2.386 2.488 2.565 2.700 2.840 2.986 3.001 3.185 5.379 3.583 3511 3.759 4.021 4.300 4108 4.435 4.785 5.160 4807 5.234 5.696 6.192 5624 6 176 6.777 7430 6.580 7.288 8.064 8.916 7.699 8.599 9.596 10.699 9.007 10.147 11.420 12.839 10539 11.974 13590 15.407 12 330 14.129 16.172 18.488 14426 16,672 19.244 22.186 16,879 19.673 22.091 26.623 19.748 23 214 27.252 31.948 23.106 27.393 3 2.429 38.338 50.658 62.669 7 7388 95.396 111.070 143.370 184.680 237.380 533.870 750.380 1.051.700 1.469.800 2.566.2003.927.400 5.998.900 9.100.400 25% 30% 1.250 1.300 1.563 1.690 1.953 2.197 2.441 2.856 3.052 3.713 3.815 4.827 4.768 6.276 5.960 8.157 7.451 10.604 9.313 13.786 11.642 17.922 14.552 23.298 18.190 30.288 22.737 39.374 28.422 51.186 35.527 66.542 44.409 86.504 55.511 112.460 69.389 46.190 86.736 190.050 264.700 705.640 807.790 2.620.000 7.523.200 36,119.000 70,065.000 497.929.000 4898 5515 5.474 6.254 6.130 7.067 6.866 7.986 7.6909 .024 8.613 10.197 9.646 11.523 17.000 21.231 29.960 39.116 93.051 132.780 289.000 450.740 5.492 6.261 7138 8.137 9.276 10.575 12056 13.743 26.462 50.950 188.880 700.230 25 50 EXHIBIT 1-B Future value (compounded sum) of $1 paid in at the end of each period for a given number of time periods (an annuity) Period 7% 8% 9% 10% 11% 1.000 1.000 1.000 1.000 1.000 2 4 5 7 8 9 10 11 12 13 14 15 1% 1.000 2.010 3.050 4 .060 5 .101 6.152 7 .214 8 .286 9 .369 10.462 11.567 12.683 13.809 14.947 14.097 17.258 18.450 19.615 2 0.811 22019 28.245 34.785 48.886 64.463 2% 3% 4% 5% 6% 1.000 1.000 1.000 1.000 1.000 2.020 2.030 2.040 2.050 2060 3060 3.091 3.122 3.153 3184 4.122 4,184 4.246 4.310 4 .375 5.204 5.3095.416 5.526 5637 6.308 6.468 6.633 6.802 6 .975 7.4347 .6627 .898 8.142 8.394 8.583 8.892 9.214 9.549 0.897 9.755 10.159 10.583 11.027 11 491 10.950 11.464 12.006 12.578 13.181 12.169 1 2808 1 3 486 14 207 14972 13.412 14.192 15.026 15.917 16.870 14.680 15.618 16.627 17.713 18 882 15.974 17.086 1 8.292 19.599 21.015 17.293 1 8.599 20.024 21.579 23.276 1659 20.157 218252365725673 2 0.012 21.762 23.698 25.840 28 213 21412 2 3.414 25.645 2 8.132 30 906 22.841 25.117 27.671 30.539 33.760 24.297 26.870 29.778 33.066 36.786 32030 36.459 41.646 47727 54.865 40.588 47.575 56.085 66.439 79058 60.402 7 5.401 9 5.026 120.800 154.760 84.579 112.800 152.670 209.350290.340 2.070 2.080 2.090 2.100 2.110 3 .215 3.246 3.278 5.310 3.342 4.440 4.506 4.573 4641 4.710 5.7515.8575.9856.1056.228 7.153 7336 7523 7.716 7913 8.654 8.9239.2009.487 9.783 10.260 10.637 11.028 11.436 11.859 11.978 12.438 1 3,021 13579 14.164 1 3.816 14.487 15.193 15.937 16.722 15.784 16.645 17.560 18.531 19561 17.888 1 8.977 20.141 21.384 22.713 20.141 2 1.495 2 2.953 24.523 26.212 22.550 24.215 26.019 27.975 30.095 25.129 27.152 29.361 31.772 34.405 2788830.324 33 003 35.950 39,190 50.840 33.750 36,974 40.545 44.501 33.999 37.450 41.301 45.599 50.596 37.379 41.446 4 6.018 51.159 56.939 40.905 45.762 51.160 57.275 64.203 63.249 73.106 84.701 98.347 114.410 94.461 113.280 136.310 164.490 199.020 199.640 259,060 337.890 442.590 581.850 406,530 573.770815.080 1.163.900 1.668.800 17 18 19 20 25 30 40 50 Period 12% 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 1.000 2130 1.000 2140 3.440 4.921 6.742 1.000 2.120 3.374 4.779 6353 8.115 10089 12.300 14.776 17.549 20.655 3.407 4,850 6.480 8.323 10.405 12.757 15.416 18.420 21.814 6.610 8.536 10.730 13.233 14.095 19337 23.045 27 271 25.650 29.985 32089 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 2150 100 2.170 2.180 2.190 2.200 2.250 2.300 3.473 3506 3.539 3.572 3.606 3.990 4.995 5066 5.141 5.215 5.291 5.368 5.766 6 .187 6.877 7,014 7.154 7.297 7442 8.207 9043 8.754 8.977 9.207 9.442 9.683 9.950 11.259 12.756 11.067 11.414 11.772 1 2.142 1 2523 12016 15.073 17583 13.727 14.240 14.773 15.327 15.902 16.499 1 9.842 23.858 16.786 17519 1 8.285 19.086 19.923 20.799 25.802 3 2.015 20.504 21.321 22.393 23.521 24.701 25.959 33.253 42.619 24349 25.733 27 200 28.755 30404 32.150 4 2566 55.405 20 002 30.850 32.824 34.931 3 7.180 3 9,581 54.208 74.327 34.352 36.786 39.404 42.219 45.244 48.497 68.760 97.625 40.505 4 3.672 47.103 50.818 54.841 59.196 86.949 127.910 47.580 51.660 56.110 60.965 66.261 72.035 109.690 167.290 55.717 60.925 66.649 72.939 79.850 8 7.442 138.110 218.470 65 075 71.675 7897987068 96072 105 950 175.640285 010 75.836 8 4,141 0 3.405 103.740 115.270 128 120 218,050 371.520 88.212 98.603 110.290 123.410 138.170 154.740 273.560 483.970 102.440 115.380 130.030 146.630 165.420 186.690 342.950 630.170 212.790 249.210 292.110 342.600 402.040 471.980 1,054.800 2.348.800 4 54.750 530.310 647.440 790.950 966.700 1.181.900 3.227.200 8.750.000 1.779.100 2.560.800 3.134.500 4.163.210 5,529.800 7.345.900 30,089.000 120,393.000 7.217.700 10,436.000 15.090.000 21,813.000 31,515.000 45,497.000 80.256.000 165,976.000 18 19 20 25 50 40 50 24.133 28.029 32 393 37.280 42.753 48 884 55.750 6 3.440 72.052 133.330 241.330 767,090 2.400.000 34.883 40.417 46.672 55759 61.725 70.749 80.947 155.620 295.200 1.015.700 3,450.500 37.581 43.8.42 50.980 59.118 68.394 78.969 91.025 181.870 356.790 1,342.000 4,994.500 Continuing Case 65. Retirement Income Forecast Jamie Lee and Ross, now 57 and still very active, have plenty of time on their hands now that the triplets are away at college. They both realized that time has just flown by; over twenty-four years have passed since they married! Looking back over the past years, they realized that they have worked hard in their careers, Jamie Lee as the proprietor of a cupcake caf and Ross, self-employed as a web-page designer. They have enjoyed raising their family and strived to be financially sound as they are looking to retirement that is just around the corner. They saved regularly and invested wisely over the years. They rebounded nicely from the economic crisis over the past few years, as they watched their investments closely and adjusted their strategies when they felt it necessary. They purchase vehicles with cash and do not carry credit card balances, choosing instead to use them for convenience only. The triplets are pursuing their master's degrees and have tuition covered through work/study programs at the university. Jamie Lee and Ross are just a few short years from realizing their goals of retiring at 65 and purchasing a home at the beach! They are reviewing their financial situation to ensure they will be ready for retirement. They anticipate being able to live comfortably with 80% of their current expenses. The rate of return on their investments until they retire is 4%. They expect this percentage to drop to 3% after retirement. Use this information, along with Exhibit 1-A, Exhibit 1-B, and the information provided below to determine the annual deposit amount Jamie Lee and Ross will need to make until they retire in order to make up the shortfall between their estimated expenses and income needed during retirement. Each answer must have a value for the assignment to be complete. Enter "O" for any unused categories. Current Expense Amounts (Jamie Lee and Ross Combined). Fixed expenses: $3,200/month Variable expenses: $2,200/month Estimated Income Amounts (Jamie Lee and Ross Combined) Social Security: $2,300/month Current IRA balance: $91,000 Estimated IRA withdrawal: $300/month Other investments: $27,400/year Estimated Annual Retirement Living Expenses Estimated annual living expenses if retiring today Number of years until retirement Expected annual rate of return before retirement Future value (use Exhibit 1-A) Projected annual retirement living expenses, adjusted for inflation (Round your final answer to nearest whole number.) (A) Estimated Annual Income at Retirement Social Security income Company pension, personal retirement account income Investment and other income Total retirement income (Round your final answer to nearest whole number.) Needed investment fund after retirement (A - B) (Round your final answer to nearest whole number.) Number of years until retirement Expected annual rate of return before retirement Future value for a series of deposits (use Exhibit 1-B) Annual deposit to achieve needed investment fund (C/D) (Round your final answer to two decimal places.) EXHIBIT 1-A Future value (compounded sum) of $1 after a given number of time periods 1 Period 1 2 3 4 5 1% 1 010 1 .020 1030 1041 1051 1.062 1.072 1.083 1 094 2% 1020 1.040 1.061 1.082 .104 1.126 1.149 1.172 1195 11% 1.110 1.232 1368 1518 3% 1030 1.061 1 093 1.126 1.159 1.194 .230 .267 1305 4% 1040 1.082 1.125 1.170 1.217 1.265 1316 1.369 1423 5% 10 1050 1 103 1.158 1.216 1.276 10% 1.100 1.210 1.331 1.464 1.611 1 13.40 1.407 1.772 1.949 8 1 1477 1551 9 10 1.105 1.219 1.344 1.480 1.629 11 1.116 1.243 1 384 1.539 12 1.1271.2681.426 1.601 13 1 .138 1.294 1469 1665 1.149 1.319 1.513 1732 151.1611 .3461.5581801 16 1.173 1373 1605 1 873 17 1.184 1.400 1.653 1948 18 1.196 1.428 1.702 2 026 1.208 1.457 1.754 2107 1220 1.486 1.806 2191 25 1.282 1.641 2094 2666 30 1 .348 1.811 2.427 3243 40 1.489 2.208 3.262 4.801 50 1.645 2.692 4.384 7.107 1710 1.796 1886 1.980 2079 2.183 2292 2407 2.527 2653 3.386 4.322 7.040 11.467 6% 7% 8% 9% 1060 1070 1070 1080 1080 1.090 1.090 1124 .145 1.1661.188 1.191 1225 1.260 1.295 1.262 1.311 1.360 1.412 1358 1.403 1469 1.5.39 1419 1501 1.587 1.677 1504 1 .606 1714 TRR 1.594 1.718 1.851 1.993 1689 1838 1999 2.172 1.791 1.967 2159 2.367 1898 2.105 2332 2.580 2012 2.252 2518 2.813 2133 2410 2720 3.066 2261 2579 2 937 3.342 2397 2759 3.172 3.642 2540 2.952 3.426 3.970 2693 3.159 3 .700 4.328 2854 3.380 3.996 4717 3.026 3.617 4.316 5.142 3.207 38704661 5.604 42925.427 68.48 8.623 .743 7.612 10.063 13.268 10.286 14974 21.725 31.409 18.420 29.457 46.902 7 4.358 2.144 2358 2.594 2.853 3.138 3.452 3.797 4.177 4.595 5.054 5.560 6.116 6.727 10.835 17.449 45.259 117.390 1.685 1.870 2076 2.305 2.558 2.839 3152 3.498 3.883 4310 4.785 5.311 5.895 6544 7.263 20 8.062 5 13.585 22.892 65.001 184.570 Period 12% 1.120 1.254 13% 1.130 1.277 14% 1.140 1.500 2 1.405 1.443 1482 16.30 1.574 1.762 1.974 2.211 1689 1.925 2.195 2.502 2853 3.252 3.707 1842 2082 2.353 2658 3,004 3.395 3.836 D E o o ovan 2.773 3.106 3.479 4226 4.335 4818 3.896 4.363 4887 15% 1150 1.323 1.323 1.521 1.740 2011 2.313 2.660 3.059 3.518 4.046 4.652 5.350 6.153 7,076 8. 137 9.358 10.761 12375 14.232 1 6.367 32.919 66.212 267.860 ,083.700 16% 1160 13.46 1.346 1.561 1811 2.100 2.436 2826 3.278 3.803 4.411 5 117 5.936 6.886 7.988 9.266 10.748 12.468 14.463 16.777 19.461 40.874 85.850 378.720 1.670.700 17% 18% 19% 20% 1170 1.180 .190 1 .200 1360 1.369 1392 1392 1416 1.4.40 1.602 1 643 1.685 1.728 1874 1939 2.005 2074 2.192 2.288 2.386 2.488 2.565 2.700 2.840 2.986 3.001 3.185 5.379 3.583 3511 3.759 4.021 4.300 4108 4.435 4.785 5.160 4807 5.234 5.696 6.192 5624 6 176 6.777 7430 6.580 7.288 8.064 8.916 7.699 8.599 9.596 10.699 9.007 10.147 11.420 12.839 10539 11.974 13590 15.407 12 330 14.129 16.172 18.488 14426 16,672 19.244 22.186 16,879 19.673 22.091 26.623 19.748 23 214 27.252 31.948 23.106 27.393 3 2.429 38.338 50.658 62.669 7 7388 95.396 111.070 143.370 184.680 237.380 533.870 750.380 1.051.700 1.469.800 2.566.2003.927.400 5.998.900 9.100.400 25% 30% 1.250 1.300 1.563 1.690 1.953 2.197 2.441 2.856 3.052 3.713 3.815 4.827 4.768 6.276 5.960 8.157 7.451 10.604 9.313 13.786 11.642 17.922 14.552 23.298 18.190 30.288 22.737 39.374 28.422 51.186 35.527 66.542 44.409 86.504 55.511 112.460 69.389 46.190 86.736 190.050 264.700 705.640 807.790 2.620.000 7.523.200 36,119.000 70,065.000 497.929.000 4898 5515 5.474 6.254 6.130 7.067 6.866 7.986 7.6909 .024 8.613 10.197 9.646 11.523 17.000 21.231 29.960 39.116 93.051 132.780 289.000 450.740 5.492 6.261 7138 8.137 9.276 10.575 12056 13.743 26.462 50.950 188.880 700.230 25 50 EXHIBIT 1-B Future value (compounded sum) of $1 paid in at the end of each period for a given number of time periods (an annuity) Period 7% 8% 9% 10% 11% 1.000 1.000 1.000 1.000 1.000 2 4 5 7 8 9 10 11 12 13 14 15 1% 1.000 2.010 3.050 4 .060 5 .101 6.152 7 .214 8 .286 9 .369 10.462 11.567 12.683 13.809 14.947 14.097 17.258 18.450 19.615 2 0.811 22019 28.245 34.785 48.886 64.463 2% 3% 4% 5% 6% 1.000 1.000 1.000 1.000 1.000 2.020 2.030 2.040 2.050 2060 3060 3.091 3.122 3.153 3184 4.122 4,184 4.246 4.310 4 .375 5.204 5.3095.416 5.526 5637 6.308 6.468 6.633 6.802 6 .975 7.4347 .6627 .898 8.142 8.394 8.583 8.892 9.214 9.549 0.897 9.755 10.159 10.583 11.027 11 491 10.950 11.464 12.006 12.578 13.181 12.169 1 2808 1 3 486 14 207 14972 13.412 14.192 15.026 15.917 16.870 14.680 15.618 16.627 17.713 18 882 15.974 17.086 1 8.292 19.599 21.015 17.293 1 8.599 20.024 21.579 23.276 1659 20.157 218252365725673 2 0.012 21.762 23.698 25.840 28 213 21412 2 3.414 25.645 2 8.132 30 906 22.841 25.117 27.671 30.539 33.760 24.297 26.870 29.778 33.066 36.786 32030 36.459 41.646 47727 54.865 40.588 47.575 56.085 66.439 79058 60.402 7 5.401 9 5.026 120.800 154.760 84.579 112.800 152.670 209.350290.340 2.070 2.080 2.090 2.100 2.110 3 .215 3.246 3.278 5.310 3.342 4.440 4.506 4.573 4641 4.710 5.7515.8575.9856.1056.228 7.153 7336 7523 7.716 7913 8.654 8.9239.2009.487 9.783 10.260 10.637 11.028 11.436 11.859 11.978 12.438 1 3,021 13579 14.164 1 3.816 14.487 15.193 15.937 16.722 15.784 16.645 17.560 18.531 19561 17.888 1 8.977 20.141 21.384 22.713 20.141 2 1.495 2 2.953 24.523 26.212 22.550 24.215 26.019 27.975 30.095 25.129 27.152 29.361 31.772 34.405 2788830.324 33 003 35.950 39,190 50.840 33.750 36,974 40.545 44.501 33.999 37.450 41.301 45.599 50.596 37.379 41.446 4 6.018 51.159 56.939 40.905 45.762 51.160 57.275 64.203 63.249 73.106 84.701 98.347 114.410 94.461 113.280 136.310 164.490 199.020 199.640 259,060 337.890 442.590 581.850 406,530 573.770815.080 1.163.900 1.668.800 17 18 19 20 25 30 40 50 Period 12% 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 1.000 2130 1.000 2140 3.440 4.921 6.742 1.000 2.120 3.374 4.779 6353 8.115 10089 12.300 14.776 17.549 20.655 3.407 4,850 6.480 8.323 10.405 12.757 15.416 18.420 21.814 6.610 8.536 10.730 13.233 14.095 19337 23.045 27 271 25.650 29.985 32089 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 2150 100 2.170 2.180 2.190 2.200 2.250 2.300 3.473 3506 3.539 3.572 3.606 3.990 4.995 5066 5.141 5.215 5.291 5.368 5.766 6 .187 6.877 7,014 7.154 7.297 7442 8.207 9043 8.754 8.977 9.207 9.442 9.683 9.950 11.259 12.756 11.067 11.414 11.772 1 2.142 1 2523 12016 15.073 17583 13.727 14.240 14.773 15.327 15.902 16.499 1 9.842 23.858 16.786 17519 1 8.285 19.086 19.923 20.799 25.802 3 2.015 20.504 21.321 22.393 23.521 24.701 25.959 33.253 42.619 24349 25.733 27 200 28.755 30404 32.150 4 2566 55.405 20 002 30.850 32.824 34.931 3 7.180 3 9,581 54.208 74.327 34.352 36.786 39.404 42.219 45.244 48.497 68.760 97.625 40.505 4 3.672 47.103 50.818 54.841 59.196 86.949 127.910 47.580 51.660 56.110 60.965 66.261 72.035 109.690 167.290 55.717 60.925 66.649 72.939 79.850 8 7.442 138.110 218.470 65 075 71.675 7897987068 96072 105 950 175.640285 010 75.836 8 4,141 0 3.405 103.740 115.270 128 120 218,050 371.520 88.212 98.603 110.290 123.410 138.170 154.740 273.560 483.970 102.440 115.380 130.030 146.630 165.420 186.690 342.950 630.170 212.790 249.210 292.110 342.600 402.040 471.980 1,054.800 2.348.800 4 54.750 530.310 647.440 790.950 966.700 1.181.900 3.227.200 8.750.000 1.779.100 2.560.800 3.134.500 4.163.210 5,529.800 7.345.900 30,089.000 120,393.000 7.217.700 10,436.000 15.090.000 21,813.000 31,515.000 45,497.000 80.256.000 165,976.000 18 19 20 25 50 40 50 24.133 28.029 32 393 37.280 42.753 48 884 55.750 6 3.440 72.052 133.330 241.330 767,090 2.400.000 34.883 40.417 46.672 55759 61.725 70.749 80.947 155.620 295.200 1.015.700 3,450.500 37.581 43.8.42 50.980 59.118 68.394 78.969 91.025 181.870 356.790 1,342.000 4,994.500Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Horngrens Cost Accounting A Managerial Emphasis

Authors: Srikant Datar, Madhav Rajan

17th Global Edition

129236307X, 9781292363073