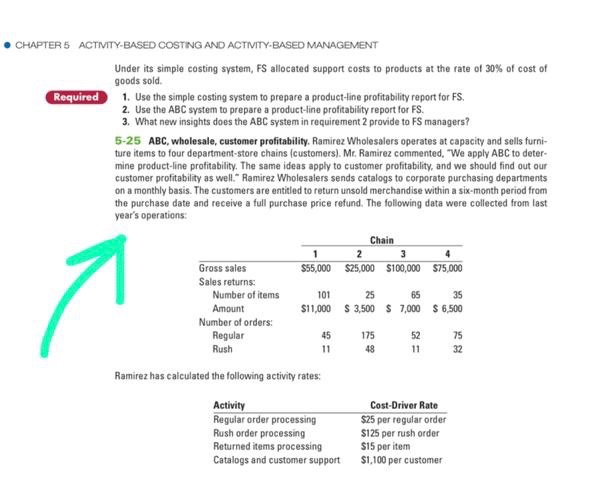

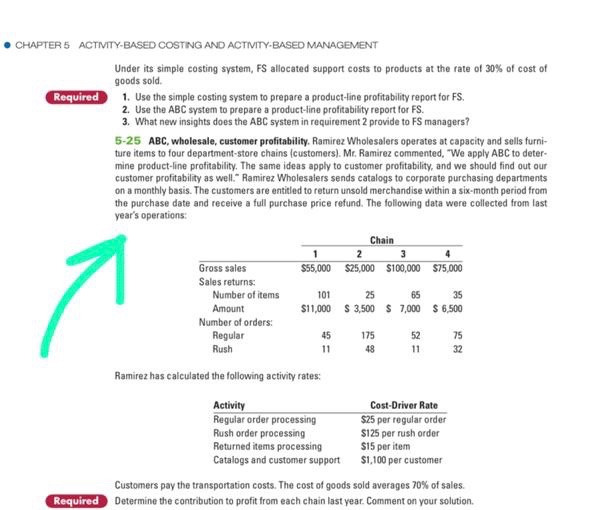

. CHAPTER 5 ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT Required Under its simple costing system, FS allocated support costs to products at the rate of 30% of cost of goods sold. 1. Use the simple costing system to prepare a product-line profitability report for FS. 2. Use the ABC system to prepare a product-line profitability report for FS. 3. What new insights does the ABC system in requirement 2 provide to FS managers? 5-25 ABC, wholesale, customer profitability. Ramirez Wholesalers operates at capacity and sells furni- ture items to four department store chains (customers). Mr. Ramirez commented, "We apply ABC to deter- mine product-line profitability. The same ideas apply to customer profitability, and we should find out our customer profitability as well." Ramirez Wholesalers sends catalogs to corporate purchasing departments on a monthly basis. The customers are entitled to return unsold merchandise within a six-month period from the purchase date and receive a full purchase price refund. The following data were collected from last year's operations 1 $55,000 Chain 2 3 $25,000 $100,000 4 $75,000 Gross sales Sales returns Number of items Amount Number of orders: Regular Rush 101 $11,000 2565 $3,500 $ 7,000 $ 6,500 45 175 1148 52 11 75 32 Ramirez has calculated the following activity rates: Activity Regular order processing Rush order processing Returned items processing Catalogs and customer support Cost-Driver Rate $25 per regular order $125 per rush order S15 per item $1,100 per customer . CHAPTER 5 ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT Required Under its simple costing system, FS allocated support costs to products at the rate of 30% of cost of goods sold. 1. Use the simple costing system to prepare a product-line profitability report for FS. 2. Use the ABC system to prepare a product-line profitability report for FS. 3. What new insights does the ABC system in requirement 2 provide to FS managers? 5-25 ABC, wholesale, customer profitability. Ramirez Wholesalers operates at capacity and sells furni- ture items to four department store chains (customers). Mr. Ramirez commented, "We apply ABC to deter- mine product-line profitability. The same ideas apply to customer profitability, and we should find out our customer profitability as well." Ramirez Wholesalers sends catalogs to corporate purchasing departments on a monthly basis. The customers are entitled to return unsold merchandise within a six-month period from the purchase date and receive a full purchase price refund. The following data were collected from last year's operations 1 $55,000 Chain 2 3 $25,000 $100,000 4 $75,000 Gross sales Sales returns Number of items Amount Number of orders: Regular Rush 101 $11,000 2565 $3,500 $ 7,000 $ 6,500 45 175 1148 52 11 75 32 Ramirez has calculated the following activity rates: Activity Regular order processing Rush order processing Returned items processing Catalogs and customer support Cost-Driver Rate $25 per regular order $125 per rush order S15 per item $1,100 per customer Customers pay the transportation costs. The cost of goods sold averages 70% of sales. Determine the contribution to profit from each chain last year. Comment on your solution Required