Answered step by step

Verified Expert Solution

Question

1 Approved Answer

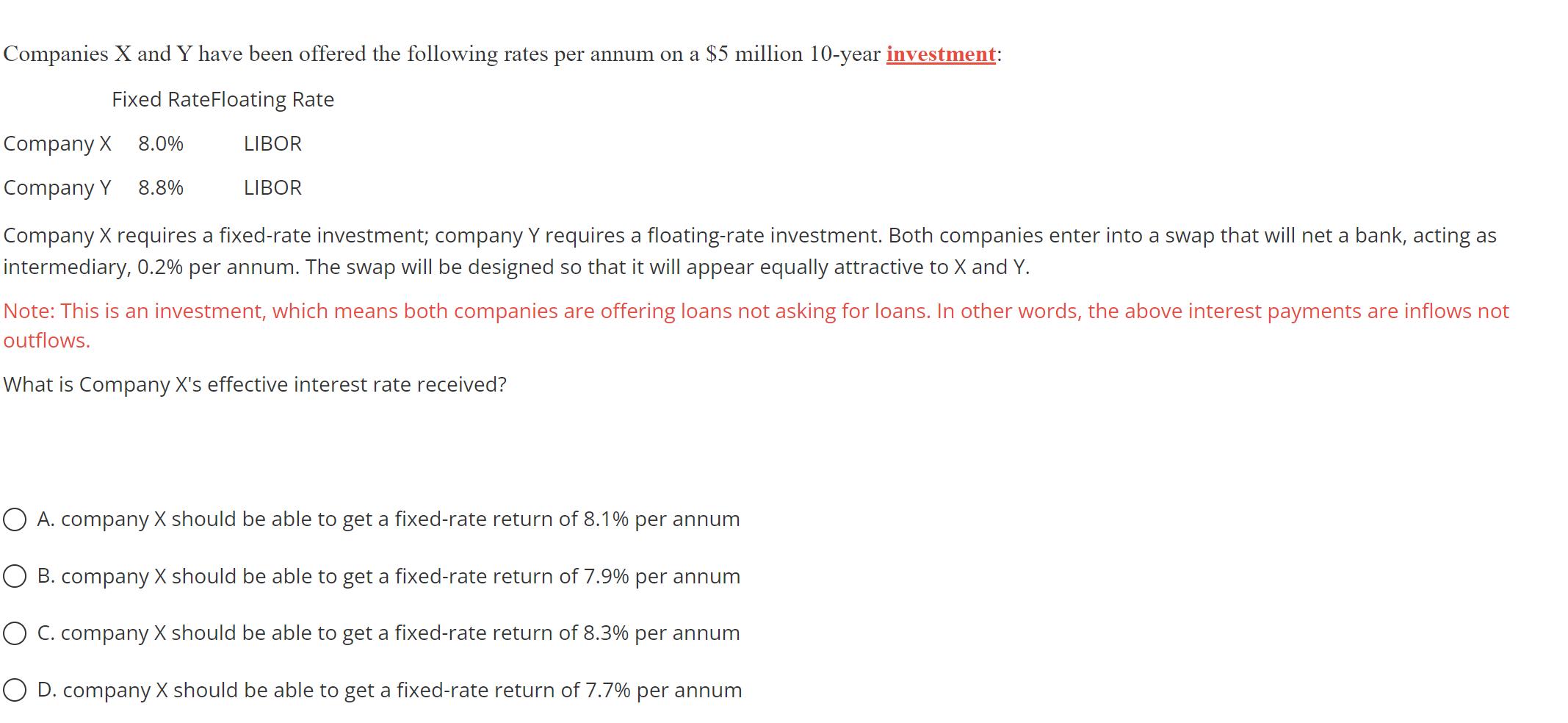

Companies X and Y have been offered the following rates per annum on a $5 million 10-year investment: Fixed RateFloating Rate Company X 8.0%

Companies X and Y have been offered the following rates per annum on a $5 million 10-year investment: Fixed RateFloating Rate Company X 8.0% Company Y 8.8% LIBOR LIBOR Company X requires a fixed-rate investment; company Y requires a floating-rate investment. Both companies enter into a swap that will net a bank, acting as intermediary, 0.2% per annum. The swap will be designed so that it will appear equally attractive to X and Y. Note: This is an investment, which means both companies are offering loans not asking for loans. In other words, the above interest payments are inflows not outflows. What is Company X's effective interest rate received? A. company X should be able to get a fixed-rate return of 8.1% per annum B. company X should be able to get a fixed-rate return of 7.9% per annum C. company X should be able to get a fixed-rate return of 8.3% per annum D. company X should be able to get a fixed-rate return of 7.7% per annum

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Futures and Options Markets

Authors: John C. Hull

8th edition

978-1292155036, 1292155035, 132993341, 978-0132993340