Answered step by step

Verified Expert Solution

Question

1 Approved Answer

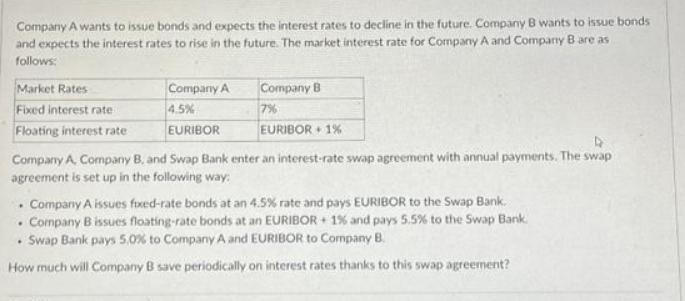

Company A wants to issue bonds and expects the interest rates to decline in the future. Company B wants to issue bonds and expects

Company A wants to issue bonds and expects the interest rates to decline in the future. Company B wants to issue bonds and expects the interest rates to rise in the future. The market interest rate for Company A and Company B are as follows: Market Rates Fixed interest rate Floating interest rate Company A 4.5% EURIBOR Company B 7% EURIBOR+ 1% Company A, Company B, and Swap Bank enter an interest-rate swap agreement with annual payments. The swap agreement is set up in the following way: . Company A issues fixed-rate bonds at an 4.5% rate and pays EURIBOR to the Swap Bank. Company B issues floating-rate bonds at an EURIBOR+ 1% and pays 5.5% to the Swap Bank. Swap Bank pays 5,0% to Company A and EURIBOR to Company B. How much will Company B save periodically on interest rates thanks to this swap agreement?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

l Let me show the stepbystep calculations Company As position Company A issued fixedrate bonds payin...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations of Financial Management

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen, Doug Short, Michael Perretta

10th Canadian edition

1259261018, 1259261015, 978-1259024979