Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Chrome File Edit View History Bookmarks Profiles Tab Window Help HW05_Spring_2024.pdf: ECC X > HW05_Spring_2024 (4).pdf C Home Learn with Chegg + File /Users/kshamamumbai/Downloads/HW05_Spring_2024%20(4).pdf

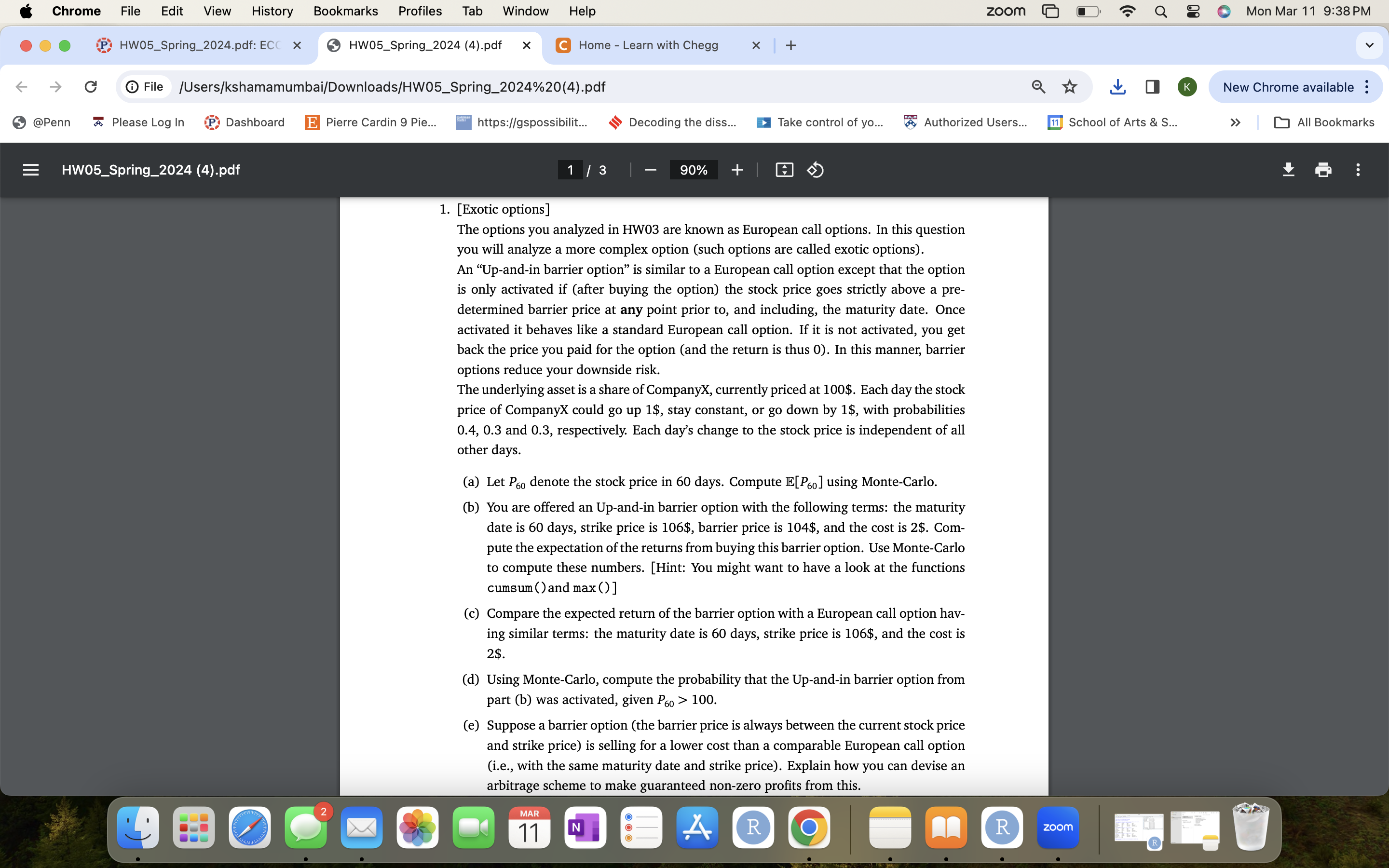

Chrome File Edit View History Bookmarks Profiles Tab Window Help HW05_Spring_2024.pdf: ECC X > HW05_Spring_2024 (4).pdf C Home Learn with Chegg + File /Users/kshamamumbai/Downloads/HW05_Spring_2024%20(4).pdf @Penn Please Log In Dashboard E Pierre Cardin 9 Pie... https://gspossibilit... HW05_Spring_2024 (4).pdf 2 zoom Mon Mar 11 9:38 PM K New Chrome available: Decoding the diss... Take control of yo... Authorized Users... 11 School of Arts & S... | All Bookmarks 1 / 3 - 90% 1. [Exotic options] The options you analyzed in HW03 are known as European call options. In this question you will analyze a more complex option (such options are called exotic options). An "Up-and-in barrier option is similar to a European call option except that the option is only activated if (after buying the option) the stock price goes strictly above a pre- determined barrier price at any point prior to, and including, the maturity date. Once activated it behaves like a standard European call option. If it is not activated, you get back the price you paid for the option (and the return is thus 0). In this manner, barrier options reduce your downside risk. The underlying asset is a share of CompanyX, currently priced at 100$. Each day the stock price of CompanyX could go up 1$, stay constant, or go down by 1$, with probabilities 0.4, 0.3 and 0.3, respectively. Each day's change to the stock price is independent of all other days. (a) Let P60 denote the stock price in 60 days. Compute E[P60] using Monte-Carlo. (b) You are offered an Up-and-in barrier option with the following terms: the maturity date is 60 days, strike price is 106$, barrier price is 104$, and the cost is 2$. Com- pute the expectation of the returns from buying this barrier option. Use Monte-Carlo to compute these numbers. [Hint: You might want to have a look at the functions cumsum() and max()] (c) Compare the expected return of the barrier option with a European call option hav- ing similar terms: the maturity date is 60 days, strike price is 106$, and the cost is 2$. (d) Using Monte-Carlo, compute the probability that the Up-and-in barrier option from part (b) was activated, given P60 > 100. (e) Suppose a barrier option (the barrier price is always between the current stock price and strike price) is selling for a lower cost than a comparable European call option (i.e., with the same maturity date and strike price). Explain how you can devise an arbitrage scheme to make guaranteed non-zero profits from this. MAR 11 N A R O R zoom

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction to Java Programming, Comprehensive Version

Authors: Y. Daniel Liang

10th Edition

133761312, 978-0133761313