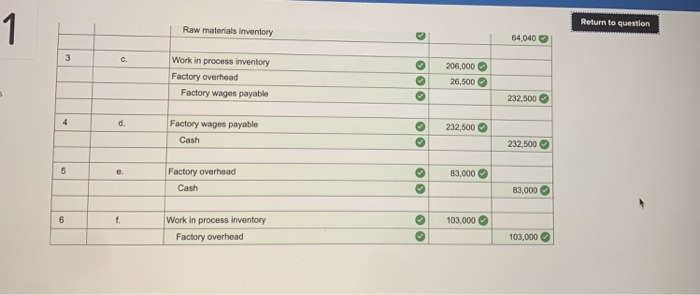

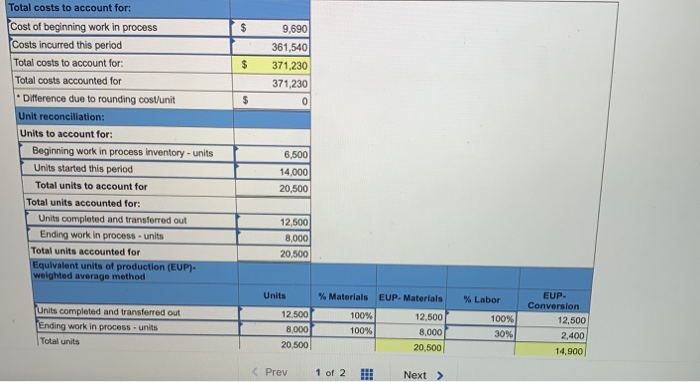

Check my work Major League Bat Company manufactures baseball bats. In addition to its work in process inventories, the company maintains inventories of raw materials and finished goods, It uses raw materials as direct materials in production and as indirect materials. Its factory payroll costs include direct labor for production and indirect labor. All materials are added at the beginning of the process, and conversion costs are applied uniformly throughout the production process Required: You are to maintain records and produce measures of inventories to reflect the July events of this company. The June 30 balances: Raw Materials Inventory. $22,000; Work in Process Inventory. $9,690 (52,810 of direct materials and $6,880 of conversionk Finished Goods Inventory. $140,000; Sales, $o; Cost of Goods Sold. $0; Factory Payroll Payable, 50; and Factory Overhead, $0. Book References 1. Prepare journal entries to record the following July transactions and events a. Purchased raw materials for $130.000 cash (the company uses a perpetual inventory system). b. Used raw materials as follows: direct materials, $52.540, and indirect materials, $11,500. c. Recorded factory payroll payable costs as follows: direct labor, $206,000; and indirect labor, $26,500. d. Paid factory payroll cost of $232,500 with cash ignore taxes). e. Incurred additional factory overhead costs of $83.000 paid in cash. f. Allocated factory overhead to production at 50% of direct labor costs. View transaction list Journal entry worksheet Return to question Raw materials inventory 64,040 Work in process inventory Factory overhead Factory wages payable 206,000 26,500 232.500 Factory wages payable Cash 232,500 232,500 e. 83,000 Factory overhead Cash 83,000 1 103.000 Work in process inventory Factory overhead 103,000 $ 9,690 361,5401 371,230 371.230 $ Total costs to account for: Cost of beginning work in process Costs incurred this period Total costs to account for: Total costs accounted for * Difference due to rounding costunit Unit reconciliation: Units to account for: Beginning work in process inventory - units Units started this period Total units to account for Total units accounted for: Units completed and transferred out Ending work in process units Total units accounted for Equivalent units of production (EUP). weighted average method 6,500 14,000 20,500 12.500 8.000 20,500 Units Units completed and transferred out Ending work in process units Total units % Materials EUP. Materials 100% 12,500 100% 8,000 20,500 EUP. Conversion 12,500 12,500 8.000 20,500 % Labor 100% 30% 2.400 14,900 weighted average method Units % Materials EUP-Materials % Labor 100% 100% 12,500 8,000 20,500 100% 30% Materials $ 2,810 52,540| $ 55,350 20,500 $ 2.70 EUP Conversion 12,500 2,400 14,900 Conversion $ 6,880 309,000 $ 315,880 14,900 $ 21.20 Costs EUP Costs EUP Units completed and transferred out 12,500 Ending work in process - units 8,000 Total units 20,500 Cost per equivalent unit of production Cost of beginning work in process Costs incurred this period Total costs + Equivalent units of production Cost per equivalent unit of production (rounded to 2 decimals) Total costs accounted for: Cost of units transferred out: EUP Direct materials 12,500 Conversion 12,500 Total costs transferred out Costs of ending goods in process EUP Direct materials 8,000 Conversion 2.400 Total cost of ending goods in process Total costs accounted for Cost per EUP $ 2.70 $ 21.20 Total cost $ 33,750 265,000 $ 298,750 Cost per EUP $ 2.70 $ 21.20 Total cost $ 21,600 50,880 72,480 371.230 $ 3. Using the results from part 2 and the available information, make computations and prepare journal entries to record the following: g. Total costs transferred to finished goods for July h. Sale of finished goods costing $273,200 for $640,000 in cash. View transaction list View journal entry worksheet No Transaction Debit Credit General Journal Finished goods inventory Work in process inventory 640,000 640,000 3 h 273.200 Cost of goods sold Finished goods inventory 273.200 4. Post entries from parts 1 and 3 to the following general ledger accounts. Raw Materials Inventory Debit Credit Acct. No. 132 Balance Work in Process Inventory Debit Credit Date Date Acct. No. 133 Balance 9,690 June 30 June 30 Finished Goods Inventory Date Debit Credit June 30 Acct. No. 135 Balance 140,000 Factory Wages Payable Debit Acct. No. 212 Balance Date Credit Sales Debit Acct. No. 413 Balance Credit Cost of Goods Sold Debit Date Date Acct. No. 502 Balance Credit Checi Finished Goods Inventory Date Debit Credit June 30 Acct. No. 135 Balance 140,000 Factory Wages Payable Debit Date Credit Acct. No. 212 Balance Sales Debit Acct. No. 413 Balance Cost of Goods Sold Debit Acct. No. 502 Balance Date Credit Date Credit Factory Overhead Debit Acct. No. 540 Balance Date Credit Check my work Major League Bat Company manufactures baseball bats. In addition to its work in process inventories, the company maintains inventories of raw materials and finished goods, It uses raw materials as direct materials in production and as indirect materials. Its factory payroll costs include direct labor for production and indirect labor. All materials are added at the beginning of the process, and conversion costs are applied uniformly throughout the production process Required: You are to maintain records and produce measures of inventories to reflect the July events of this company. The June 30 balances: Raw Materials Inventory. $22,000; Work in Process Inventory. $9,690 (52,810 of direct materials and $6,880 of conversionk Finished Goods Inventory. $140,000; Sales, $o; Cost of Goods Sold. $0; Factory Payroll Payable, 50; and Factory Overhead, $0. Book References 1. Prepare journal entries to record the following July transactions and events a. Purchased raw materials for $130.000 cash (the company uses a perpetual inventory system). b. Used raw materials as follows: direct materials, $52.540, and indirect materials, $11,500. c. Recorded factory payroll payable costs as follows: direct labor, $206,000; and indirect labor, $26,500. d. Paid factory payroll cost of $232,500 with cash ignore taxes). e. Incurred additional factory overhead costs of $83.000 paid in cash. f. Allocated factory overhead to production at 50% of direct labor costs. View transaction list Journal entry worksheet Return to question Raw materials inventory 64,040 Work in process inventory Factory overhead Factory wages payable 206,000 26,500 232.500 Factory wages payable Cash 232,500 232,500 e. 83,000 Factory overhead Cash 83,000 1 103.000 Work in process inventory Factory overhead 103,000 $ 9,690 361,5401 371,230 371.230 $ Total costs to account for: Cost of beginning work in process Costs incurred this period Total costs to account for: Total costs accounted for * Difference due to rounding costunit Unit reconciliation: Units to account for: Beginning work in process inventory - units Units started this period Total units to account for Total units accounted for: Units completed and transferred out Ending work in process units Total units accounted for Equivalent units of production (EUP). weighted average method 6,500 14,000 20,500 12.500 8.000 20,500 Units Units completed and transferred out Ending work in process units Total units % Materials EUP. Materials 100% 12,500 100% 8,000 20,500 EUP. Conversion 12,500 12,500 8.000 20,500 % Labor 100% 30% 2.400 14,900 weighted average method Units % Materials EUP-Materials % Labor 100% 100% 12,500 8,000 20,500 100% 30% Materials $ 2,810 52,540| $ 55,350 20,500 $ 2.70 EUP Conversion 12,500 2,400 14,900 Conversion $ 6,880 309,000 $ 315,880 14,900 $ 21.20 Costs EUP Costs EUP Units completed and transferred out 12,500 Ending work in process - units 8,000 Total units 20,500 Cost per equivalent unit of production Cost of beginning work in process Costs incurred this period Total costs + Equivalent units of production Cost per equivalent unit of production (rounded to 2 decimals) Total costs accounted for: Cost of units transferred out: EUP Direct materials 12,500 Conversion 12,500 Total costs transferred out Costs of ending goods in process EUP Direct materials 8,000 Conversion 2.400 Total cost of ending goods in process Total costs accounted for Cost per EUP $ 2.70 $ 21.20 Total cost $ 33,750 265,000 $ 298,750 Cost per EUP $ 2.70 $ 21.20 Total cost $ 21,600 50,880 72,480 371.230 $ 3. Using the results from part 2 and the available information, make computations and prepare journal entries to record the following: g. Total costs transferred to finished goods for July h. Sale of finished goods costing $273,200 for $640,000 in cash. View transaction list View journal entry worksheet No Transaction Debit Credit General Journal Finished goods inventory Work in process inventory 640,000 640,000 3 h 273.200 Cost of goods sold Finished goods inventory 273.200 4. Post entries from parts 1 and 3 to the following general ledger accounts. Raw Materials Inventory Debit Credit Acct. No. 132 Balance Work in Process Inventory Debit Credit Date Date Acct. No. 133 Balance 9,690 June 30 June 30 Finished Goods Inventory Date Debit Credit June 30 Acct. No. 135 Balance 140,000 Factory Wages Payable Debit Acct. No. 212 Balance Date Credit Sales Debit Acct. No. 413 Balance Credit Cost of Goods Sold Debit Date Date Acct. No. 502 Balance Credit Checi Finished Goods Inventory Date Debit Credit June 30 Acct. No. 135 Balance 140,000 Factory Wages Payable Debit Date Credit Acct. No. 212 Balance Sales Debit Acct. No. 413 Balance Cost of Goods Sold Debit Acct. No. 502 Balance Date Credit Date Credit Factory Overhead Debit Acct. No. 540 Balance Date Credit