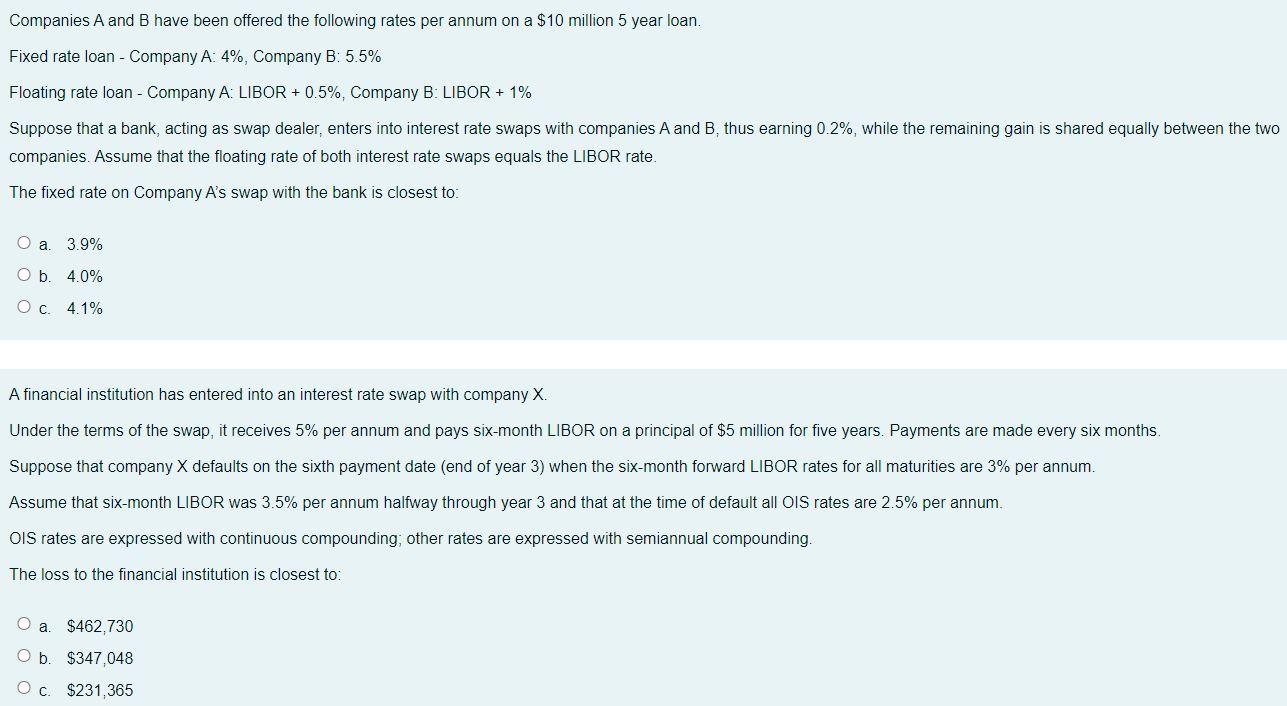

Companies A and B have been offered the following rates per annum on a $10 million 5 year loan. Fixed rate loan - Company A: 4%, Company B: 5.5% Floating rate loan - Company A: LIBOR + 0.5%, Company B: LIBOR + 1% Suppose that a bank, acting as swap dealer, enters into interest rate swaps with companies A and B, thus earning 0.2%, while the remaining gain is shared equally between the two companies. Assume that the floating rate of both interest rate swaps equals the LIBOR rate. The fixed rate on Company A's swap with the bank is closest to: O a 3.9% Ob. 4.0% Oc 4.1% A financial institution has entered into an interest rate swap with company X. Under the terms of the swap, it receives 5% per annum and pays six-month LIBOR on a principal of $5 million for five years. Payments are made every six months. Suppose that company X defaults on the sixth payment date (end of year 3) when the six-month forward LIBOR rates for all maturities are 3% per annum. Assume that six-month LIBOR was 3.5% per annum halfway through year 3 and that at the time of default all OIS rates are 2.5% per annum. OIS rates are expressed with continuous compounding; other rates are expressed with semiannual compounding. The loss to the financial institution is closest to: a. $462,730 ob. $347,048 OC. $231,365 Companies A and B have been offered the following rates per annum on a $10 million 5 year loan. Fixed rate loan - Company A: 4%, Company B: 5.5% Floating rate loan - Company A: LIBOR + 0.5%, Company B: LIBOR + 1% Suppose that a bank, acting as swap dealer, enters into interest rate swaps with companies A and B, thus earning 0.2%, while the remaining gain is shared equally between the two companies. Assume that the floating rate of both interest rate swaps equals the LIBOR rate. The fixed rate on Company A's swap with the bank is closest to: O a 3.9% Ob. 4.0% Oc 4.1% A financial institution has entered into an interest rate swap with company X. Under the terms of the swap, it receives 5% per annum and pays six-month LIBOR on a principal of $5 million for five years. Payments are made every six months. Suppose that company X defaults on the sixth payment date (end of year 3) when the six-month forward LIBOR rates for all maturities are 3% per annum. Assume that six-month LIBOR was 3.5% per annum halfway through year 3 and that at the time of default all OIS rates are 2.5% per annum. OIS rates are expressed with continuous compounding; other rates are expressed with semiannual compounding. The loss to the financial institution is closest to: a. $462,730 ob. $347,048 OC. $231,365