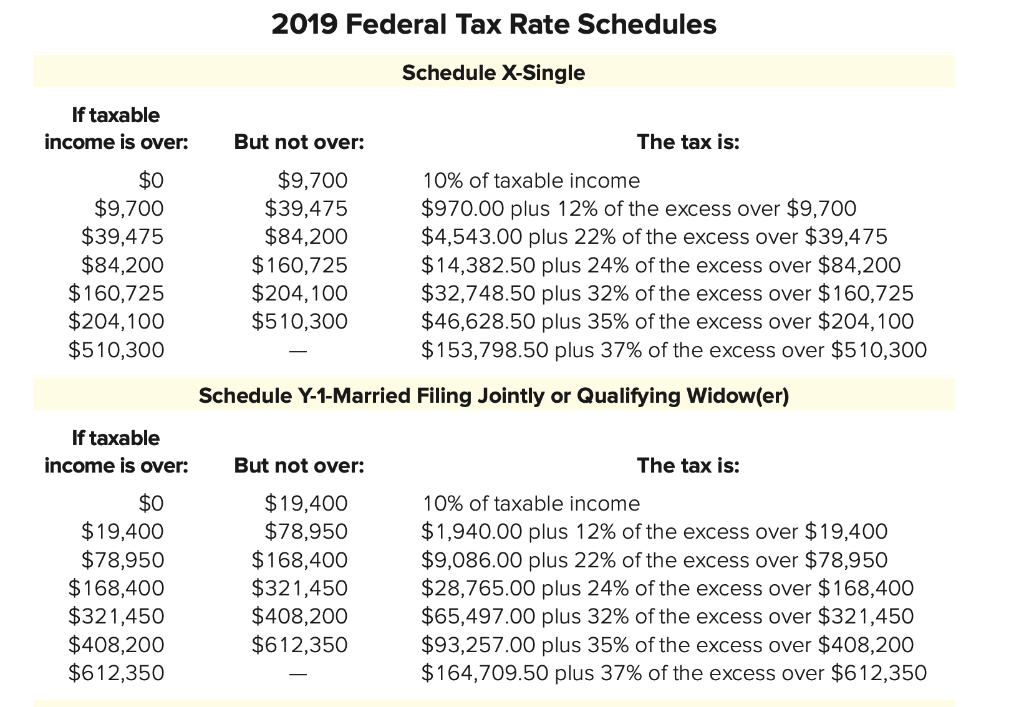

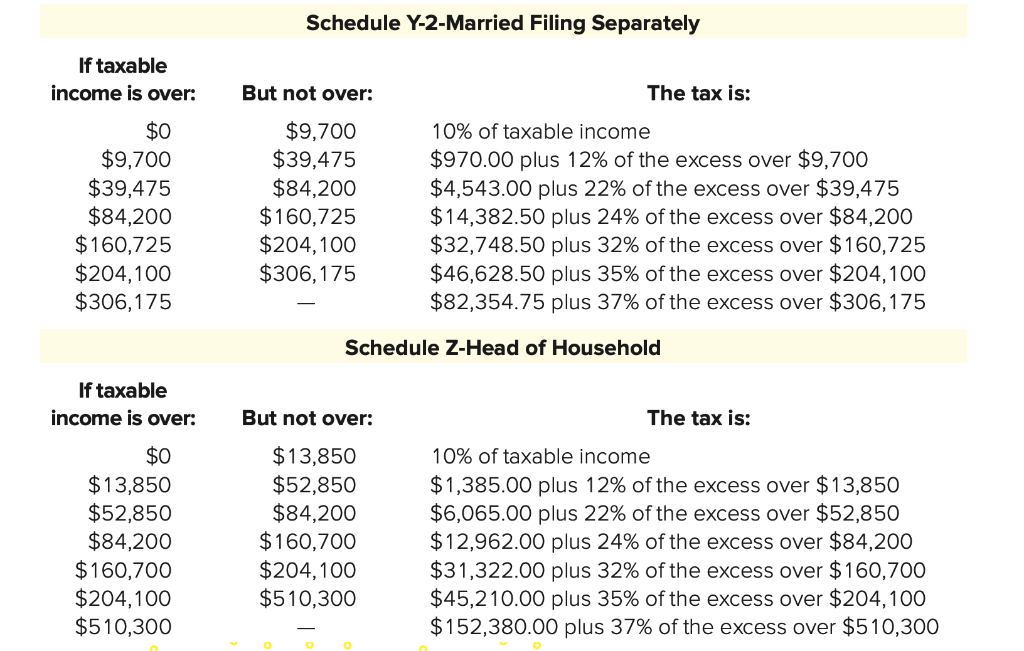

Charles and Joan Thompson file a joint return. In 2018, they had taxable income of $92,370 and paid tax of $12,202. Charles is an advertising executive, and Joan is a college professor. During the fall 2019 semester, Joan is planning to take a leave of absence without pay. The Thompsons expect their taxable income to drop to $70,000 in 2019. They expect their 2019 tax liability will be $8,015, which will be the approximate amount of their withholding. Joan anticipates that she will work on academic research during the fall semester. During September, Joan decides to perform consulting services for some local businesses. Charles and Joan had not anticipated this development. Joan is paid a total of $35,000 during October, November, and December for her work. Use the appropriate Tax Rate Schedules. Required: a. What estimated tax payments are Charles and Joan required to make, if any, for tax year 2019? 2019 Federal Tax Rate Schedules Schedule X-Single If taxable income is over: But not over: The tax is: $0 $9,700 $39,475 $84,200 $160,725 $204,100 $510,300 $9,700 $39,475 $84,200 $160,725 $204,100 $510,300 10% of taxable income $970.00 plus 12% of the excess over $9,700 $4,543.00 plus 22% of the excess over $39,475 $14,382.50 plus 24% of the excess over $84,200 $32,748.50 plus 32% of the excess over $160,725 $46,628.50 plus 35% of the excess over $204,100 $153,798.50 plus 37% of the excess over $510,300 Schedule Y-1-Married Filing Jointly or Qualifying Widow(er) If taxable income is over: But not over: The tax is: $0 $19,400 $78,950 $168,400 $321,450 $408,200 $612,350 $19,400 $78,950 $168,400 $321,450 $408,200 $612,350 10% of taxable income $1,940.00 plus 12% of the excess over $19,400 $9,086.00 plus 22% of the excess over $78,950 $28,765.00 plus 24% of the excess over $168,400 $65,497.00 plus 32% of the excess over $321,450 $93,257.00 plus 35% of the excess over $408,200 $164,709.50 plus 37% of the excess over $612,350 Schedule Y-2-Married Filing Separately If taxable income is over: But not over: The tax is: $0 $9,700 $39,475 $84,200 $160,725 $204,100 $306, 175 $9,700 $39,475 $84,200 $160,725 $204,100 $306,175 10% of taxable income $970.00 plus 12% of the excess over $9,700 $4,543.00 plus 22% of the excess over $39,475 $14,382.50 plus 24% of the excess over $84,200 $32,748.50 plus 32% of the excess over $160,725 $46,628.50 plus 35% of the excess over $204,100 $82,354.75 plus 37% of the excess over $306,175 Schedule Z-Head of Household If taxable income is over: But not over: The tax is: $0 $13,850 $52,850 $84,200 $160,700 $204,100 $510,300 $13,850 $52,850 $84,200 $160,700 $204,100 $510,300 10% of taxable income $1,385.00 plus 12% of the excess over $13,850 $6,065.00 plus 22% of the excess over $52,850 $12,962.00 plus 24% of the excess over $84,200 $31,322.00 plus 32% of the excess over $160,700 $45,210.00 plus 35% of the excess over $204,100 $152,380.00 plus 37% of the excess over $510,300 Qualified Dividends & Capital Gains Tax Rates Standard Mileage Rates 28% Business miles $0.58 Collectible gain Section 1202 gain 28% $0.14 Charity miles Medical miles $0.20 Moving miles $0.20 Child Tax Credit Amount per child under 17 $2,000 Credit reduction-$50 per $1,000 over AGI threshold Married filing jointly $400,000 All other taxpayers $200,000 Unrecaptured Section 1250 gain 25% Other capital gains and qualified dividends based on taxable income: Zero tax rate: Single & Married filing separately: taxable income of $0-$39,375 Married filing jointly: taxable income of $0-$78,750 Head of household: taxable income of $0-$52,750 15% tax rate: Single & Married filing separately: taxable income of $39,376-$434,550 Married filing jointly: taxable income of $78,751-$488,850 Head of household: taxable income of $52,751-$461,700 20% tax rate: Single and Married filing separately: taxable income of over $434,550 Married filing jointly: taxable income of over $488,850 Head of household: taxable income of over $461,700 Short-term capital gains (held 1 year or less) are taxed at ordinary tax rates Coverdell Educational Savings Accounts Contributions limit-$2,000 per year per beneficiary, must be in cash, and must be made before the beneficiary turns 18. Phase-out Thresholds Married filing jointly-AGI Single-AGI $190,000-$220,000 $95,000-$110,000 Traditional IRA Contribution Deduction Standard Deduction IRA contributions-Lower of $6,000 or the amount of compensation Individuals who are age 50 or older-Lower of $7,000 or compensation. Filing Status Single Married filing jointly Married filing separately Head of household Qualifying widow(er) Additional over 65 or blind Married, qual. widow(er) Single/Head of household Basic Standard Deduction $12,200 $24,400 $12,200 $18,350 $24,400 Phase-outs if the individual is a participant in another retirement plan: Married $103,000-$123,000 Phase-out range Greater than $123,000-no deduction Single $64,000-$74,000 Phase-out range Greater than $74,000no deduction $1,300 $1,650 Roth IRA Contribution Social Security, Medicare, & Self-Employment Taxes Rate Income Limit Roth contribution $6,000 or compensation 50 or older $7,000 or compensation All Roth contributions are not tax deductible 6.2% $132,900 Unlimited Employee . Social Security Medicare Total Self-employed Social Security Medicare 1.45% 7.65% Joint Returns-$193,000-$203,000 phase-out range Rate Income Limit Single or head of household$122,000-$137,000 phase-out range 12.4% $132,900 Unlimited 2.9% 15.3% Health Savings Account Contribution Total