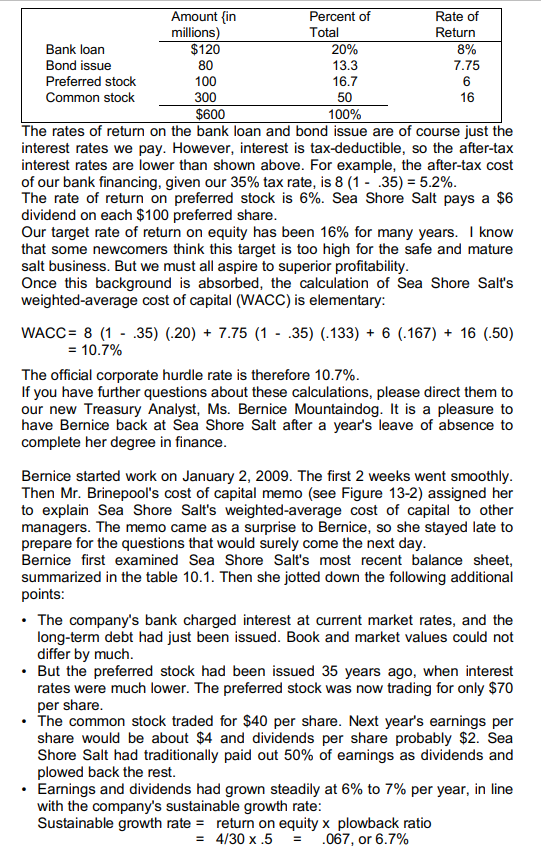

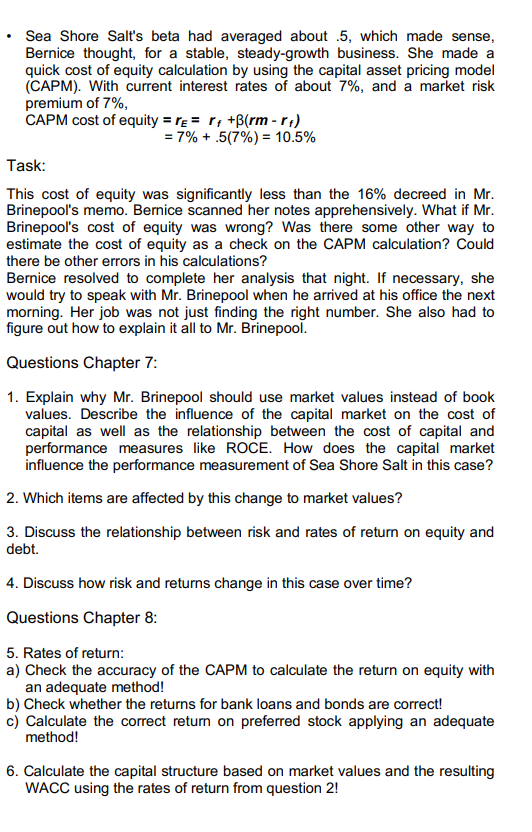

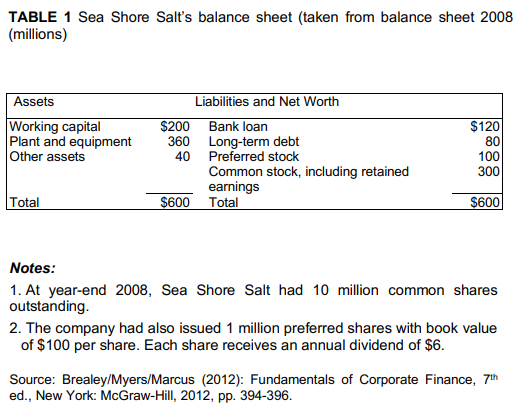

Chapter 8: The Weighted Average Cost of Capital and Company Valuation Case Study: Sea Shore Salt Bernice Mountaindog was glad to be back at Sea Shore Salt. Employees were treated well. When she had asked a year ago for a leave of absence to complete her degree in finance, top management promptly agreed. When she returned with an honors degree, she was promoted from administrative assistant (she had been secretary to Joe-Bob Brinepool, the president) to treasury analyst. Bernice thought the company's prospects were good. Sure, table salt was a mature business, but Sea Shore Salt had grown steadily at the expense of its less well known competitors. The company's brand name was an important advantage, despite the difficulty most customers had in pronouncing it rapidly. FIGURE 1 Mr. Brinepool's cost of capital memo Sea Shore Salt Company Spring Vacation Beach, Florida CONFIDENTIAL MEMORANDUM DATE: January 15, 2009 TO: S.S.S. Management FROM: Joe-Bob Brinepool, President SUBJECT: Cost of Capital This memo states and clarifies our company's long-standing policy regarding hurdle rates for capital investment decisions. There have been many recent questions, and some evident confusion, on this matter. Sea Shore Salt evaluates replacement and expansion investments by discounted cash flow. The discount or hurdle rate is the company's after- tax weighted average cost of capital. The weighted average cost of capital is simply a blend of the rates of return expected by investors in our company. These investors include banks, bondholders, and preferred stock investors in addition to common stockholders. Of course many of you are, or soon will be, stockholders of our company. The following table summarizes the composition of Sea Shore Salt's financing. Amount {in Percent of Rate of millions) Total Return Bank loan $120 20% 8% Bond issue 80 13.3 7.75 Preferred stock 100 16.7 6 Common stock 300 50 16 $600 100% The rates of return on the bank loan and bond issue are of course just the interest rates we pay. However, interest is tax-deductible, so the after-tax interest rates are lower than shown above. For example, the after-tax cost of our bank financing, given our 35% tax rate, is 8 (1 - 35) = 5.2%. The rate of return on preferred stock is 6%. Sea Shore Salt pays a $6 dividend on each $100 preferred share. Our target rate of return on equity has been 16% for many years. I know that some newcomers think this target is too high for the safe and mature salt business. But we must all aspire to superior profitability. Once this background is absorbed, the calculation of Sea Shore Salt's weighted average cost of capital (WACC) is elementary: WACC= 8 (1 - .35) (-20) + 7.75 (1 - .35) (.133) + 6 (.167) + 16 (50) = 10.7% The official corporate hurdle rate is therefore 10.7%. If you have further questions about these calculations, please direct them to our new Treasury Analyst, Ms. Bernice Mountaindog. It is a pleasure to have Bernice back at Sea Shore Salt after a year's leave of absence to complete her degree in finance. Bernice started work on January 2, 2009. The first 2 weeks went smoothly. Then Mr. Brinepool's cost of capital memo (see Figure 13-2) assigned her to explain Sea Shore Salt's weighted average cost of capital to other managers. The memo came as a surprise to Bernice, so she stayed late to prepare for the questions that would surely come the next day. Bernice first examined Sea Shore Salt's most recent balance sheet, summarized in the table 10.1. Then she jotted down the following additional points: The company's bank charged interest at current market rates, and the long-term debt had just been issued. Book and market values could not differ by much. But the preferred stock had been issued 35 years ago, when interest rates were much lower. The preferred stock was now trading for only $70 per share. The common stock traded for $40 per share. Next year's earnings per share would be about $4 and dividends per share probably $2. Sea Shore Salt had traditionally paid out 50% of earnings as dividends and plowed back the rest. Earnings and dividends had grown steadily at 6% to 7% per year, in line with the company's sustainable growth rate: Sustainable growth rate = return on equity x plowback ratio = 4/30 x.5 = .067, or 6.7% Sea Shore Salt's beta had averaged about .5, which made sense, Bernice thought, for a stable, steady-growth business. She made a quick cost of equity calculation by using the capital asset pricing model (CAPM). With current interest rates of about 7%, and a market risk premium of 7% CAPM cost of equity = r = r +B(rm - rt) = 7% +.5(7%) = 10.5% Task: This cost of equity was significantly less than the 16% decreed in Mr. Brinepool's memo. Bernice scanned her notes apprehensively. What if Mr. Brinepool's cost of equity was wrong? Was there some other way to estimate the cost of equity as a check on the CAPM calculation? Could there be other errors in his calculations? Bernice resolved to complete her analysis that night. If necessary, she would try to speak with Mr. Brinepool when he arrived at his office the next morning. Her job was not just finding the right number. She also had to figure out how to explain it all to Mr. Brinepool. Questions Chapter 7: 1. Explain why Mr. Brinepool should use market values instead of book values. Describe the influence of the capital market on the cost of capital as well as the relationship between the cost of capital and performance measures like ROCE. How does the capital market influence the performance measurement of Sea Shore Salt in this case? 2. Which items are affected by this change to market values? 3. Discuss the relationship between risk and rates of return on equity and debt. 4. Discuss how risk and returns change in this case over time? Questions Chapter 8: 5. Rates of return: a) Check the accuracy of the CAPM to calculate the return on equity with an adequate method! b) Check whether the returns for bank loans and bonds are correct! c) Calculate the correct return on preferred stock applying an adequate method! 6. Calculate the capital structure based on market values and the resulting WACC using the rates of return from question 2! TABLE 1 Sea Shore Salt's balance sheet (taken from balance sheet 2008 (millions) Assets Working capital Plant and equipment Other assets Liabilities and Net Worth $200 Bank loan 360 Long-term debt 40 Preferred stock Common stock, including retained earnings $600 Total $120 80 100 300 Total $600 Notes: 1. At year-end 2008, Sea Shore Salt had 10 million common shares outstanding. 2. The company had also issued 1 million preferred shares with book value of $100 per share. Each share receives an annual dividend of $6. Source: Brealey/Myers/Marcus (2012): Fundamentals of Corporate Finance, 7th ed., New York: McGraw-Hill, 2012, pp. 394-396. Chapter 8: The Weighted Average Cost of Capital and Company Valuation Case Study: Sea Shore Salt Bernice Mountaindog was glad to be back at Sea Shore Salt. Employees were treated well. When she had asked a year ago for a leave of absence to complete her degree in finance, top management promptly agreed. When she returned with an honors degree, she was promoted from administrative assistant (she had been secretary to Joe-Bob Brinepool, the president) to treasury analyst. Bernice thought the company's prospects were good. Sure, table salt was a mature business, but Sea Shore Salt had grown steadily at the expense of its less well known competitors. The company's brand name was an important advantage, despite the difficulty most customers had in pronouncing it rapidly. FIGURE 1 Mr. Brinepool's cost of capital memo Sea Shore Salt Company Spring Vacation Beach, Florida CONFIDENTIAL MEMORANDUM DATE: January 15, 2009 TO: S.S.S. Management FROM: Joe-Bob Brinepool, President SUBJECT: Cost of Capital This memo states and clarifies our company's long-standing policy regarding hurdle rates for capital investment decisions. There have been many recent questions, and some evident confusion, on this matter. Sea Shore Salt evaluates replacement and expansion investments by discounted cash flow. The discount or hurdle rate is the company's after- tax weighted average cost of capital. The weighted average cost of capital is simply a blend of the rates of return expected by investors in our company. These investors include banks, bondholders, and preferred stock investors in addition to common stockholders. Of course many of you are, or soon will be, stockholders of our company. The following table summarizes the composition of Sea Shore Salt's financing. Amount {in Percent of Rate of millions) Total Return Bank loan $120 20% 8% Bond issue 80 13.3 7.75 Preferred stock 100 16.7 6 Common stock 300 50 16 $600 100% The rates of return on the bank loan and bond issue are of course just the interest rates we pay. However, interest is tax-deductible, so the after-tax interest rates are lower than shown above. For example, the after-tax cost of our bank financing, given our 35% tax rate, is 8 (1 - 35) = 5.2%. The rate of return on preferred stock is 6%. Sea Shore Salt pays a $6 dividend on each $100 preferred share. Our target rate of return on equity has been 16% for many years. I know that some newcomers think this target is too high for the safe and mature salt business. But we must all aspire to superior profitability. Once this background is absorbed, the calculation of Sea Shore Salt's weighted average cost of capital (WACC) is elementary: WACC= 8 (1 - .35) (-20) + 7.75 (1 - .35) (.133) + 6 (.167) + 16 (50) = 10.7% The official corporate hurdle rate is therefore 10.7%. If you have further questions about these calculations, please direct them to our new Treasury Analyst, Ms. Bernice Mountaindog. It is a pleasure to have Bernice back at Sea Shore Salt after a year's leave of absence to complete her degree in finance. Bernice started work on January 2, 2009. The first 2 weeks went smoothly. Then Mr. Brinepool's cost of capital memo (see Figure 13-2) assigned her to explain Sea Shore Salt's weighted average cost of capital to other managers. The memo came as a surprise to Bernice, so she stayed late to prepare for the questions that would surely come the next day. Bernice first examined Sea Shore Salt's most recent balance sheet, summarized in the table 10.1. Then she jotted down the following additional points: The company's bank charged interest at current market rates, and the long-term debt had just been issued. Book and market values could not differ by much. But the preferred stock had been issued 35 years ago, when interest rates were much lower. The preferred stock was now trading for only $70 per share. The common stock traded for $40 per share. Next year's earnings per share would be about $4 and dividends per share probably $2. Sea Shore Salt had traditionally paid out 50% of earnings as dividends and plowed back the rest. Earnings and dividends had grown steadily at 6% to 7% per year, in line with the company's sustainable growth rate: Sustainable growth rate = return on equity x plowback ratio = 4/30 x.5 = .067, or 6.7% Sea Shore Salt's beta had averaged about .5, which made sense, Bernice thought, for a stable, steady-growth business. She made a quick cost of equity calculation by using the capital asset pricing model (CAPM). With current interest rates of about 7%, and a market risk premium of 7% CAPM cost of equity = r = r +B(rm - rt) = 7% +.5(7%) = 10.5% Task: This cost of equity was significantly less than the 16% decreed in Mr. Brinepool's memo. Bernice scanned her notes apprehensively. What if Mr. Brinepool's cost of equity was wrong? Was there some other way to estimate the cost of equity as a check on the CAPM calculation? Could there be other errors in his calculations? Bernice resolved to complete her analysis that night. If necessary, she would try to speak with Mr. Brinepool when he arrived at his office the next morning. Her job was not just finding the right number. She also had to figure out how to explain it all to Mr. Brinepool. Questions Chapter 7: 1. Explain why Mr. Brinepool should use market values instead of book values. Describe the influence of the capital market on the cost of capital as well as the relationship between the cost of capital and performance measures like ROCE. How does the capital market influence the performance measurement of Sea Shore Salt in this case? 2. Which items are affected by this change to market values? 3. Discuss the relationship between risk and rates of return on equity and debt. 4. Discuss how risk and returns change in this case over time? Questions Chapter 8: 5. Rates of return: a) Check the accuracy of the CAPM to calculate the return on equity with an adequate method! b) Check whether the returns for bank loans and bonds are correct! c) Calculate the correct return on preferred stock applying an adequate method! 6. Calculate the capital structure based on market values and the resulting WACC using the rates of return from question 2! TABLE 1 Sea Shore Salt's balance sheet (taken from balance sheet 2008 (millions) Assets Working capital Plant and equipment Other assets Liabilities and Net Worth $200 Bank loan 360 Long-term debt 40 Preferred stock Common stock, including retained earnings $600 Total $120 80 100 300 Total $600 Notes: 1. At year-end 2008, Sea Shore Salt had 10 million common shares outstanding. 2. The company had also issued 1 million preferred shares with book value of $100 per share. Each share receives an annual dividend of $6. Source: Brealey/Myers/Marcus (2012): Fundamentals of Corporate Finance, 7th ed., New York: McGraw-Hill, 2012, pp. 394-396