company 1:AAON INC

company 2:AECOM

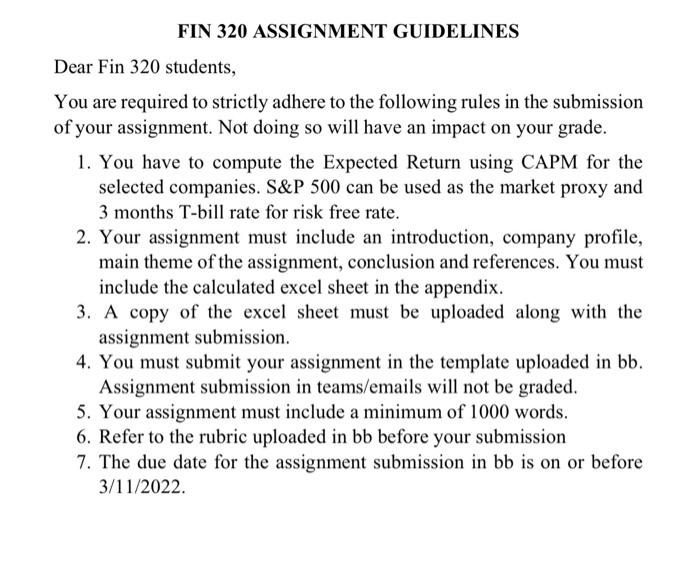

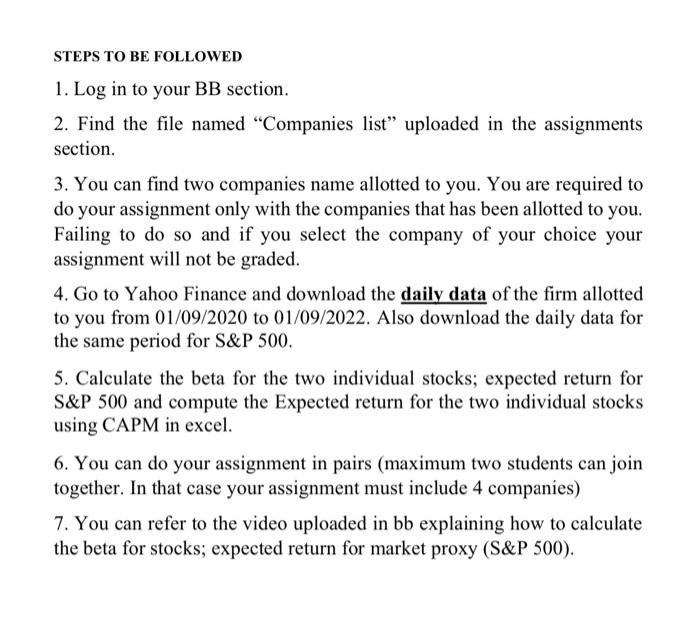

Dear Fin 320 students, You are required to strictly adhere to the following rules in the submission of your assignment. Not doing so will have an impact on your grade. 1. You have to compute the Expected Return using CAPM for the selected companies. S\&P 500 can be used as the market proxy and 3 months T-bill rate for risk free rate. 2. Your assignment must include an introduction, company profile, main theme of the assignment, conclusion and references. You must include the calculated excel sheet in the appendix. 3. A copy of the excel sheet must be uploaded along with the assignment submission. 4. You must submit your assignment in the template uploaded in bb. Assignment submission in teams/emails will not be graded. 5. Your assignment must include a minimum of 1000 words. 6. Refer to the rubric uploaded in bb before your submission 7. The due date for the assignment submission in bb is on or before 3/11/2022. 2. Find the file named "Companies list" uploaded in the assignments section. 3. You can find two companies name allotted to you. You are required to do your assignment only with the companies that has been allotted to you. Failing to do so and if you select the company of your choice your assignment will not be graded. 4. Go to Yahoo Finance and download the daily data of the firm allotted to you from 01/09/2020 to 01/09/2022. Also download the daily data for the same period for S\&P 500. 5. Calculate the beta for the two individual stocks; expected return for S\&P 500 and compute the Expected return for the two individual stocks using CAPM in excel. 6. You can do your assignment in pairs (maximum two students can join together. In that case your assignment must include 4 companies) 7. You can refer to the video uploaded in bb explaining how to calculate the beta for stocks; expected return for market proxy (S\&P 500). Dear Fin 320 students, You are required to strictly adhere to the following rules in the submission of your assignment. Not doing so will have an impact on your grade. 1. You have to compute the Expected Return using CAPM for the selected companies. S\&P 500 can be used as the market proxy and 3 months T-bill rate for risk free rate. 2. Your assignment must include an introduction, company profile, main theme of the assignment, conclusion and references. You must include the calculated excel sheet in the appendix. 3. A copy of the excel sheet must be uploaded along with the assignment submission. 4. You must submit your assignment in the template uploaded in bb. Assignment submission in teams/emails will not be graded. 5. Your assignment must include a minimum of 1000 words. 6. Refer to the rubric uploaded in bb before your submission 7. The due date for the assignment submission in bb is on or before 3/11/2022. 2. Find the file named "Companies list" uploaded in the assignments section. 3. You can find two companies name allotted to you. You are required to do your assignment only with the companies that has been allotted to you. Failing to do so and if you select the company of your choice your assignment will not be graded. 4. Go to Yahoo Finance and download the daily data of the firm allotted to you from 01/09/2020 to 01/09/2022. Also download the daily data for the same period for S\&P 500. 5. Calculate the beta for the two individual stocks; expected return for S\&P 500 and compute the Expected return for the two individual stocks using CAPM in excel. 6. You can do your assignment in pairs (maximum two students can join together. In that case your assignment must include 4 companies) 7. You can refer to the video uploaded in bb explaining how to calculate the beta for stocks; expected return for market proxy (S\&P 500)