Answered step by step

Verified Expert Solution

Question

1 Approved Answer

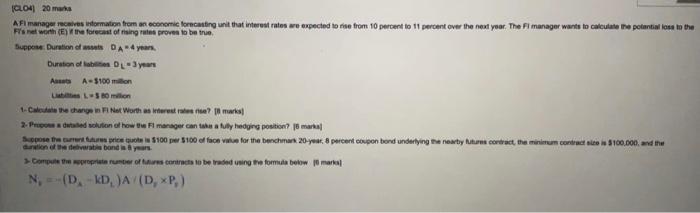

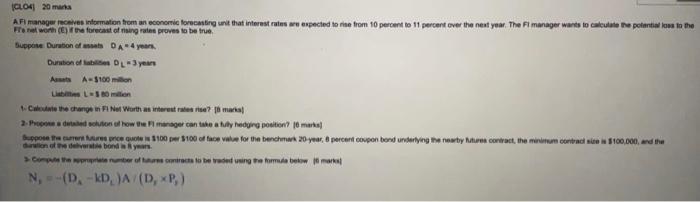

(CLO4) 20 marks AFI manager receives information from an economic forecasting unit that interest rates are expected to rise from 10 percent to 11 percent

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Restructuring Retirement Risks

Authors: David Blitzstein , Olivia S. Mitchell , Stephen P. Utkus

1st Edition

0199204659,0191525456